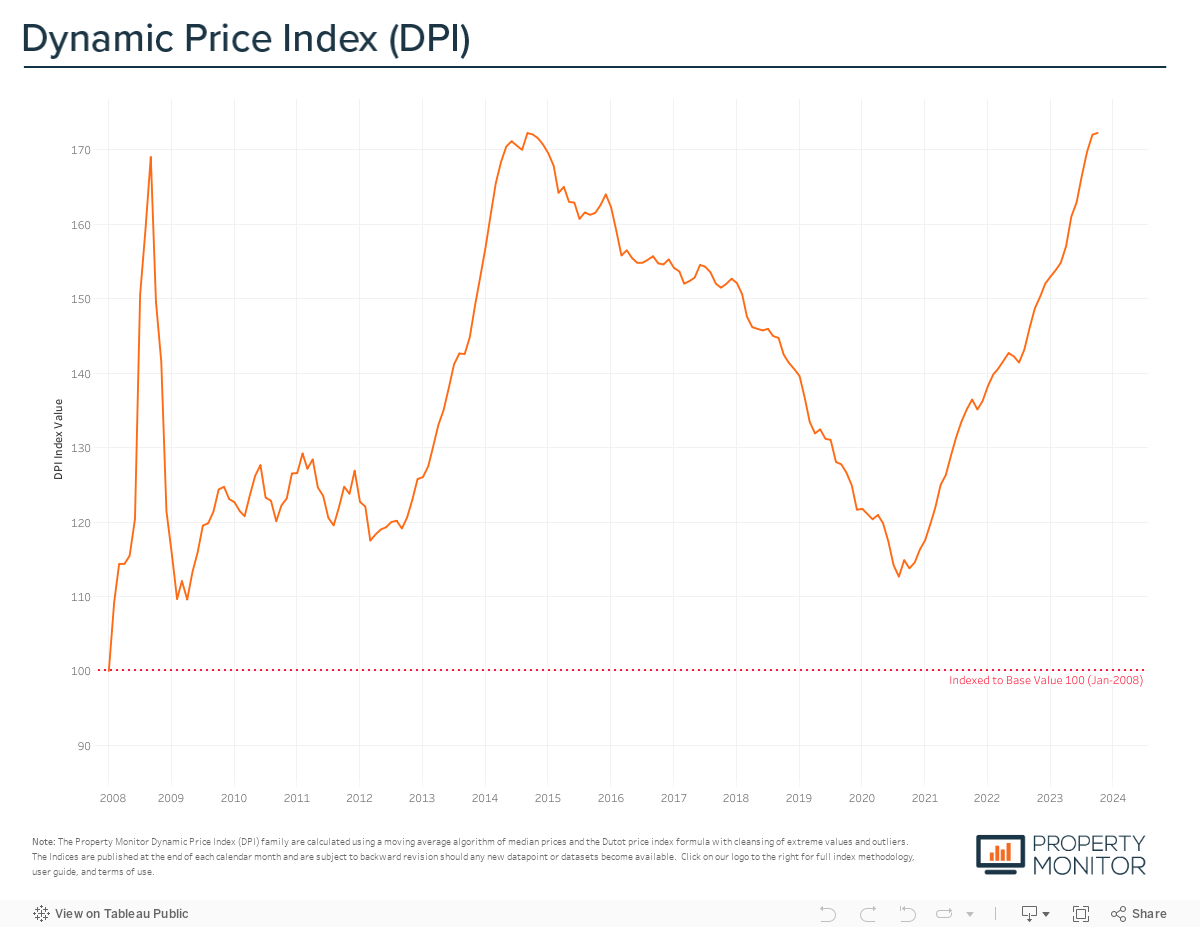

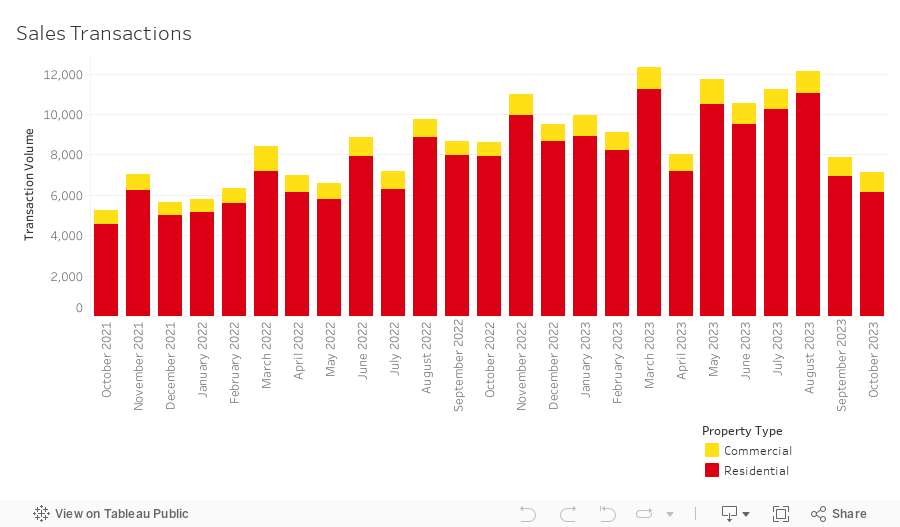

While price appreciation continues to climb, the total volume of sales transactions witnessed a second month of notable declines, down 9.2% month-on-month and falling to a total of 7,123 sales. This is the lowest level since May 2022, a time when we were just coming out of COVID-19 mobility restrictions and the ability to transact had been diminished. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 86.2% (6,142 transactions). The highest transacted commercial property types were hotel apartments (4.4%), land sales (4.0%), and office spaces (3.4%).

Year-to-date there have been 100,029 sales transactions recorded, a 29.5% increase over the same period last year and reaching a level that marks a new annual record for the Dubai market. We continue to anticipate that we’ll see over 120,000 sales registered by the end of the year, although the significant decline in total sales transactions in recent months could, when taken at face value, lead many to believe this will not be the case.

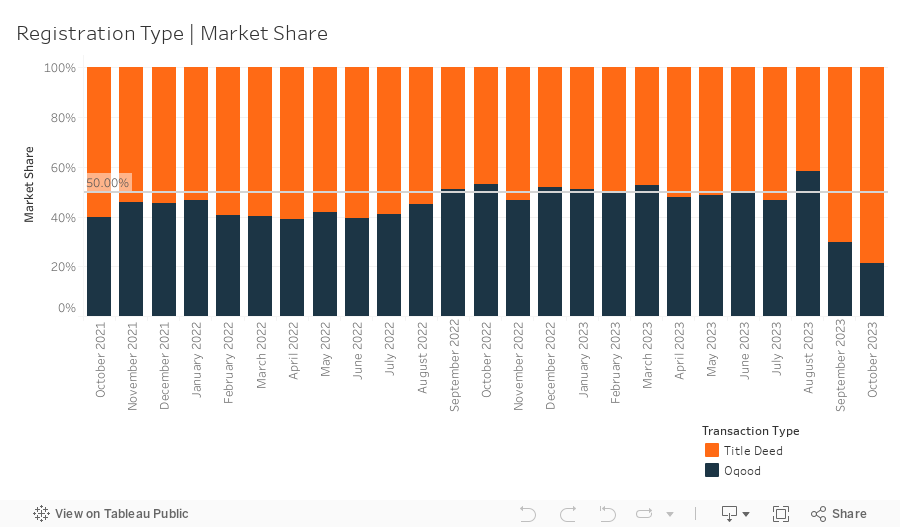

Over the past 2 months, the volume of transactions posted by the Dubai Land Department (DLD) has declined by almost a third, from a monthly average of ~10,500 sales to just over 7,000. A deeper analysis into this decline looking at the type of registration—either Oqood which is largely representative of initial off-plan developer sales, or Title Deed which in most cases would represent the sale of completed properties—shows that the drop off has only occurred in Oqood registrations, with Title Deed sales remaining relatively constant at over 5,000 sales per month. A default reaction to this could be to assume that demand in the off-plan market has weakened, however from both quantitative and qualitative evidence obtained directly from the market’s biggest developers and leading brokerages, it can easily be argued that the data is incomplete or suffering from an unusual delay.

With consistent new development project launches and the sale of offplan properties being significant drivers for the record high transaction activity experienced this year, it’s hard to imagine that the winds that have been driving this market segment could be sucked out almost instantaneously.

While there is a lag between the time a developer commences sales to those deals being registered—a 60-day grace period permitted by the DLD—it’s not enough alone to account for such a dramatic, simultaneous, wide-reaching reduction across the off-plan market. The Property Monitor team has been looking into this and at this stage, we do not believe that there is cause for concern—in all likelihood, the level of off-plan sales has not declined to any material extent indicative of a market shift. We expect to see the pending transactions appear in the registrar’s data over the coming months, and if developers’ behavior is any indication, it will be for a large amount of deals that have already been signed, and then some.

New off-plan development project launches remain at record highs, with just over 11,500 off-plan units added to the market for sale with an anticipated combined gross sales value of ~AED 25 billion. Apartments represent 81.2% by volume of this new inventory, while townhouses and villas represent 17.2% and 1.6% respectively. Yearto-date, new project launches have exceeded just over 77,000 units and AED 230 billion in aggregate sales value, eclipsing the 2022 yearend numbers by more than 20,000 units and AED 70 billion in value. With over 100 additional projects in the planning phases being tracked by the Property Monitor team, we anticipate that new launches will maintain their historically high levels for at least the remainder of the year and well into 2024.

Mortgage transaction volumes decreased by 16.1% in October with a total of 2,706 loans recorded. Bulk mortgage loans mortgages—those taken by developers and larger investors with multiple units—were a significant attributor to this decrease, seeing their market share shrink by 20.1% to 9.6%. The 259 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations in Qsar Sabah (114) in Dubai Production City, Majestic 1 (57) in International City II, and Burlington Tower (11) in Business Bay.

Meanwhile, loans for refinancing and equity release saw their market share increase by 10.7% to 41.5%. The remaining 48.9% (up 9.4% from last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.78m at a loan-tovalue ratio of 75.7%. Loans for new purchases and refinancing remain at historically high levels across all residential property types, this indicates continued strength in the overall mortgage market despite relatively high interest rates.

Average gross rental yields for residential properties in the Emirate continued to remain relatively stable in October, decreasing by just 0.04% to 6.67%. Yields for all three residential property types saw modest declines with apartments down 0.05% to 7.0%, townhouses down 0.11% to 6.41%, and villas down 0.02% to 4.96%. The marginal shifts in yields and general plateauing align with our forecasts, largely due to several communities seemingly hitting the peak in attainable rental rates, and sales prices leveling off at the same time in certain areas. With numerous new development projects edging towards completion, the rental market is poised to see an increase in available inventory in the coming months and with that we should also see a gradual decrease in rents going in 2024.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |