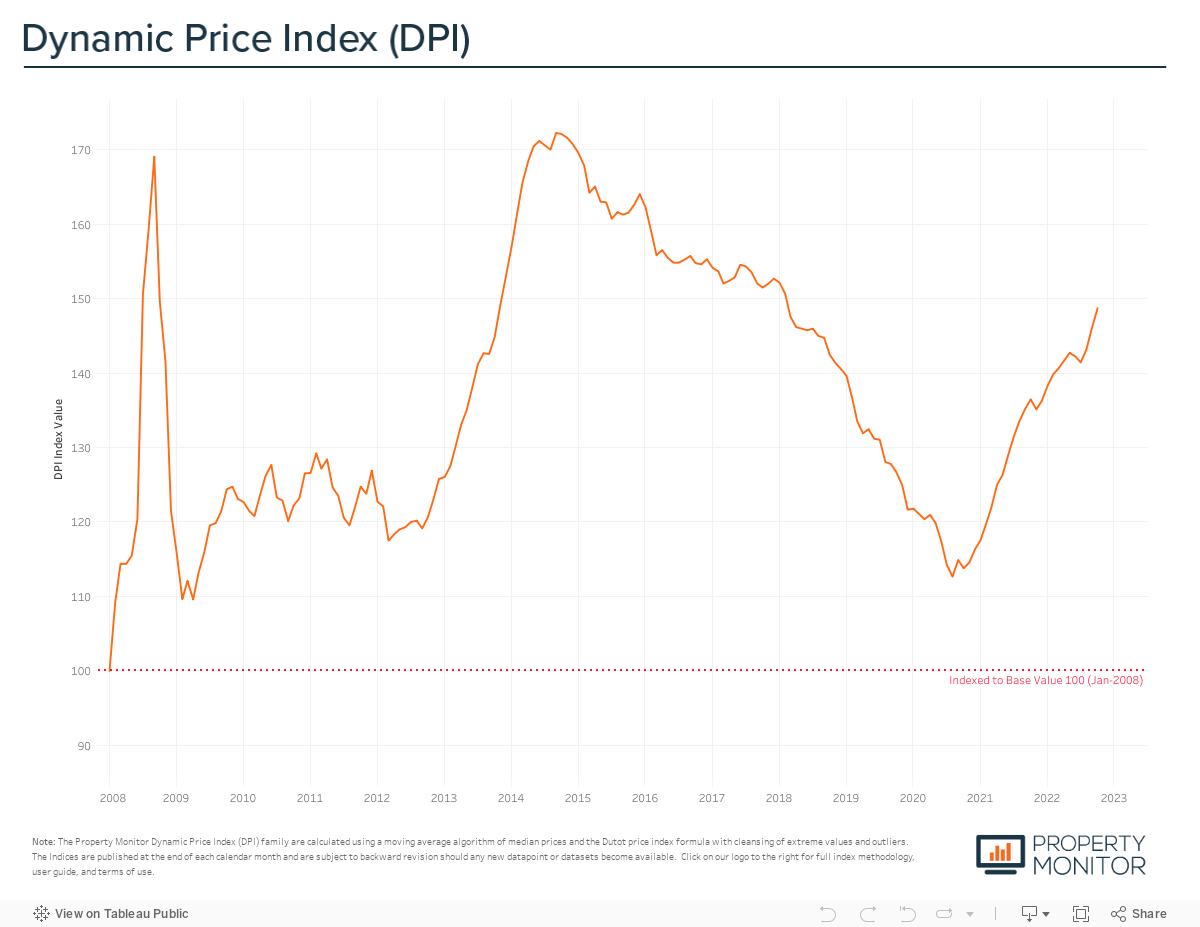

The pace of price appreciation in the Dubai property market continued to power on with surprising strength last month, recording a 1.77% increase in October. Dubai property values now stand at AED 1,065 per sq ft according to the Property Monitor Dynamic Price Index (DPI), a level not seen since the time of the last market upswing in November 2013 and then re-visited later in March 2018 on the way back down, in the subsequent steep and pro-longed downturn. The current market problems in North America, China and Europe and currently not affecting the Gulf where demand remains robust despite the rising interest rates as a consequence of the dollar-dirham peg.

Following on from the 2.06% increase last month–which was the highest monthly growth rate since mid-2021–this latest continued evidence of strong upward price pressure posted in October appears to be the formation of a trend, that points to a second wave of price appreciation. This is being driven by the recovery in apartment prices, particularly those in Dubai Studio City, Business Bay, Palm Jumeirah, and City Walk. This second phase of growth comes as we reach a point 24 months since the market bottomed out in late 2020. It can be seen as a significant milestone as 24 months was the total duration of the previous market recovery and growth phases, before entering a long 6-year down cycle. It’s important to note that no two market cycles are the same. Our analysis indicates that we are witnessing a multi-phase cycle, with each phase being driven by different market segments combined with more moderate price appreciation compared to the previous 2 year 2013-2014 upcycle. We believe this will likely result in a more sustainable and longer growth period that extends into mid-late 2023.

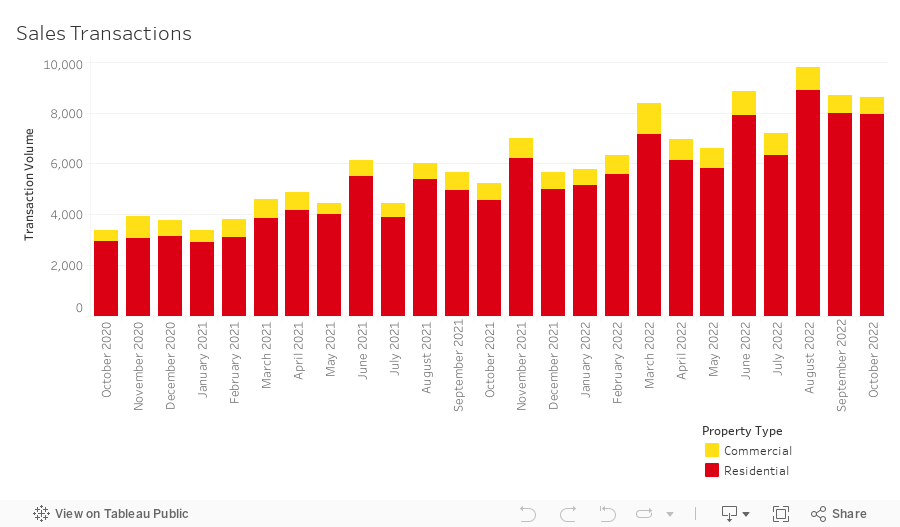

While monthly property price growth continues, the volume of sales transactions remains at par with last month, declining a mere 0.7% to 8,626 registrations. Residential transactions—those for apartments, townhouses, and villas—accounted for 92% (7,935 sales transactions) of the total, with hotel apartments (3.4%), office (1.9%), and land sales (1.7%) being the highest transacted commercial property types.

Year-to-date there have been 77,238 transactions registered (89.2% of which were residential) equal to 126% of the entire annual transaction volume of 2021. At the current annualised pace, sales transaction volumes will reach just over 92,000 and record the second highest year in Dubai market history. In a year where nearly every month sales volumes have reached historic levels–as the highest or second highest on record–the question can be asked… How much longer can the breakneck pace of sales continue?

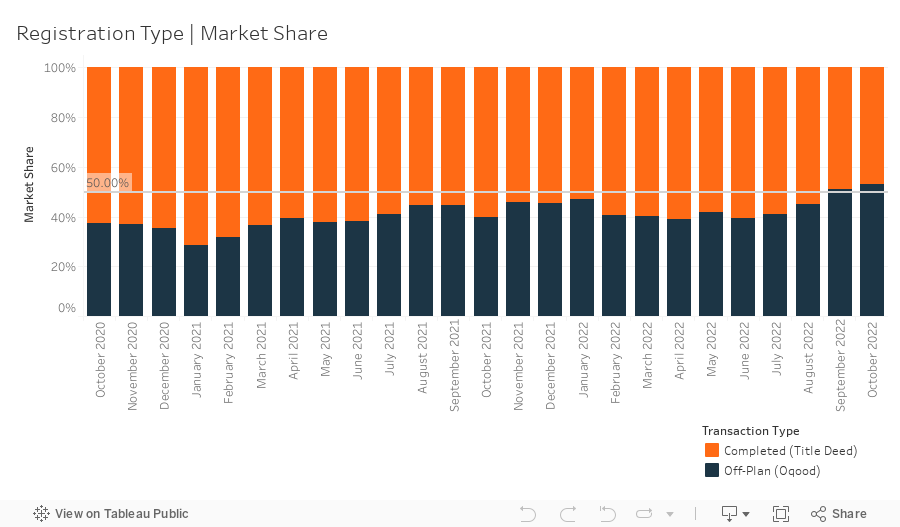

A total of 4,578 off-plan Oqood transactions were registered in October, increasing by just under 3% month-on-month however by 120.3% on a yearly basis. Meanwhile, Title Deed sale volumes continued to decrease with transactions for the month shrinking by 4.5%. Oqood registrations now represent 53.1% market share rising from 51.21% last month and remain at their highest level since May 2020, when the market share was 66.3%. While initial Oqood registrations are often considered representative of the off-plan market, several off-plan villa and townhouse transactions—for properties that are under construction—are registered as title deed transactions for parcels of ‘land’ by the Dubai Land Department. If we adjust for these registration technicalities the accurate breakdown of market share is 60.2% in favour of properties under construction having been sold off-plan.

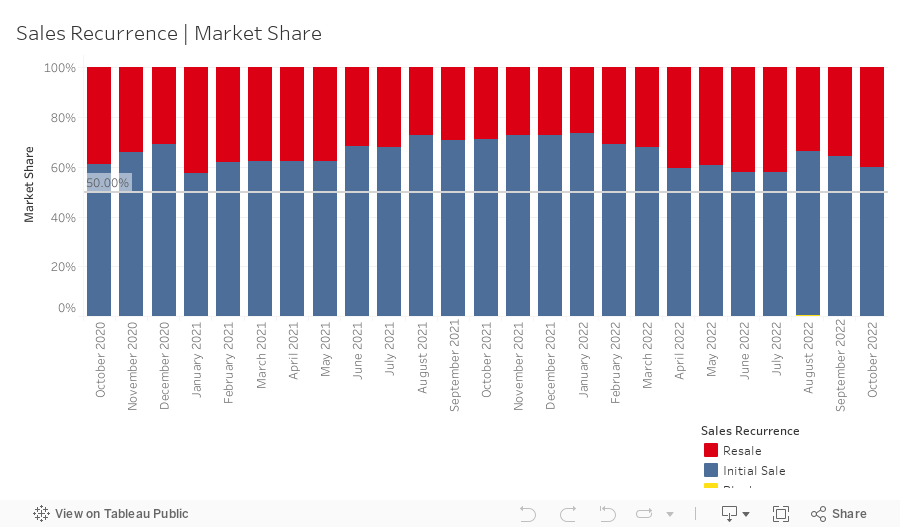

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 3,467 in October representing a market share of 40.2%, jumping 4.2% month-on-month. This jump in resale activity can be likely attributed to an increase in secondary sales of off-plan properties where the initial buyers, in most cases, are cashing out with a premium in hand. Anecdotal evidence points to the fresh buyers of these properties being those that have been unable to secure a ready property in their desired price range, and who have less of an appetite to wait for the delivery of one of the many newly launched projects from this year. While up on a monthly basis, resale’s market share remains on an overall slowdown which, unless the resale activity of off-plan projects continues, will progress further in the coming months.

New off-plan development project launches soared in October adding a further 3,431 units to the market for sale at an anticipated combined gross sales value of ~AED 12.3 billion. Apartments represent 56% by volume of this new inventory while townhouses and villas represent 31.3% and 12.6% respectively. Year-to-date new project launches are just shy of 37,000 units and have surpassed AED 104 billion in aggregate sales value.

In October mortgage transaction volumes spiked to their highest level since September 2021, reaching 2,386 loan registrations for the month. In the face of ever-increasing interest rates and borrowing costs this comes as a surprise and only upon deeper investigation makes sense. During the month there was a considerable increase in the amount bulk mortgage registrations—those taken by developers and larger investors with multiple units—representing 35.8% of all loans for the month up 20.6% month-on-month. These bulk registrations are often portfolio loans and mortgage transfers, and while containing multiple properties as a single transaction are recorded separately thereby driving the transaction count higher. Over 800 such loans were recorded in October with the bulk of registrations spread across several projects, most notably 330 transactions in Al Barari (AED 13.5B), 228 transactions at Orchid Residence in Dubai Science Park (AED 117M), 70 transactions at Orra Harbour Towers in Dubai Marina (AED 61M), and 14 transactions at the W Rediences on Palm Jumeirah (AED 393M).

Breaking down the mortgage market further, shows that 20% (down from 39.6% last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.98m at a loan-to-value ratio of 77.2%. The remaining 44.2% of loans (down 1% from last month) were for refinancing or equity releases.

In October, Emirate-wide average gross rental yields held firm at 6.50%, down by a mere 0.01% month-on-month, with yields for apartments down by 0.04% to 6.87%, townhouses up by 0.19% to 5.97%, and villas up by 0.03 to 5.12%. Yields for residential properties remain in line with pre-pandemic levels and match those last seen back in July 2019, we expect to see further growth in yields in the short-term as vacancy rates remain low and demand remains strong. With several projects nearing completion and handover in the coming quarters, the mid-term outlook could see some cooling in rental prices and in turn put some downwards pressure on yield growth as a significant portion of demand should be absorbed.

As we move through the final quarter of the year and round out what has been an incredibly robust time for the Dubai real estate market, we predict that the market will remain healthy. However, we inevitably foresee transaction volumes slowing, particularly in the completed segment of the market. With no current signs of a slowdown in new development project launches, the uptake of this new inventory will continue to be an area that needs to be closely monitored. While the data points to a market that has so far been able to absorb the high volume of new units available, almost every market cycle is pushed from growth to decline by an imbalance in supply and demand, with supply increasing too rapidly. By the years’ end we will likely have seen close to fifty thousand new residential units enter the market for sale, a record rate which will need to be met by similar record increases in population growth and economic expansion by the time of handover. Price growth in the completed property market, coupled with rising mortgage rates, has served to cool the segment with buyer and seller expectations slowly coming closer together and resultant development of a sustainable marketplace with little concern towards oversupply. How supply across the off-plan and completed segments evolves will be central to the longevity of the Dubai’s current bull run.

There is also the wider international dimension to keep in mind. Dubai cannot be insulated forever from the current recessionary real estate trends seen elsewhere in the world, as investor sentiment is contagious. For now, however, the market powers on and 2023 seems likely to start on a positive note. Our predictions for the year ahead will take shape in the coming few weeks as we take the temperature of the market and pay close attention to the performance of some key bell-weather communities which are always in demand.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |