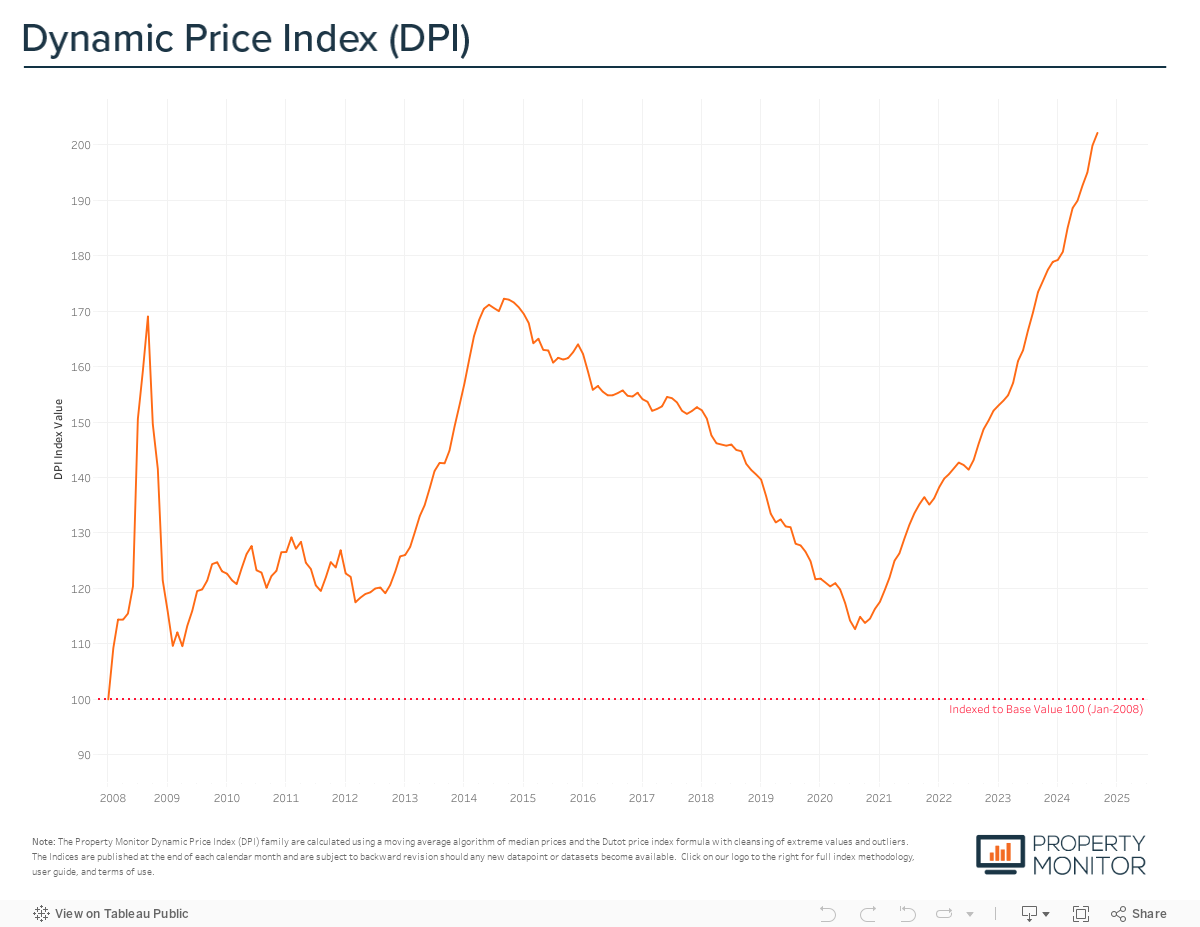

After surging to more than double the monthly average growth rate last month (2.48%), Dubai property price appreciation returned to a more subdued and moderate pace of 1.14% in September, coming back in line with the overall average rate of the current market cycle (1.23%). Fluctuations such as this are to be expected due to the dual nature of the Dubai real estate market, where not only is there steady trading of ready properties that transact relatively consistently and uniformly each month; but also an off-plan market where sales registrations come in waves as new projects are launched and with many developers submitting Oqood registrations in batches.

According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices grew by 1.14% in September and currently stand at AED 1,448 per square foot, 17.4% over the previous all-time high and market peak of September 2014. This brings the overall growth of the market cycle to 57.9% and marks the forty-seventh month since prices bottomed out in late 2020.

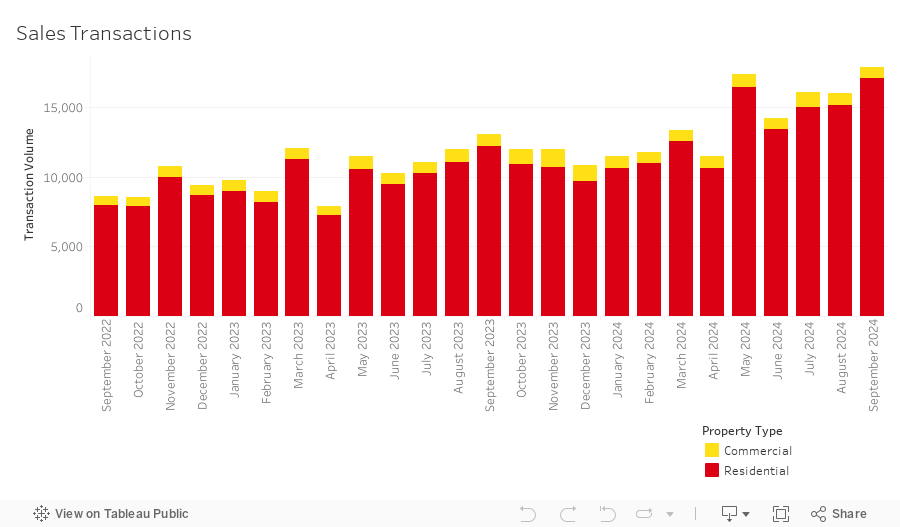

The total volume of sales transactions witnessed a significant increase of 11.7% in September, reaching a total of 18,038 transactions and marking not only the highest-ever September volume, but also the highest month on record overall. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 95.1% (17,151 transactions). The highest transacted commercial property types were office spaces (1.9%), vacant land (0.95%), and hotel apartments (0.9%).

Annual sales transaction volumes have now surpassed 131,000 and are just 1.9% shy of year-end sales from 2023. With three months remaining, we are on track to see a year-on-year increase of nearly 30% (~170,000 sales). To put this into perspective, by year-end 2024 we will have reached a level of sales activity quadruple that of pre-COVID trading. This phenomenal growth is not simply a post-pandemic recovery, it is unlike that of any other market in the world and is testament to the never-ending commitment of the UAE and Dubai government’s strategic plans, initiatives, and proactive approach to the evolution of the market.

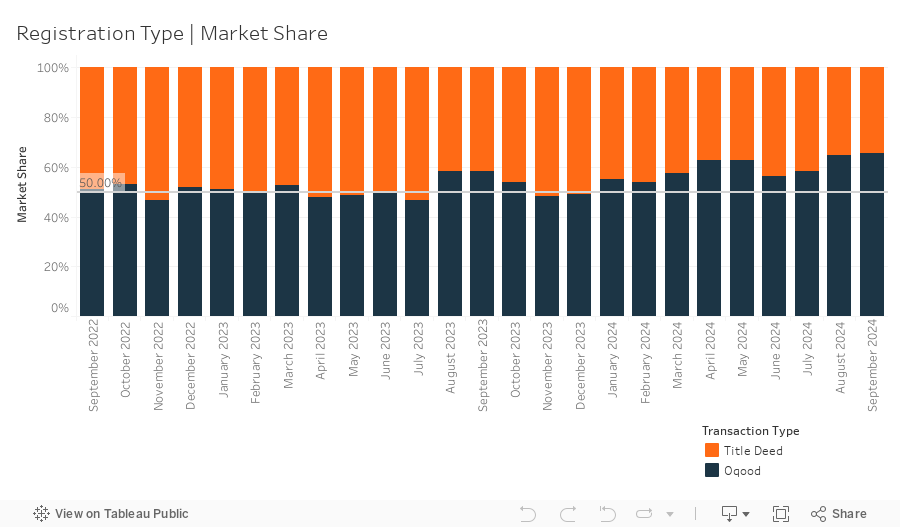

In September, 11,812 off-plan Oqood transactions were recorded, an increase of 12.9% from the previous month and saw a continued jump in market share to 65.5%. Meanwhile, Title Deed sale volumes also witnessed an increase, growing by 9.6% and now account for 34.5% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, offplan transactions secure an even larger market share of 72.8%.

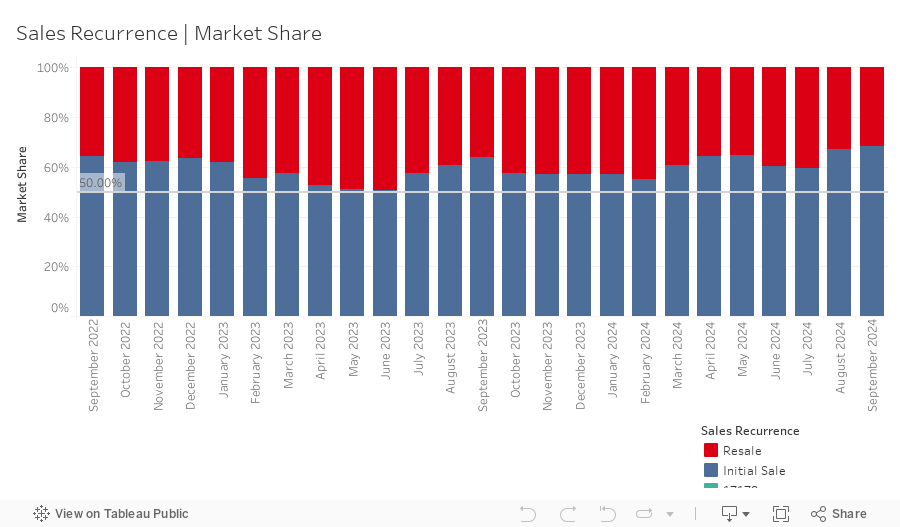

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an offplan or completed project—stood at 5,666 in September representing a market share of 31.4%, decreasing by 1.2% month-on-month. While overall resale activity decreased, the portion of off-plan resales increased 1.7% to 25.9% and registers as the second-highest level of the current market cycle. Off-plan resale activity has been on a consistent, yet slow, upwards trend over the past three years, however, and as with previous months, the majority of these resales remain skewed towards properties that are within a year of anticipated completion and as such don’t ring alarm bells of purely speculative activity.

New off-plan development project launches remain at record highs, with just over 13,500 off-plan units added to the market for sale with an anticipated combined gross sales value of ~AED 28.9 billion. Apartments represent 83.5% by volume of this new inventory, while townhouses and villas represent 14.1% and 2.4% respectively. Yearto-date, new project launches have reached slightly less than 100,000 units and AED 242.7 billion in aggregate sales value. This surpasses the volume of units launched in 2023, however falls short by ~AED 30 billion in sales value by comparison. With more than double the amount of developers active in the market, this has led to a much greater diversity in product offerings—while 2023 saw launches skewed towards the luxury and ultra-luxury segments, 2024 has seen projects spread across a wider range of price segments. With over 250 additional projects in the planning phases being tracked by the Property Monitor team, we anticipate that new launches will maintain historically high levels throughout the remainder of 2024 and well into 2025.

After dipping mildly in August, mortgage transaction volumes increased by 16.6% in September and recorded the second highest level of loans ever recorded with 4,183 registrations. This boost in overall mortgage activity follows the easing of interest rates across both variable and fixed rates, with the biggest reduction being witnessed with variable products (down ~20 basis points). During the month, loans taken for new purchase money mortgages accounted for 44.4% (down 6.9% from last month) of borrowing activity, with the average amount borrowed being AED 1.73m at a loan-to-value ratio of 76.6%. Meanwhile, loans for refinancing and equity release saw their market share decrease by 0.2% to 34.5%. The remaining 21.1% (up by 7.1% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 881 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at La Perla Blanca (190) in Jumeirah Village Circle, Al Manal Residence 1 (129) in Dubai Silicon Oasis, and Ikarus Tower (127) in Dubai Production City.

As we enter the final quarter of the year, we expect the Dubai property market to sustain its positive momentum, driven by steady price growth and strong transaction volumes. However, it’s crucial that monthly price appreciation remains moderate, ideally within the 1% range or lower, as any sustained increases above 2% could raise concerns about potential overheating.

While we do not foresee an overall slowdown, the gap between offplan and completed property sales is likely to widen. This is due to a combination of the robust pipeline of off-plan projects and the availability of competitively priced inventory. In this context, the rising level of off-plan resales must be carefully monitored, especially when considering the timeline to completion. A growing trend of flipping properties well ahead of their handover could place further pressure on both pricing and supply.

Meanwhile, ready properties could see a rise in demand as mortgage rates ease, but sellers should be cautious. Attempting to push aggressive pricing strategies may deter buyers, undermining the opportunity to capitalise on this demand.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |