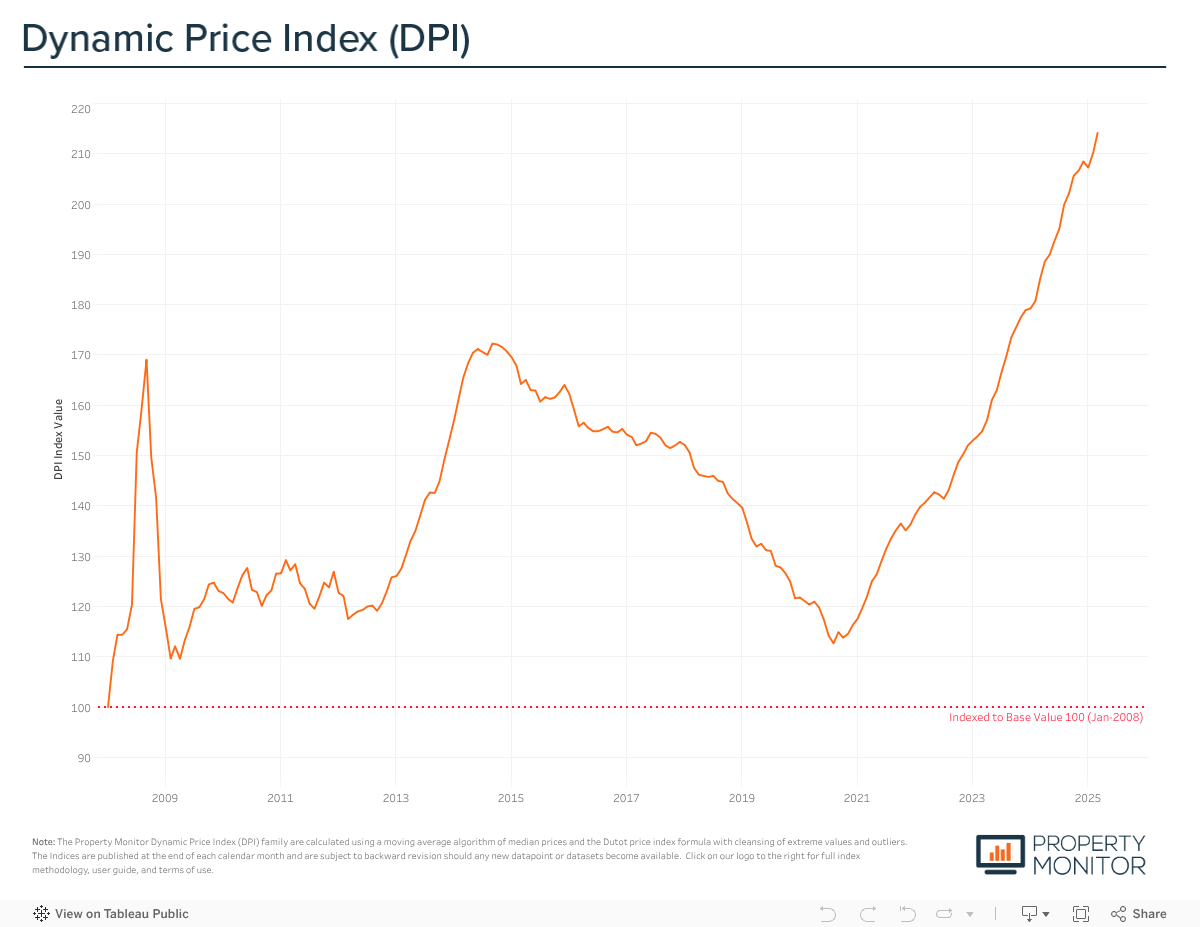

Following last month’s price growth resurgence, Dubai’s property prices experienced another higher-than-average month of average price growth, recording a gain of 1.88% in March. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently average AED 1,534 per square foot, standing 24.3% above the previous market peak in September 2014.

Delving further into the underlying data reveals that the recent uptick in price appreciation continues to be primarily driven by significant differences in trading prices between existing homes and off-plan new development projects. Among the 42 communities tracked by the index, 14 exhibited off-plan price premiums exceeding 30%, reaching levels as high as 85% and 73% respectively in Motor City and Dubai Sports City, where new apartment project launches differ drastically in quality and overall offering from the some of the now aging existing projects.

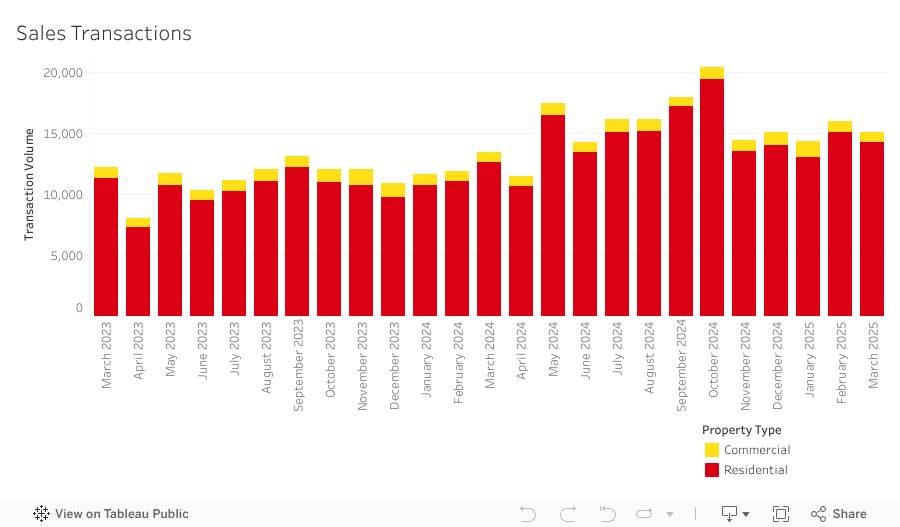

The total number of sale transactions declined by 5.7% month-on-month in March, reaching 15,223. However, despite this dip, it still stands as the highest transaction volume ever recorded for the month of March surpassing the record March in 2024 by almost 11%. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 93.7% (14,274 transactions). The highest transacted commercial property types were office spaces (2.1%), vacant land (1.5%), and hotel apartments (1.0%).

In March, 9,005 off-plan Oqood transactions were recorded, a minor decrease of 1.0% from the previous month, however an increase in market share to 59.2%. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with

Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions secure an even larger market share of 67.2%. Meanwhile, Title Deed sale volumes also witnessed a decrease, falling by 11.7% and now account for 40.8% of all sales transactions. This drop in volume, particularly in the Title Deed sales, is related to the reduced trading days at the end of the month due to the Eid break and is not indicative of any downside market factors.

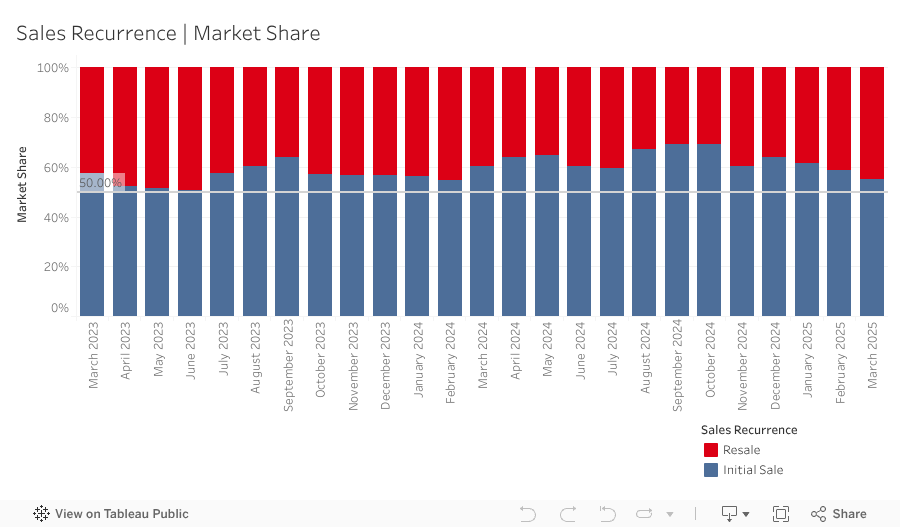

Meanwhile, resale transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 6,514 in March, accounting for 42.8% of the market. This marks a 1.4% increase month-on-month. While overall resale activity increased, so too did the portion of off-plan resales, rising to 29.3% and bringing the 12-month rolling average to 25.4%. Off-plan resale activity has continued its steady upward trajectory over the past three years. As in recent months, the majority of these resales remain concentrated in projects approaching completion within the next 12 months, indicating sustained demand from both end users and investors, rather than purely speculative behavior. That said, there are emerging signs of the market broadening, with resale transactions gradually extending to properties with handovers 15 to 16 months away. If this trend persists, it could point to a shift toward increased speculation—or alternatively, a sign of weakening investor confidence, with some choosing to exit earlier in the cycle to lock in gains and reduce exposure.

Mortgage transaction volumes decreased by 2.3% in March with a total of 3,434 loans recorded. During the month, loans taken for new purchase money mortgages accounted for 56.9% (up 6.3% from last month) of borrowing activity, with the average amount borrowed being AED 1.88m at a loan-to-value ratio of 75.6%. Meanwhile, loans for refinancing and equity release saw their market share increase by 1.3% to 36.3%. The remaining 6.8% (down by 7.6% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 232 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage

modifications at Orra Harbour (49) and Orra Marina (21) in Dubai Marina, and RP Heights (20) in Downtown.

Looking ahead, it’s important to contextualize where Dubai sits in the current market cycle. The recovery and expansion phase, now in its 53rd month, has delivered an average aggregate monthly price appreciation of 1.2%, with the peak monthly gain reaching 2.51%. By comparison, during the previous growth cycle from 2012 to 2014, monthly appreciation averaged a higher 1.6%, with individual months registering gains as high as 2.99%. While the current cycle has been more prolonged and resilient, the pace of growth has been comparatively measured—suggesting a market supported by a broader and more diverse base of demand.

High absorption rates for off-plan launches remain a key feature of the current landscape, buoyed by investor interest and a strong appetite for new supply. That said, absorption at this pace is unlikely to be sustained indefinitely. Developers and stakeholders should prepare for the likelihood of a gradual slowdown as the volume of launches begins to test demand thresholds.

Another factor to watch closely is the continued rise in off-plan resales, especially for units further from handover. While this could reflect speculative behavior, it may also signal growing concerns among investors about market saturation or timing. Early exits to lock in gains and reduce exposure could become more common, particularly if interest rates remain elevated or if global macroeconomic sentiment weakens.

To maintain a healthy trajectory, the market will benefit from a shift toward product diversity, realistic pricing, and strategic phasing of new inventory. Sustaining momentum in 2025 will depend not just on demand-side strength, but also on measured supply-side discipline.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |