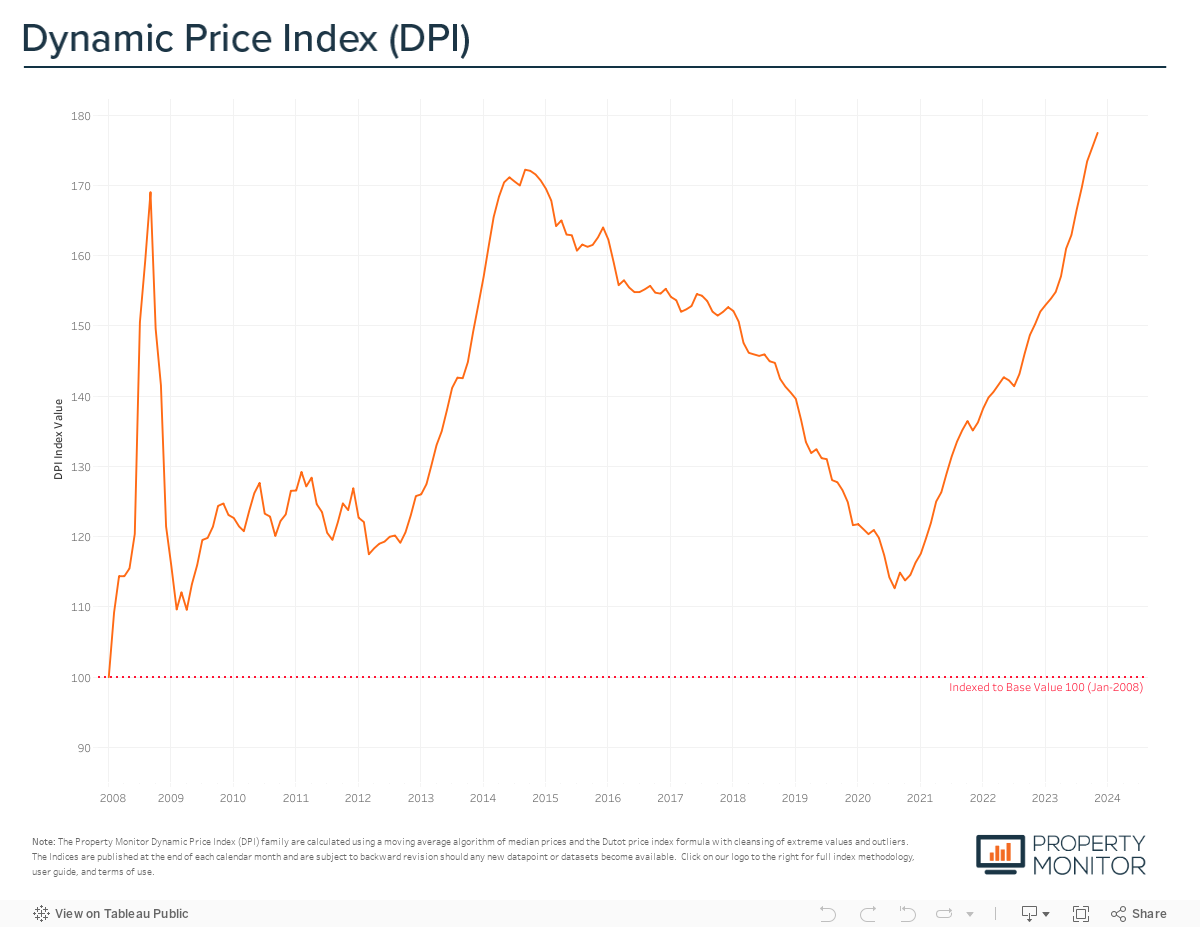

In the run up to the turn of the year, average Dubai property prices continue to reach new heights, increasing by 1.17% in November. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently stand at AED 1,271 per square foot, just over 3% above the previous all-time high and market peak of September 2014.

Since bottoming out in October 2020 prices have gone on to increase 44.9% on average, with all three residential property types experiencing varying growth trajectories. In the initial stages of the market recovery, ready single-family homes witnessed the highest demand and the steepest increase in prices with sales of comparable properties routinely achieving 5-10% above the most recent sale. Apartments—appreciating, but not at the same pace as villas and townhouses—lagged somewhat in their recovery until Q3 2022 and have since realised stronger gains while townhouses and villas have experienced muted growth appearing largely to have topped out.

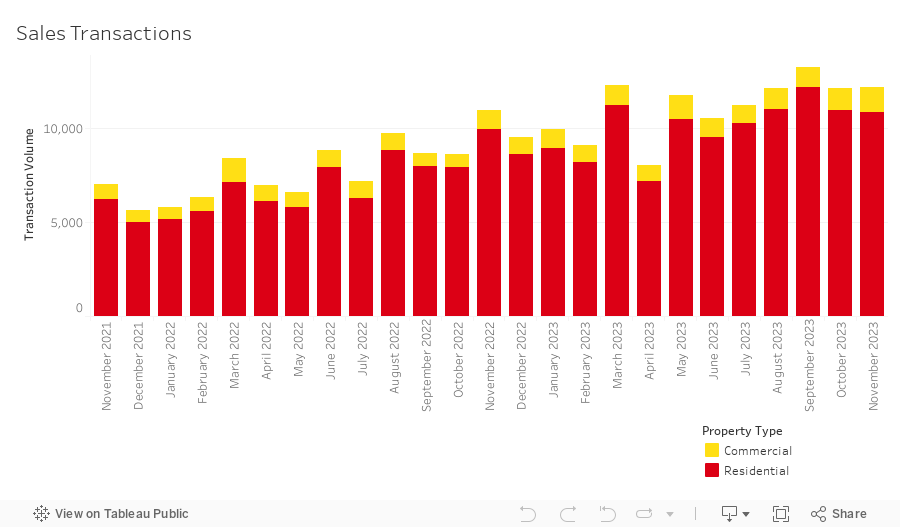

The total volume of sales transactions increased 0.75% month-on-month, reaching a total of 12,223 sales and marks the highest volume ever for the month of November. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 89.1% (10,893 transactions). The highest transacted commercial property types were land sales (4.1%), hotel apartments (3.6%), and office spaces (1.8%). Year-to-date there have been 122,657 sales transactions recorded, a 40.3% increase over the same period last year. We now anticipate that we will see over 130,000 sales registered by the end of the year, surpassing our initial expectations of 120,000 to 125,000.

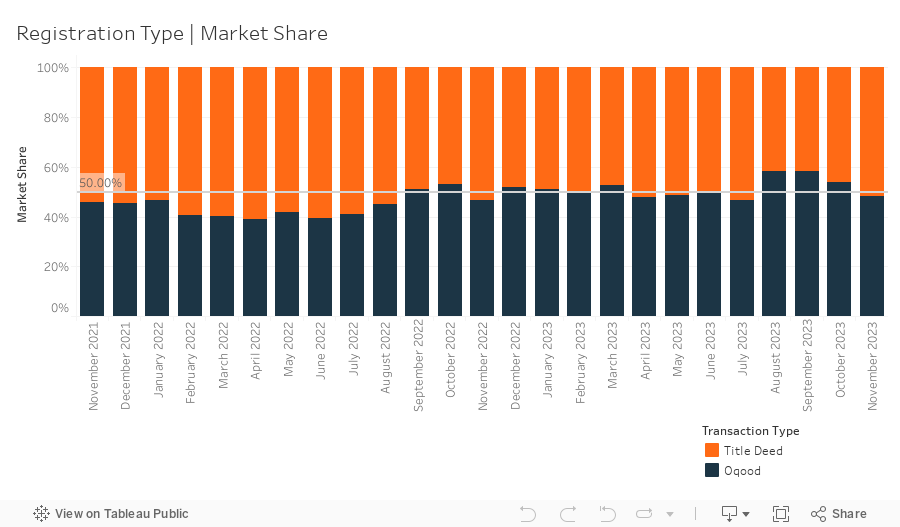

In November, a total of 5,884 off-plan Oqood transactions were registered, marking a 9.9% month-on-month decrease in volume with Oqood transactions and a 5.7% decreased in market share. Meanwhile, Title Deed sale volumes witnessed an increase rising by 12.3% and now account for 51.9% of all sales transactions. Although the market may appear to be slightly tilted in favour of completed properties over off-plan, a correctional adjustment by the Property Monitor team for registration technicalities within the Dubai Land Department (DLD), reveals that several villa and townhouse sales, presented as completed with issued Title Deeds, are indeed under construction and sold off-plan. In reality, off-plan transactions have held a dominant market share since Q4 2021, currently standing at 60.3%.

New off-plan development project launches remain at record highs, with just shy of 8,500 off-plan units added to the market for sale in November with an anticipated combined gross sales value of ~AED 19.5 billion. Apartments represent 90.9%—by volume—of this new inventory while townhouses and villas represent 6.1% and 3.0% respectively. Year-to-date, new project launches have exceeded just over 86,000 units and AED 252 billion in aggregate sales value, eclipsing the 2022 year-end numbers by nearly 33,000 units and AED 95 billion in value. With over 130 additional projects in the planning phases being tracked by the Property Monitor team, we anticipate that new launches will maintain their historically high levels well into 2024, however we do expect to see a shift in the type of product offerings, particularly a reduction in the luxury and ultra-luxury segments.

Mortgage transaction volumes increased by 7.8% in November with a total of 2,917 loans recorded. This pushed annual volumes to new heights, with more than 33,500 loans year-to-date. Bulk mortgage loans—those taken by developers and larger investors with multiple units—were a significant attributor to this increase, seeing their market share grow by 3.9% to 13.5%. The 394 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations in Siraj Tower (203) in Arjan, Rokane G22 (62) in Jumeriah Village Circle, and Al Jawhara Tower (21) in Jumeirah Village Triangle. Meanwhile, loans for refinancing and equity release saw their market share decrease by 6.4% to 35.1%. The remaining 51.4% (up 2.5% from last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.69m at a loan-to-value ratio of 75.5%. Loans for new purchases and refinancing remain at historically high levels across all residential property types, this indicates continued strength in the overall mortgage market despite relatively high interest rates.

Average gross rental yields for residential properties in the Emirate continued to remain relatively stable in November, increasing by just 0.08% to 6.68%. Yields for both villas and townhouses saw modest declines down 0.34% to 4.62% and 0.31% to 6.10% respectively, whilst yields for apartments experienced a marginal gain, up 0.24% to 7.24%. The marginal shifts in yields and general plateauing align with our forecasts, and with numerous new development projects edging towards completion the rental market is poised to see an increase in available inventory in the coming months and with that we should also see a gradual decrease in rents throughout 2024.

New off-plan development project launches remain at record highs, with just over 11,500 off-plan units added to the market for sale with an anticipated combined gross sales value of ~AED 25 billion. Apartments represent 81.2% by volume of this new inventory, while townhouses and villas represent 17.2% and 1.6% respectively. Yearto-date, new project launches have exceeded just over 77,000 units and AED 230 billion in aggregate sales value, eclipsing the 2022 yearend numbers by more than 20,000 units and AED 70 billion in value. With over 100 additional projects in the planning phases being tracked by the Property Monitor team, we anticipate that new launches will maintain their historically high levels for at least the remainder of the year and well into 2024.

Mortgage transaction volumes decreased by 16.1% in October with a total of 2,706 loans recorded. Bulk mortgage loans mortgages—those taken by developers and larger investors with multiple units—were a significant attributor to this decrease, seeing their market share shrink by 20.1% to 9.6%. The 259 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations in Qsar Sabah (114) in Dubai Production City, Majestic 1 (57) in International City II, and Burlington Tower (11) in Business Bay. Meanwhile, loans for refinancing and equity release saw their market share increase by 10.7% to 41.5%. The remaining 48.9% (up 9.4% from last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.78m at a loan-tovalue ratio of 75.7%. Loans for new purchases and refinancing remain at historically high levels across all residential property types, this indicates continued strength in the overall mortgage market despite relatively high interest rates.

Average gross rental yields for residential properties in the Emirate continued to remain relatively stable in October, decreasing by just 0.04% to 6.67%. Yields for all three residential property types saw modest declines with apartments down 0.05% to 7.0%, townhouses down 0.11% to 6.41%, and villas down 0.02% to 4.96%. The marginal shifts in yields and general plateauing align with our forecasts, largely due to several communities seemingly hitting the peak in attainable rental rates, and sales prices leveling off at the same time in certain areas. With numerous new development projects edging towards completion, the rental market is poised to see an increase in available inventory in the coming months and with that we should also see a gradual decrease in rents going in 2024.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |