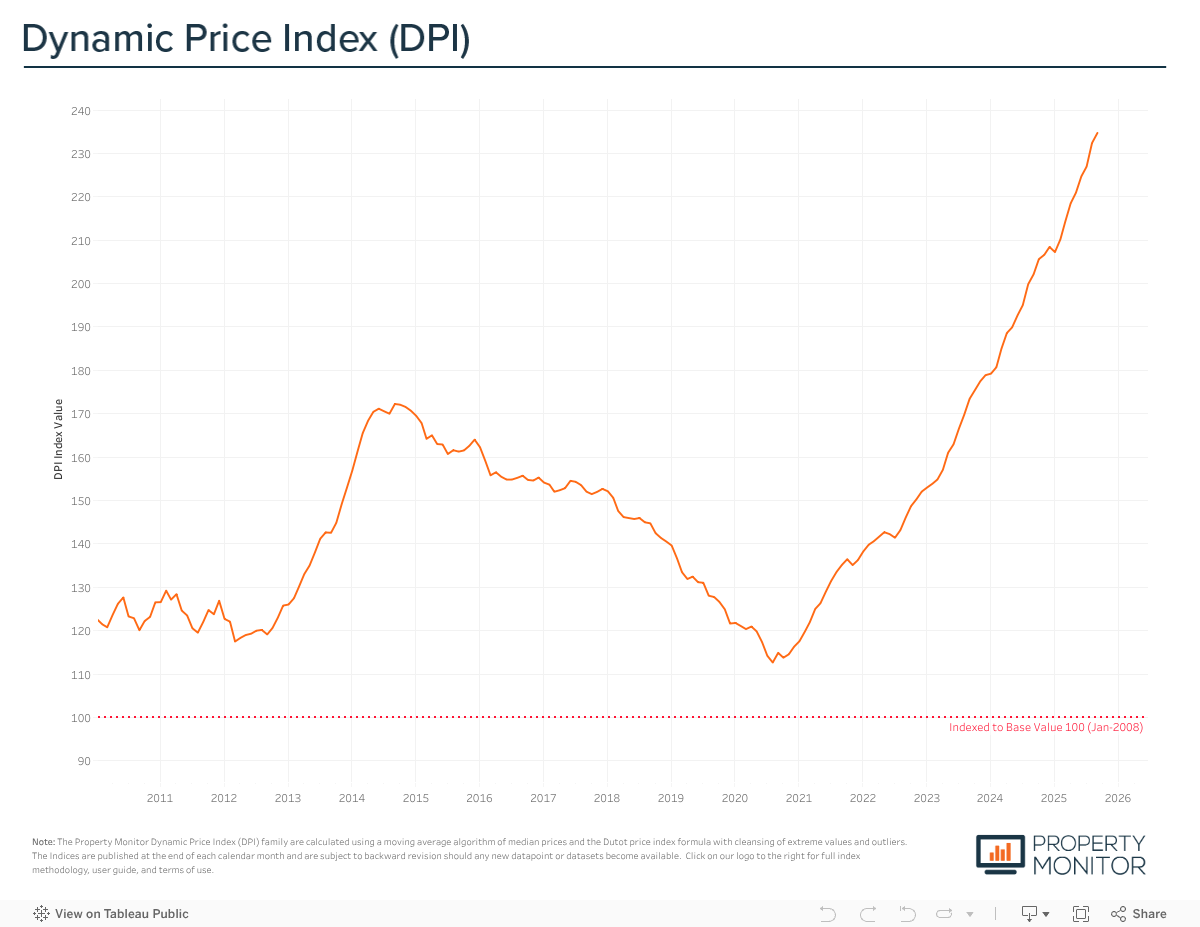

Dubai’s residential real estate market sustained its growth momentum in September, though at a slower pace than the month prior. Average prices increased by 1.0% month-on-month, easing from August’s stronger 2.4% rise. According to the Property Monitor Dynamic Price Index (DPI), the average price reached AED 1,681 per square foot—now 106.3% above the market trough recorded in October 2020 and 36.3% higher than the previous market peak of September 2014.

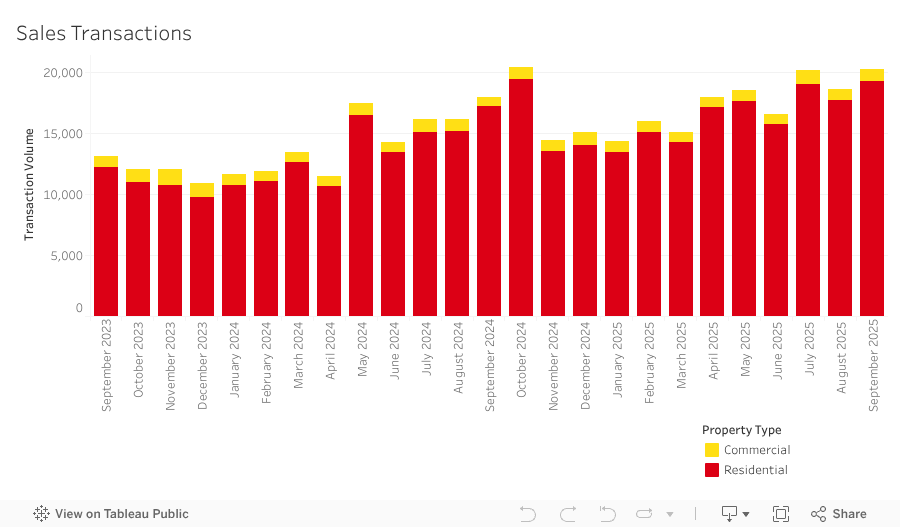

A total of 20,309 sales transactions were recorded in September, an 8.9% increase from August. This marks the highest level ever achieved for the month of September and the second-highest monthly total on record, trailing only October 2024 by just 159 sales. The continued acceleration in activity highlights the market’s sustained growth momentum and enduring buyer appetite heading into the final quarter of the year. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 94.3% (19,158 transactions). The highest transacted commercial property types were office spaces (1.9%), vacant land (1.5%), then hotel apartments (0.7%).

Year-to-date sales transaction volumes have exceeded 158,000, up more than 20% compared to the same period in 2024. Monthly activity has averaged roughly 17,500 transactions over the past 12 months, with only two months falling below 15,000. If this pace continues through year-end, total sales are projected to surpass 210,000 transactions, establishing a new all-time annual record and extending Dubai’s record-breaking streak for a third consecutive year.

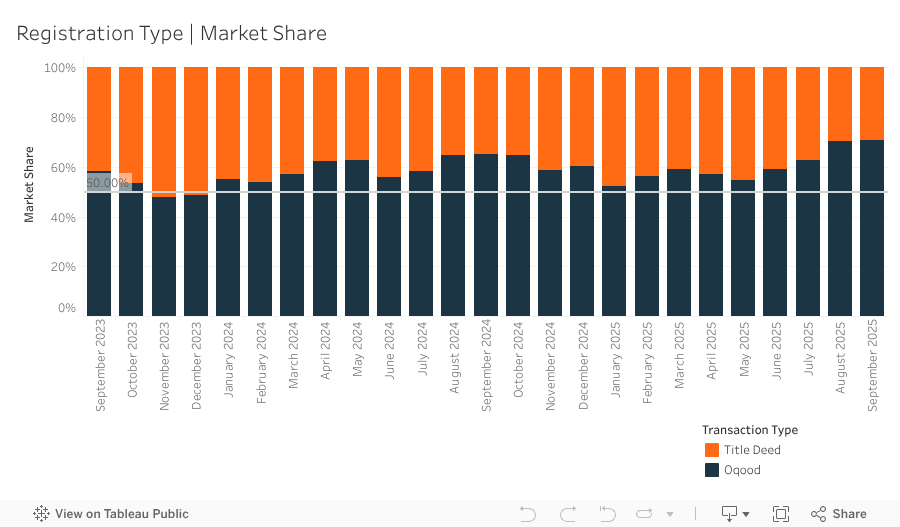

In September, 14,371 off-plan (Oqood) transactions were recorded, a 9.6% increase from the previous month. Alongside the higher volume, the off-plan market’s share of total sales also expanded to 70.8%, up 0.5% month-on-month. While Oqood registrations are typically used to track off-plan activity, a number of villa and townhouse sales are recorded by the Dubai Land Department as Title Deed transactions—classified as completed properties rather than units under construction. After adjusting for this technical discrepancy, the true off-plan share rises to approximately 76.1%. This reinforces the current dominant role of the off-plan segment in driving overall market growth, while also highlighting a growing dependence on future project deliveries rather than immediately available inventory. Title Deed transactions likewise increased, up 7.2% month-on-month, though their market share contracted slightly to 29.2%.

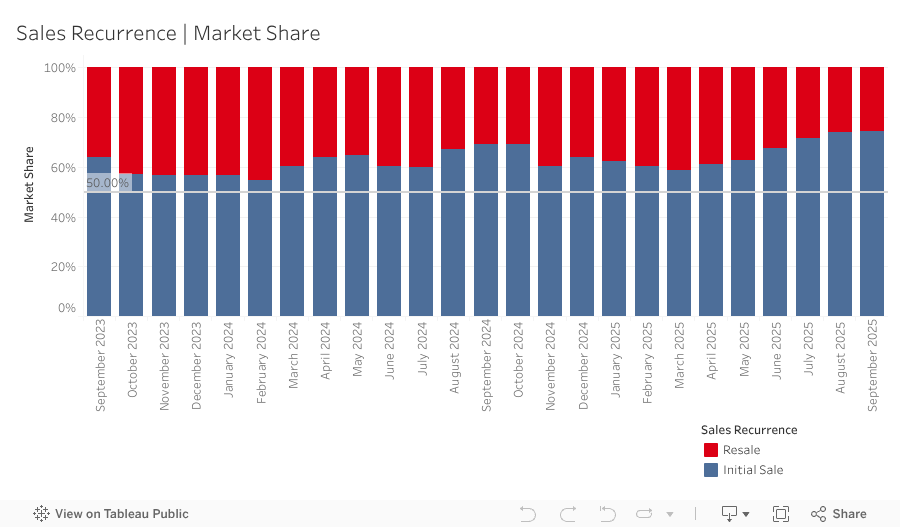

Meanwhile, resale transactions—any subsequent sale of a property following its initial sale by the developer—regardless of whether the first sale was off-plan or completed—totaled 5,191 in September, accounting for 25.6% of all sales and remaining largely unchanged from August. Off-plan resales edged lower, representing 20.3% of all resale activity, while the 12-month rolling average continued its downward trend to 25.4%. After peaking above 33% in April, off-plan resales remain well below previous highs despite sustained strength in the initial developer sales market.

These shifts indicate that resale activity is being shaped less by short-term investor exits prior to handover and more by a natural moderation in buyer demand as the market transitions into a more mature phase of the cycle. Developers, meanwhile, continue to market unsold inventory across multiple projects, offering incentives and flexible payment plans that make direct sales increasingly attractive. This growing divergence between initial and resale market dynamics is placing additional pressure on resale listings, particularly those priced above original purchase prices.

Dubai’s new project pipeline remained robust in September, with 62 launches introducing more than 15,000 residential units valued at an estimated AED 38.6 billion. Year-to-date, over 460 projects have been launched, bringing nearly 117,000 units to market—volumes that far exceed what would traditionally represent a full year of activity. A total of 205 developers have launched projects so far in 2025, compared to 143 during the same period in 2024, highlighting the growing breadth of supply-side participation. Apartments dominated September’s launches at 88.4% of total supply, broadly consistent with the 2025 year-to-date share of 90.2% (up from 85.0% in 2024). Townhouses and villas accounted for 9.0% and 2.6%, respectively. While this steady flow of launches underscores developer confidence, absorption is showing early signs of softening—particularly for apartments—as newer entrants face slower uptake and rely increasingly on incentives and flexible payment plans to attract buyers.

Mortgage activity declined in September, registering 3,790 loans, a 17.2% month-on-month drop and the largest decline since Q2 2024, though still the second-strongest September on record. The slowdown appears to be largely driven by bulk mortgage activity, with major investors and developers likely postponing financing to benefit from the recent 25 basis-point rate cut once fully implemented. New purchase mortgages accounted for 50.9% of transactions, up 8.5% from August, with an average loan size of AED 1.79 million and an average loan-to-value (LTV) ratio of 73.6%. Refinancing and equity release loans rose to a 43.2% share (up 10.4%), while bulk mortgages fell 18.9% to just 5.9% of total activity. The 223 bulk loans recorded were spread across multiple projects, most notably The Polo Residence C8 (30) in Meydan, HDS Sunstar 1 (19) in International City, and Almas Tower (10) in Jumeirah Lakes Towers.

As the market advances into the final quarter of the year, Dubai’s residential sector remains firmly in growth territory, even as indicators point to a gradual cooling of momentum. Price appreciation has eased to more sustainable levels, and while transaction volumes continue to break historical records, the pace of absorption—particularly in the off-plan segment—is beginning to normalize.

The recent 25 basis-point rate cut is expected to provide renewed support to mortgage activity in the months ahead, especially as larger investors and developers resume any postponed plans for bulk financing. With additional rate reductions anticipated before year-end, lending conditions are likely to improve further, reinforcing purchase demand and stimulating refinancing activity.

Despite the moderation in price growth, underlying fundamentals remain robust. Continued population inflows, strong economic performance, and Dubai’s enduring appeal as a regional and global investment hub are helping sustain buyer confidence. However, the combination of rising new supply, slower resale activity, and growing affordability constraints suggests the market is entering a more mature and selective phase. The coming months will test how effectively both developers and buyers adapt to this evolving balance between abundant supply, moderating demand, and gradually easing financial conditions.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |