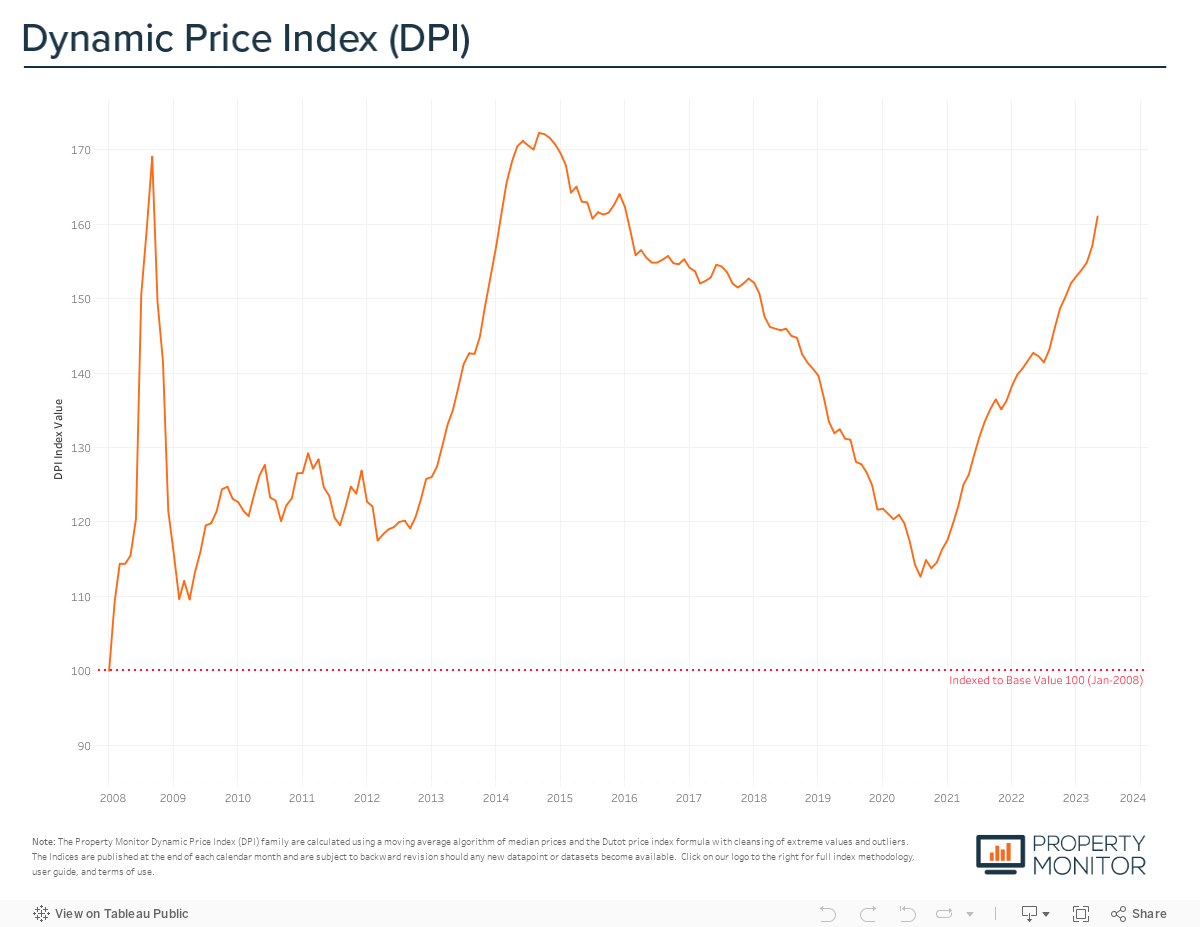

Here we go again. The pace of Dubai property price appreciation has skyrocketed to its highest rate in over 2 years increasing by 2.51% in May turbo-charged by off plan. This unexpectedly big monthly rise matches the red-hot pace of April 2021 which was the highest recorded in the current market upcycle – and previously last witnessed in March 2014 just before the market entered a six-year downcycle. This ‘May Mayhem’ gives pause for thought, as Dubai property values currently stand at AED 1,153 per sq ft measured by the independent Property Monitor Dynamic Price Index (DPI), and now sit just a shade over AED 80 per sq ft beneath the September 2014 peak of the last market cycle.

Over the last two quarters of 2022 and the first quarter of 2023 we saw monthly price growth significantly moderate and saw signs of a market that was moving towards healthy and sustainable expansion. However, as we have entered Q2 2023, price growth has rapidly gained momentum increasing by just under 4% in two months. The immediate question that enters the mind is “should this be real cause for concern?”

There is no simple definitive answer. In the unique Dubai market, investors and buyers have learned to ‘expect the unexpected’, and to get some context it’s important to understand what’s been the catalyst behind this recent skyrocket. When we dig into the data, we quickly uncover that the resurgence of off-plan project launches has significantly contributed to the substantial increase in transaction activity and subsequent positive price reaction across several areas of Dubai. This is particularly prevalent with new development projects in tier 2 communities, seeing average price per square foot values recording marked highs in contrast to the existing residential supply in the community. For example, Arjan which has had multiple successful project launches by developers such as ORO24 and Samana, have achieved an average of AED 1,267 per sq ft in 2023 whereas existing ready projects are trading at an average of AED 851 per sq ft. Given the record high number of new developments launched in recent months, and an outlook of several more upcoming throughout the year, we may see the pace of price appreciation continue to trend high and be driven by the off-plan segment. At the same time, price growth in the ready property market can be expected to be relatively muted in comparison particularly in the villa and townhouse segment where a general plateau in price has already been observed following their rapid rise at the onset of the market recovery.

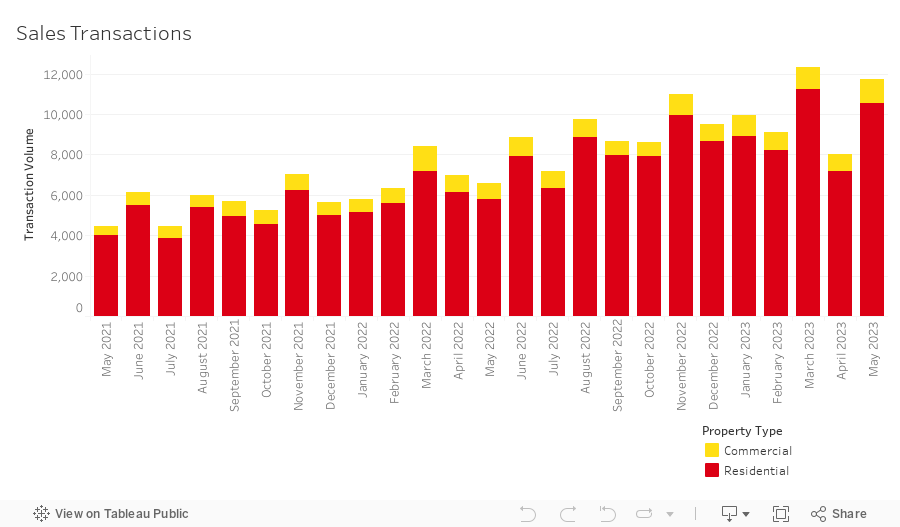

The total volume of sales transactions rocketed in May, increasing by a momentous 46.1% month-on-month to 11,749 sales. This comes just two months after the market recorded its fourth-highest monthly sales volume ever with just over 12,300 sales, yet directly follows a month where volume dropped to ~8,000 sales. This volatility correlates with shortened working hours and vacation periods in April owing to the holy month of Ramadan, when averaged out over the 3-month period volumes fall much closer inline with over trend of the market. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority at 89.5% (10,5202 sales transactions). The

highest transacted commercial property types were hotel apartments (4.5%), office spaces (2.8%), and land sales (1.8%).

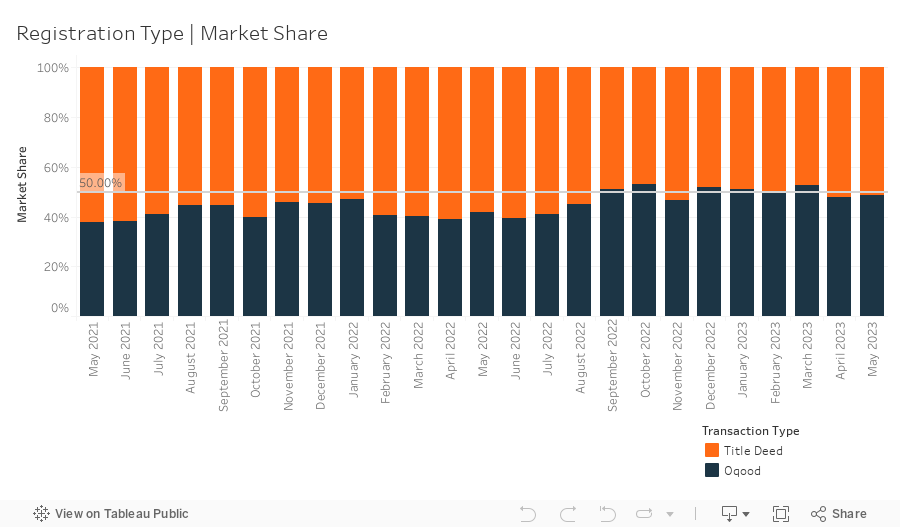

In May, a total of 5,698 off-plan Oqood transactions were registered, marking a 47.5% month-on-month increase in volume with Oqood transactions slightly increasing market share now representing 48.5% of the market. Meanwhile, Title Deed sale volumes also witnessed an increase rising by 44.8% and now account for 51.5% of all sales transactions. Although the market may appear to be slightly tilted in favour of completed properties over off-plan, a correctional adjustment by the Property Monitor team for registration technicalities within the Dubai Land Department (DLD), reveals that several villa and townhouse sales, presented as completed with issued Title Deeds, are indeed under construction and sold off-plan. In reality, off-plan transactions have held a dominant market share since Q4 2021, currently standing at 54.8%.

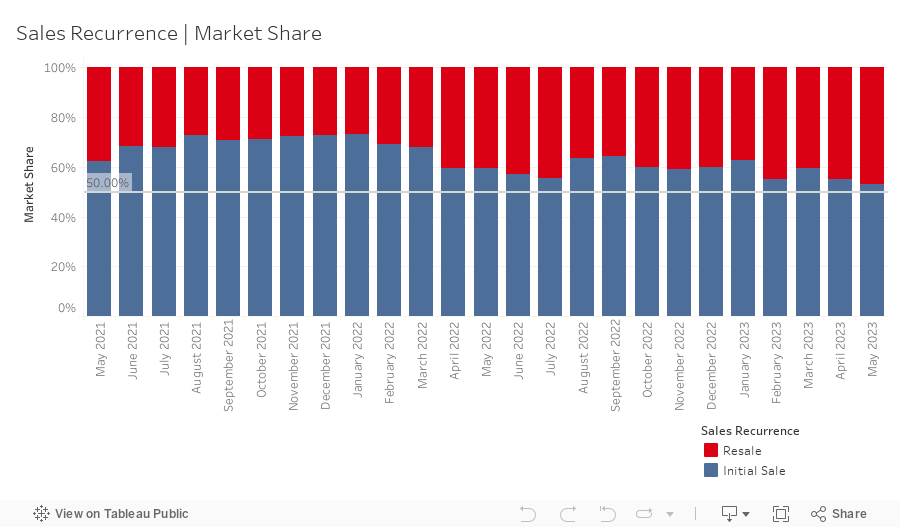

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 5,496 in May representing a market share of 46.8%, increasing by a further 2.1% month-on-month following a 3.9% increase in April. With this increase in overall resale activity, the portion of off-plan resales also continued to decrease—down 0.3% in April—falling to 21.1% after reaching a high of 28.3% in February this year. Whilst off-plan resale activity has itself recently shown a slowdown, when we look at the 12-month moving average such activity has now reached an all-time high of 20%. We continue to stress that closely monitoring this activity remains important as off-plan resales can be an indicator of increasing speculative activity, particularly if it’s in the early days of construction, well before handover. For now, whilst the current level of activity is skewed towards properties that are within a year of anticipated completion this helps to support a view that there is no immediate cause for alarm. But seasoned investors will be watching carefully as the next few months data unfolds.

Mortgage transaction volumes increased by 18.9% in May with a total of 2,881 loans recorded. Loans for refinancing and equity release were a significant driver of this growth, increasing their market share by 9.6% to 40.3% and now account for the majority of the transaction activity. Meanwhile, bulk mortgages—those taken by developers and larger investors with multiple units—fell sharply by 19.2% to 20.1% in May losing their majority share of the market. The 579 loan transactions were spread across several projects, most notably portfolio mortgage modifications at Orchard Residence (156) in Dubai Science Park, portfolio mortgage registrations at Da Vinci Tower (96) in Business Bay, and mortgage transfers at Marina Sail (49) in Dubai Marina. The remaining 39.6% (up 9.6% from last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.72m at a loan-to-value ratio of 76.9%.

Average gross rental yields for residential properties in the Emirate continued to remain stable as a whole in May, increasing by just 0.02% to 6.72%. Yields for apartments and townhouses saw modest declines of 0.02% and 0.07% respectively, dropping to 7.15% and 6.27%. However, villa yields rebounded after hitting their lowest level in nine months in April, increasing by 0.23% to 4.81%.

Forward looking into the summer months of the year we anticipate that given supply already in the pipeline and the international picture, the diverging tale of two markets will continue, with off-plan maintaining its dominance for the foreseeable future, while the ready property market will largely continue to plateau across the majority of property types and prices points, save for the exception of the ultra-high-end which has become a micro market of its own. Investment into the Dubai property market from aboard should see a further boost from the Far East with purchases by Chinese investors slowing gathering momentum yet remaining short of the top spot which they held prior to the COVID-19 pandemic. As the weather heats up so will the market.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |