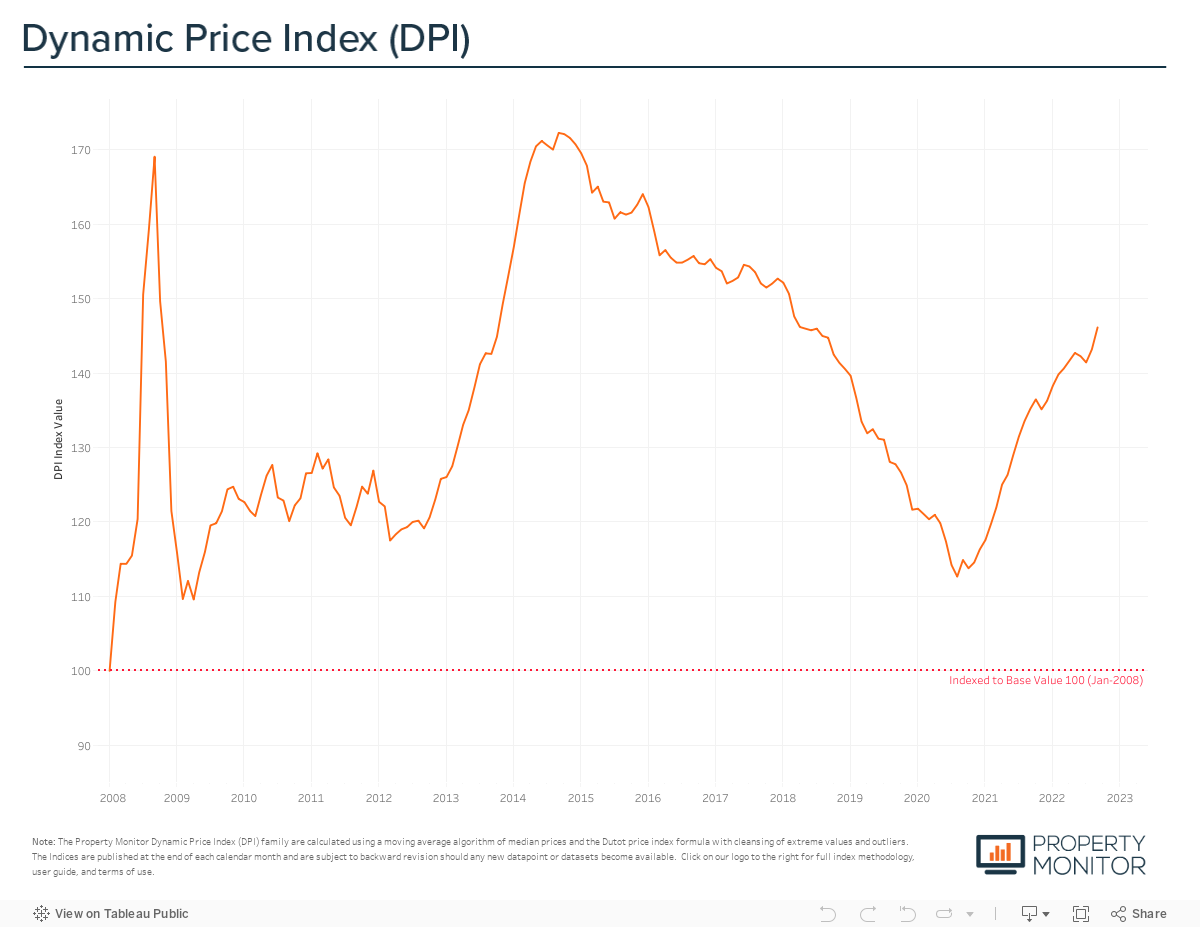

After the post-pandemic rapid pace of price appreciation slowing down over the past year, Dubai property prices surged by just over 2% in September. Property values now stand at AED 1,047 per sq ft according to the Property Monitor Dynamic Price Index (DPI), a level not seen since April 2018 when the market was enduring a period of a long market downturn.

After reaching a peak growth rate of 2.51% in April 2021 monthly price appreciation slowed, progressively tapering down to small, sub 1% incremental ups and downs and a 12-month moving average of +0.7%. As previously reported, this is a much-welcomed sign of a market that is trending towards price stability and sustainable long-term growth.

Wilst the jump in September runs contrary to this outlook, a deeper and more granular look at the price increases at property type and community level shows that apartment sales, particularly those in Arjan, Business Bay, and Dubai Residence Complex, increased at significant pace and have contributed to the uptick in September. With this in mind, the sudden bump in September is likely a second phase of the market upcycle that is being driven by recovery in apartment prices as the villa and townhouse market continues to plateau after storming ahead and leading the recovery from the bottom of the market 23 months ago.

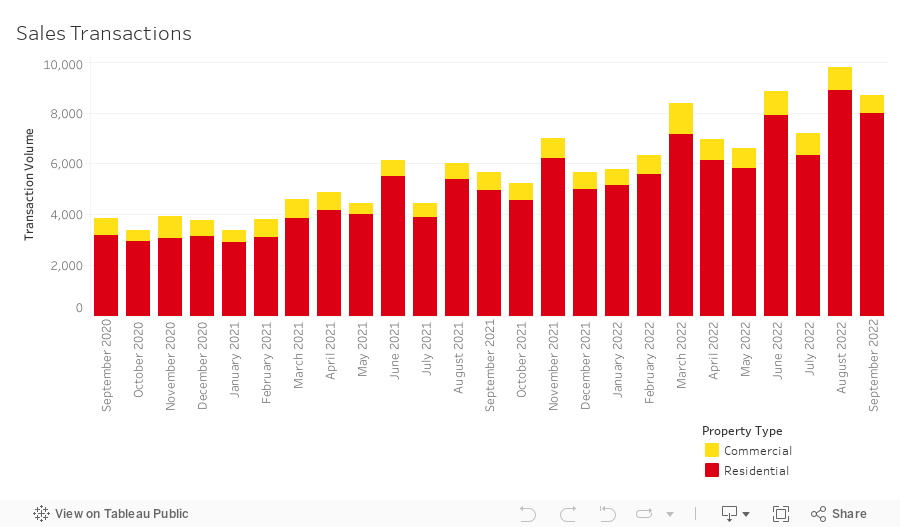

While property prices have increased, and year to date transactions have already eclipsed the whole of 2021, the total volume of sales transactions actually fell back, declining by 11.1% month-on-month to 8,686 registrations. Residential transactions—those for apartments, townhouses, and villas—accounted for 91.9% (7,979 sales transactions) of the total, with hotel apartments (3.2%), office (2%), and land sales (1.8%) being the highest transacted commercial property types. However, in a sign of continuing strength, transactions for the month still reached a level that marks the strongest September on record and the third highest month this year behind those record-breaking months in August and June 2022.

Year-to-date there have been 68,612 transactions registered (88.8% of which were residential), an increase of 114.8% over the three quarters of last year and equal to 111.9% of the entire annual transaction volume of 2021. At the current annualised pace, sales transaction volumes will reach just over 90,000 and record the second highest year in Dubai market history.

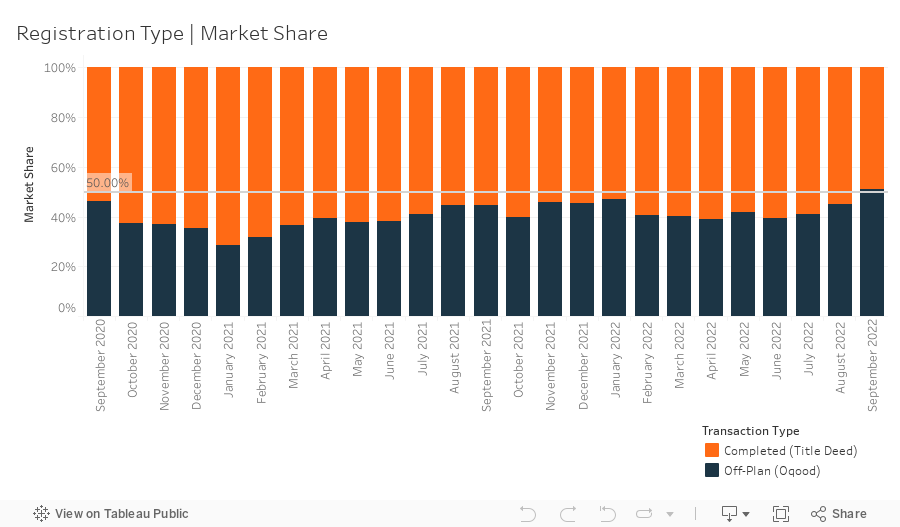

A total of 4,447 off-plan Oqood transactions were registered in September, increasing by just under 1% month-on-month however by 76% on a yearly basis. Meanwhile, Title Deed sale volumes significantly decreased for the month with transactions shrinking by 21%. Oqood registrations now represent 51.2% market share rising from 45.1% last month and reaching their highest level since May 2020. While initial Oqood registrations are often considered representative of the off-plan market, several off-plan villa and townhouse transactions—for properties that are under construction—are registered as title deed transactions for parcels of ‘land’ by the Dubai Land Department. If we adjust for these registration technicalities the accurate breakdown of market share is 60.1% in favour of properties under construction having been sold off-plan. This is a significant milestone and a reversal of the market trend—favoring ready property—that began following the gradual lifting of COVID-19 movement restrictions.

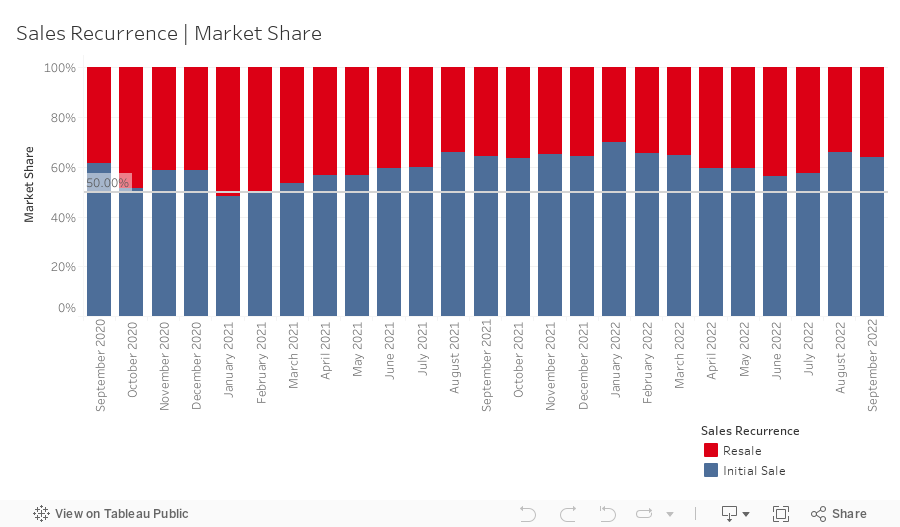

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 3,123 in September representing a market share of 36.0%, edging up 1.9% month-on-month. While up slightly on a monthly basis, resale’s market share remains on an overall slowdown which given the growing strength in the off-plan market—which is largely initial sales driven—will continue in the coming months.

New off-plan development project launches soared in September adding a further 3,633 units to the market for sale at an anticipated combined gross sales value of ~AED 8.93 billion. Apartments represent 90.9% by volume of this new inventory while townhouses and villas represent 7.4% and 1.7% respectively. High-end projects—those with price per square foot sales values between the 85th to 94thpercentile—accounted for 53.7% of new launches, and Ultra-luxury projects—those with price per square foot sales values above the 97th percentile—accounted for an additional 32.1% of new launches, demonstrate that several developers are keen to capture the rapid rise in demand at the upper end of the market. Year-to-date new project launches are just shy of 33,500 units and nearly AED 92 billion in aggregate sales value.

After momentarily increasing last month, mortgages volumes decreased 8.7% in September with a total of 1,970 loans recorded. This is in line with expectations as September also marked the month of the US Federal Reserve’s third 75 basis-point increase in the Fed Funds Rate, and subsequently the same increase in the local UAE overnight deposit facility (ODF) to a base rate of 3.15%.

This now puts the average 3-year fixed rate mortgage at 4.49%, 2% higher than just one year ago. What this means for the average borrower is that for every AED 1m of loan value, their monthly mortgage repayments would be approximately AED 1,072 higher relative to the rates available last year.

Breaking down the mortgage market further, shows that 39.6% of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.66m at a loan-to-value ratio of 77.2%. A further 45.2% of loans (up 2.6% from last month) were for refinancing, while the remaining 15.2% of loans (down 1% from last month) were bulk mortgage registrations—those taken by developers and larger investors with multiple units. These bulk registrations were spread across several projects, most notably Al Barari (AED 190M), FIVE Jumeirah Village (AED 161M), and Lakeview Apartments in Green Community (AED 37M).

In September, Emirate-wide average gross rental yields grew by 0.25% to 6.51%, with yields for all three residential property types increasing: apartments up by 0.09% to 6.90%, townhouses up by 0.14% to 5.78%, and villas up by 0.04 to 5.08%. Yields for residential properties have now reached pre-pandemic levels and match those last seen back in July 2019. This comes as no surprise, given that vacancy rates continue to trend lower, and many would-be homebuyers are forced to turn to the rental market as purchasing is put further out of reach for many owing to the nearly two year run of property price appreciation and an increasingly unfavorable mortgage interest rate environment. We expect to see further upwards pressure on rental rates in the coming months, with the only respite in sight being tied to the handover of projects that are nearing completion.

As we enter the fourth quarter, we predict that the Dubai property market, and its various community sub-markets, will continue their divergence with two main markets running in parallel—new development off-plan sales market, and the completed / resale property market. The health and prospects of these two main markets will be further differentiated and separated by unit typology—apartments, townhouses, and villas. It won’t be a one size fits all market and a rising tide of slow and steady price appreciation will not lift all boats by an equal amount.

The completed and resale property market will likely see transacted sales prices for townhouses and villas stabilise with some level of negotiability on asking prices emerge, while apartments in tier 1 and tier 2 communities are expected to see additional price growth after trailing their single-family counterparts thus far. The most significant headwind for the resale market ultimately remains affordability and international demand factors, centered around the trajectory of interest rates and recession in developed markets. We foresee rates continuing to rise well into the first two quarters of next year.

Meanwhile, in our view, the outlook for the new development sales market will continue its resurgence and maintain leading market share with an increasing number of end-users and investors opting to purchase off-plan. The extent to which the off-plan market continues to grow and remain attractive to buyers will rely largely on the pressures and headwinds facing the completed and resale property market remaining constant, as well as developers ensuring that their pipeline of units adequately reflects the demand of buyers. Developers will need to pay particular attention to the shortage of certain property types across the spectrum of price points. With the majority of new project launches currently favoring apartments in the upper end price tiers there may be a gap already emerging, one which is hopefully grasped as an opportunity and acted on.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |