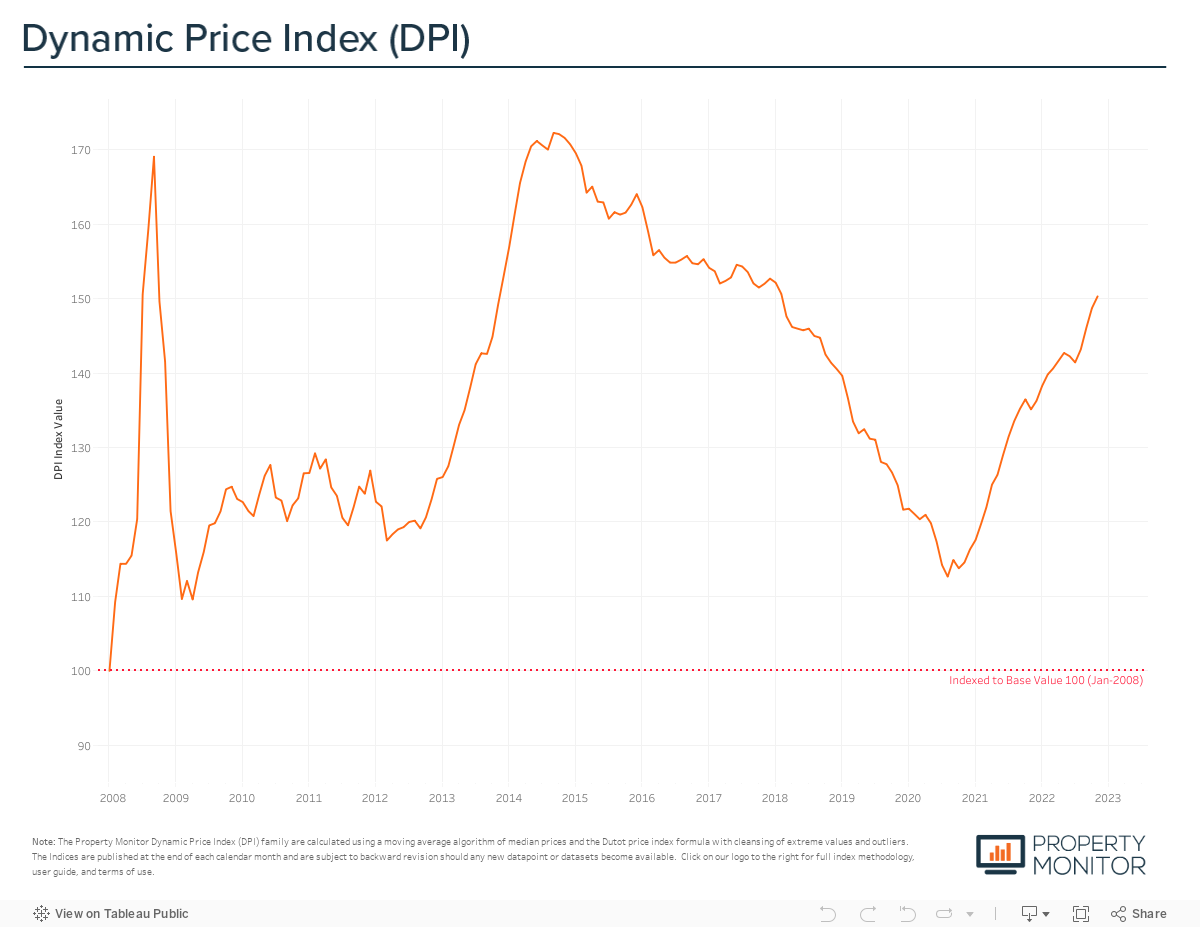

Without pausing for breath in the run up to the turn of the year, Dubai’s on-going property price growth moderated only slightly last month recording a 1.06% increase in November. Dubai property values now stand at AED 1,076 per sq ft according to the Property Monitor Dynamic Price Index (DPI), now back to a level not seen since November-December 2013 when the market was in the throes of a string upswing. Dubai now looks like a strong outlier in world markets, with North American, European, and other developed markets showing price drops despite the inflationary pressures on energy, traded goods and food prices and strongly rising interest rates.

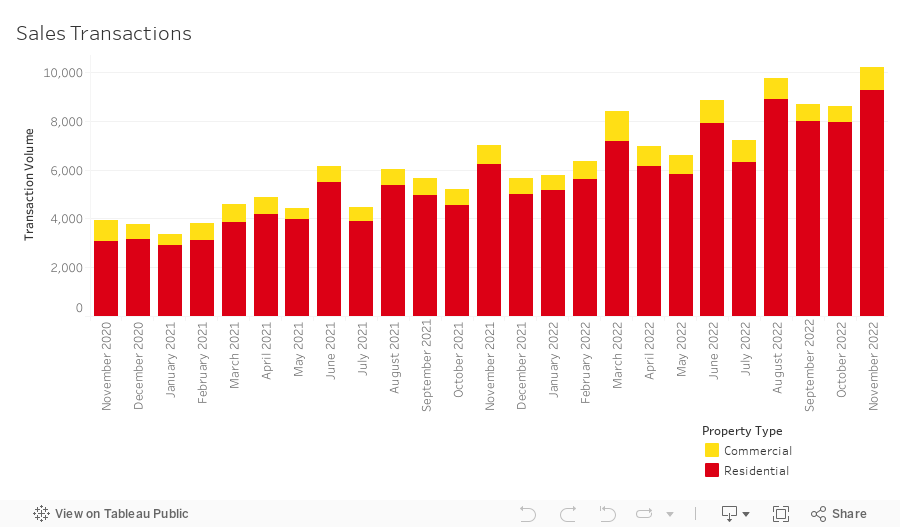

In a year where, nearly every month, sales volumes have reached historic levels it seemed only a matter of time before they would break through the 10,000 barrier. In November they did just that, registering a record November performance with 10,188 sales, evidence of strong consumer and investor demand. Residential transactions—those for apartments, townhouses, and villas—accounted for 91.1% (9,279 sales transactions) of the total, with hotel apartments (4.1%), office (2.2%), and land sales (1.8%) being the highest transacted commercial property types.

Year-to-date there have been 87,426 transactions registered (89.4% of which were residential) equal to a whopping 142.6% of the entire annual transaction volume of 2021 which at the time, we believed looked like a very decent year. At the current annualised pace, sales transaction volumes will reach just over 95,000 and record the second highest year ever witnessed in Dubai market history.

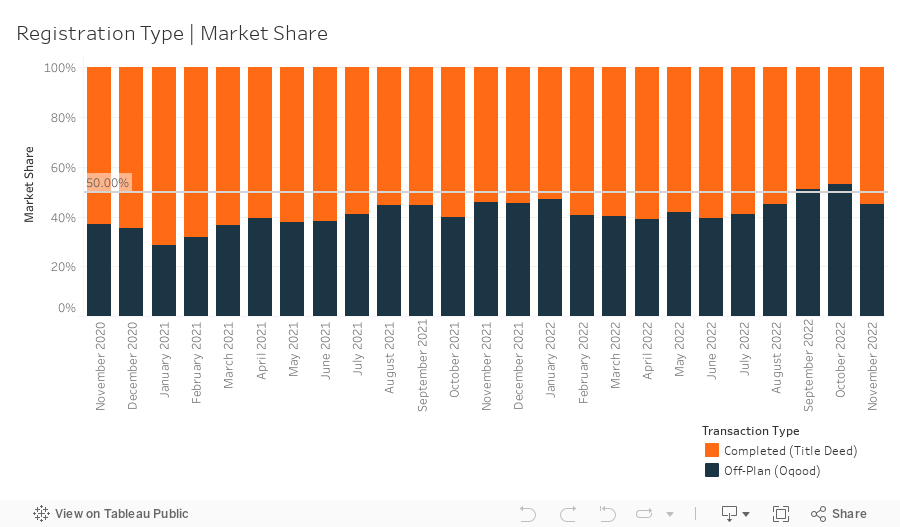

A total of 4,602 off-plan Oqood transactions were registered in November, increasing marginally by just 0.5% month-on-month however by a more robust 42.7% on a yearly basis. Meanwhile, Title Deed sale volumes again witnessed a marked increase for the month, growing by 38%. Title Deed registrations now represent 54.8% of the market, rising from their recent low of 46.9% last month. While at face value it may appear that sales of completed properties—those represented by Title Deeds—have started a resurgence, due to registration technicalities with the Dubai Land Department these numbers are unintentionally inflated and include several transactions for villas and townhouses in DAMAC Lagoons, Jebel Ali Village, and Dubai Hills, which are off-plan and under construction. When adjusted the accurate breakdown of market share is 55.2% in favour of off-plan. This market insight provided by Property Monitor experts, is important for professionals and consumers to understand when analysing the market and making key decisions.

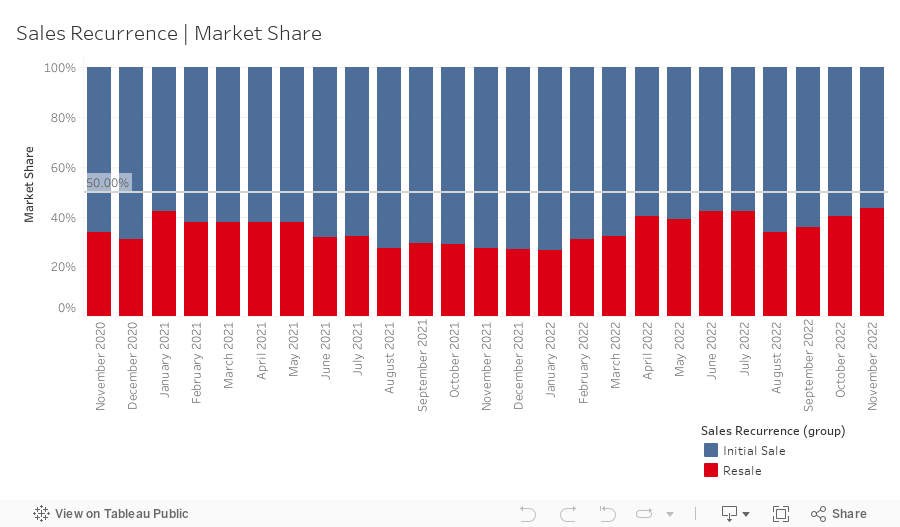

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 4,425 in November representing a market share of 43.4%, jumping 3.2% month-on-month. A growing portion (18.8%) of this jump in resale activity can be attributed to secondary sales of off-plan properties where the initial buyers, in most cases, are cashing out with a premium in hand. This may seem reminiscent of a trend which occurred in the previous market cycle where flipping and speculation towards short-term gains was rampant, however at this stage anecdotal evidence points to fortunate buyers who were presented with unplanned opportunities for a windfall and not premeditated speculative purchases. In any event, the volume of off-plan resales is an area to be closely monitored in the coming months and any significant uptick viewed as a cautionary market signal of a bubble bursting.

New off-plan development project launches reached a record monthly high in November adding a further 7,161 units to the market for sale at an anticipated combined gross sales value of ~AED 28.2 billion. Apartments represent 63.7% by volume of this new inventory while villas and townhouses represent 22.8% and 13.5% respectively. Year-to-date new project launches have exceeded just over 44,000 units and AED 132.5 billion in aggregate sales value.

After spiking to their highest level since September 2021 last month, mortgage transaction volumes declined slightly in November (down 2.9%), registering 2,317 loans for the month (with a total value of ~AED 18 billion), however, remain unexpectedly high given the current interest rate environment and ever-increasing borrowing costs. As with previous months a deeper investigation into these transactions gives better context to the eye-opening headline numbers and reveals that over AED 11 billion (~61% by value) of loans can be attributed to the Nakheel’s strategic financing deal with Mashreq Bank, Dubai Islamic Bank and Emirates NBD, that is earmarked for a new phase of growth including the relaunch of Palm Jebel Ali as well as the Dubai Islands (Deira Islands) project. Additionally, a high number of loans were recorded under government initiatives for Emiratis where interest rates have a negligible effect on borrowing.

Breaking down the mortgage market further, shows that 37.7% of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.68m at a loan-to-value ratio of 77.7%. A further 38.7% of loans (down 5.56% from last month) were for refinancing or equity releases, while the remaining 23.6% of loans (down 12.2% from last month) were bulk mortgage registrations—those taken by developers and larger investors with multiple units. These bulk registrations were spread across several projects, most notably FIVE Jumeirah Village where 238 hotel apartment units were recorded in a mortgage portfolio modification for a total of AED 313m.

In November, Emirate-wide average gross rental yields continued to hold firm at 6.53%, up by 0.03% month-on-month, with yields for all three residential property types increasing: townhouses up by 0.09% to 6.06%, apartments up by 0.04% to 6.91%, and villas up by 0.02 to 5.14%. Yields for residential properties remain in line with pre-pandemic levels and have begun to show signs of plateauing out. With several projects nearing completion and handover in the early part of the new year, it is likely that we will witness rental prices cool off, particularly in the apartment market, and in turn put some downwards pressure on yield growth.

With the end of the year in sight and taking a step back to see how the market has performed in 2022, it would be fair to say that it has outperformed nearly all expectations. From the bottom of the market, which we called just two years ago, prices have appreciated just over 28%, an average of 1.12% per month, and over the last 12 months at an average of 0.89%. This pace of price appreciation, notably the diminishing monthly rate, can be viewed as a positive sign of a market that is losing some of the post-pandemic built-up steam, but overall trending towards sustainable price growth. At the same time, transaction volumes have averaged 6,258 per month since the start of the recovery and 7,757 per month over the last 12 months. Comparing this to the previous market recovery and growth phases—a period that ran the course of 24 months and ended in April 2014—where a monthly average of 5,155 transactions occurred (21.4% fewer than this market cycle) it raises the question of how long can sales volumes remain at such an aggressive pace? Some of the drivers behind this can be attributed to the ongoing conflict between the Ukraine and Russia, and subsequent inbound migration flow into the UAE as well as general population growth through the attractiveness of Dubai and the many government initiatives and reforms being rolled out. Dubai is an international outlier, but the reasons for its strong performance are demonstrable and unlikely to evaporate in the very near term.

New development project launches and the off-plan market in general have done well to attract a broad spectrum of buyer interest, with a myriad of products coming to market targeted to the various investor and end-user profiles. While many of these launches have had strong uptake thus far the pace of new launches continues to increase, and the ongoing absorption rate is something that should be closely monitored with any slowdown seen as a potential early warning sign of oversupply which could trigger a market slowdown. With this in mind, whilst we remain positive on the health of the Dubai market moving into 2023 and predict that growth will continue, the lessons of the past market cycles will need to stay at the forefront of decision makers across developers, investors, and consumers. The current market boom can’t run indefinitely. The big gains are probably behind us for the foreseeable future and some months of price stability look in prospect with small gains and losses evening out as we get into 2023.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |