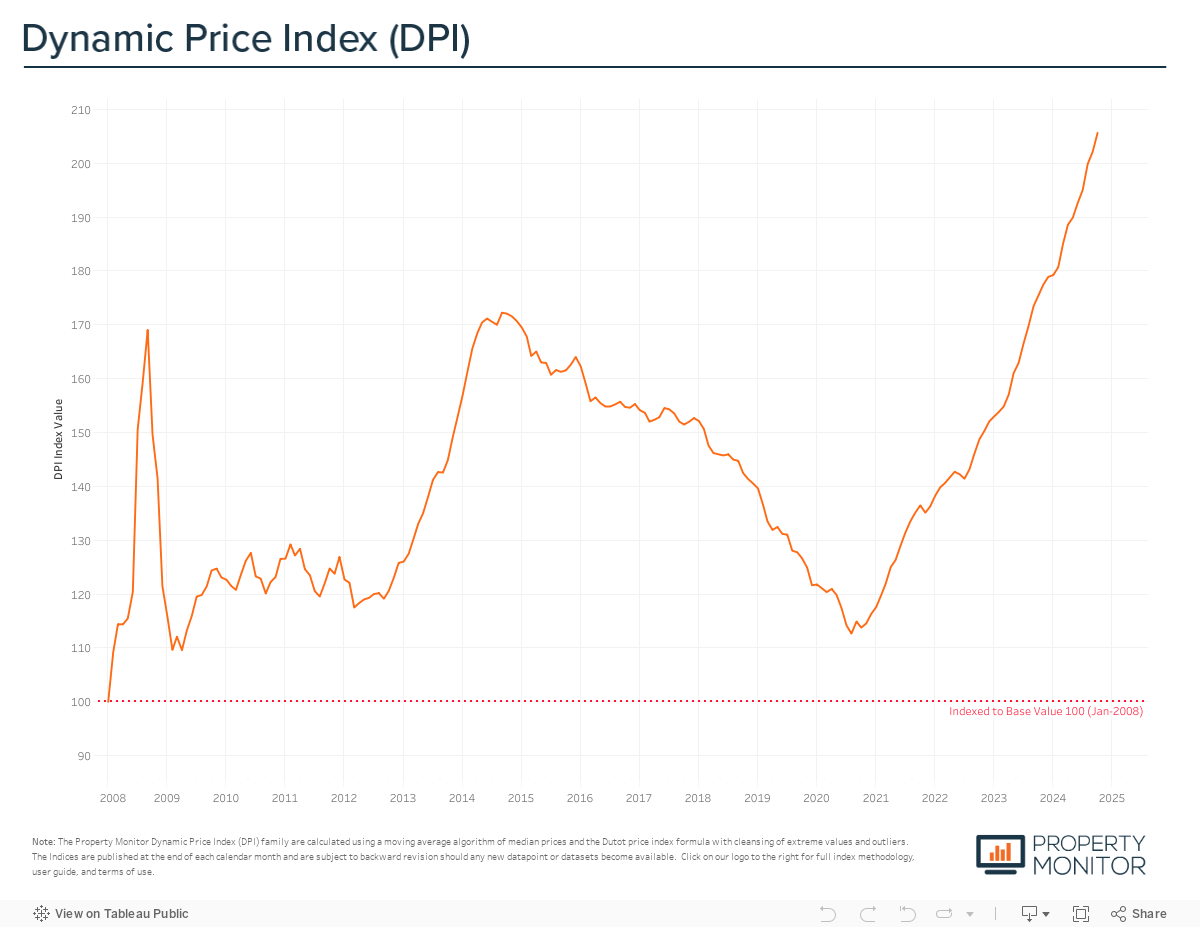

Four years after finding the bottom of the market, Dubai property prices have gone on to appreciate nearly 60%, increasing 1.73% in October. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices grew by 1.73% in October and currently stand at AED 1,473 per square foot, 19.4% over the previous all-time high and market peak of September 2014. The upward phases (recovery and growth) of the current market cycle have spanned 48 months so far, with prices increasing at a moderate rate of 1.24% per month on average. In contrast to the previous market cycle—one that experienced a period of aggressive price increases in excess of 2% per month—which lasted only 24-months and saw average monthly appreciation of 1.6%, what we are experiencing now shows greater signs of stability with less speculative activity. Barring any major disruptions, this trend appears likely to carry on well into the new year.

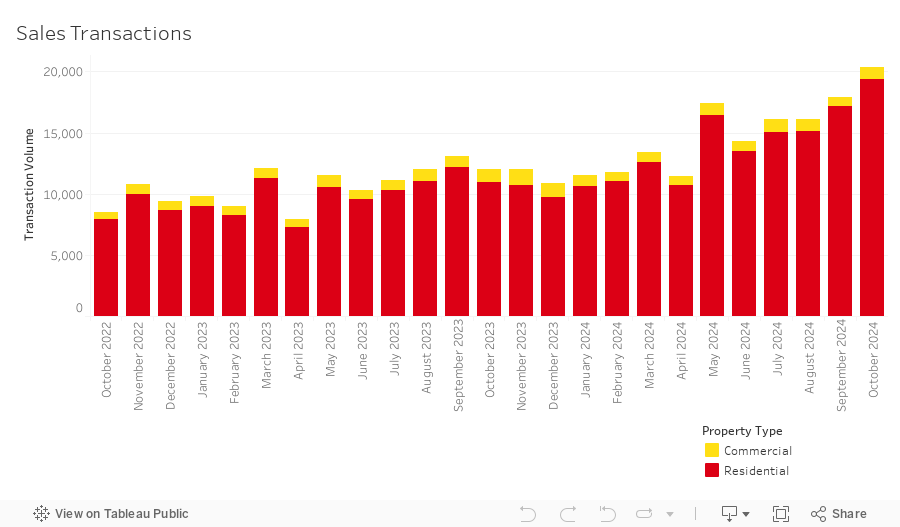

October shattered records with a notable 13.4% increase in sales transactions, soaring to an unprecedented 20,460 deals. Not only did this mark the highest October sales volume ever, but it set yet another all-time monthly record. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 94.9% (17,151 transactions). The highest transacted commercial property types were office spaces (1.5%), hotel apartments (1.04%), and vacant land (0.91%).

Annual sales transaction volumes have now surpassed 151,000 and have eclipsed 2023 year-end sales by 13.4%. With two months remaining, we are on track to see a year-on-year increase of over 30% (~175,000 sales) and a redefining of what’s possible in the Dubai market. This phenomenal growth and overall trajectory of market activity will provide a solid footing for achieving the ambitious objectives of the Dubai Real Estate Sector Strategy 2033, which calls for real estate transactions to grow by 70%, raising the overall market value to AED 1 trillion.

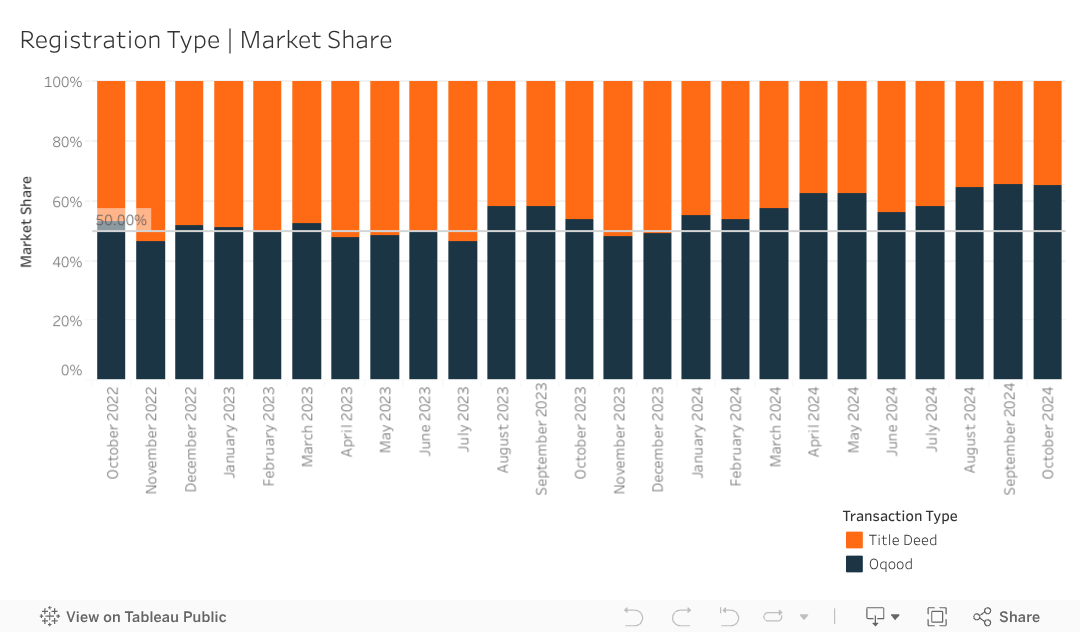

In October, 13,316 off-plan Oqood transactions were recorded, an increase of 12.7% from the previous month and a minor decrease in market share falling to 65.1%. Meanwhile, Title Deed sale volumes also witnessed an increase, growing by 14.7% and now account for 34.9% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, offplan transactions secure an even larger market share of 72.6%.

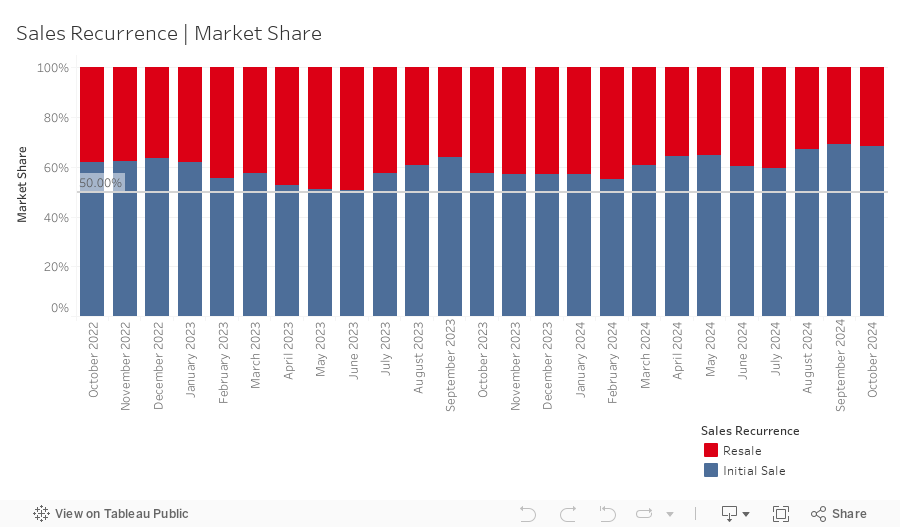

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 6,392 in October representing a market share of 31.2%, decreasing by 0.2% month-on-month. While overall resale activity decreased, the portion of off-plan resales increased 1.2% to 27.1% and registered as the highest level of the current market cycle. Off-plan resale activity has seen a steady yet gradual rise over the past three years. However, as in previous months, the bulk of these resales are concentrated in properties nearing completion within the year, suggesting a healthy demand rather than purely speculative trading.

Preliminary figures for October indicate the introduction of 48 new residential projects with over 15,000 off-plan units added to the market. This contributes to an already record-breaking total of approximately 99,000 units across over 343 projects this year. The growing number of active developers in the market has led to a much broader diversity in product offerings. While 2023’s launches were largely concentrated in the luxury and ultra-luxury segments, 2024 has brought projects across a wider spectrum of price ranges. With over 250 additional projects in the planning phases being tracked by the Property Monitor team, we anticipate that new launches will maintain historically high levels throughout the remainder of 2024 and well into 2025.

Mortgage activity surged in October, reflecting the broader rise in sales transactions. The number of registered loans hit an all-time high of 4,318, marking a 3.26% increase from September and a 1.34% rise over the previous record. This uptick in mortgage activity aligns with recent interest rate easing, making financing more accessible and attractive for buyers. Notably, mortgage penetration for completed properties reached 36.3% this month, a substantial increase from 28.3% at the same time last year, underscoring a growing reliance on financing in the market. During the month, loans taken for new purchase money mortgages accounted for 48.2% (up 3.8% from last month) of borrowing activity, with the average amount borrowed being AED 1.75m at a loan-to-value ratio of 76.5%. Meanwhile, loans for refinancing and equity release saw their market share decrease by 1.2% to 33.3%. The remaining 18.5% (down by 2.6% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 798 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Marriott Residences (325) in Dubai Science Park, Canal Front Residences CF3 and CF4 (92), and Rokane G25 (89) in Jumeirah Village Circle, as well as portfolio mortgage modifications at Micase Avenue (62) in Al Furjan.

As we move through the year’s final quarter, closing out an exceptionally strong phase for the Dubai real estate market, we anticipate continued overall market health. However, a gradual slowdown in transaction volumes is likely. With new development project launches showing no signs of deceleration, monitoring the absorption of this fresh inventory will be crucial. While data suggests that the market has so far managed to accommodate the high influx of new units, almost every market cycle eventually shifts from growth to decline due to a supplydemand imbalance, often triggered by an oversupply. By year’s end, close to 135,000 new residential units are expected to have entered the market for sale—a record pace that will require commensurate growth in population and economic activity by the time these units are handed over.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |