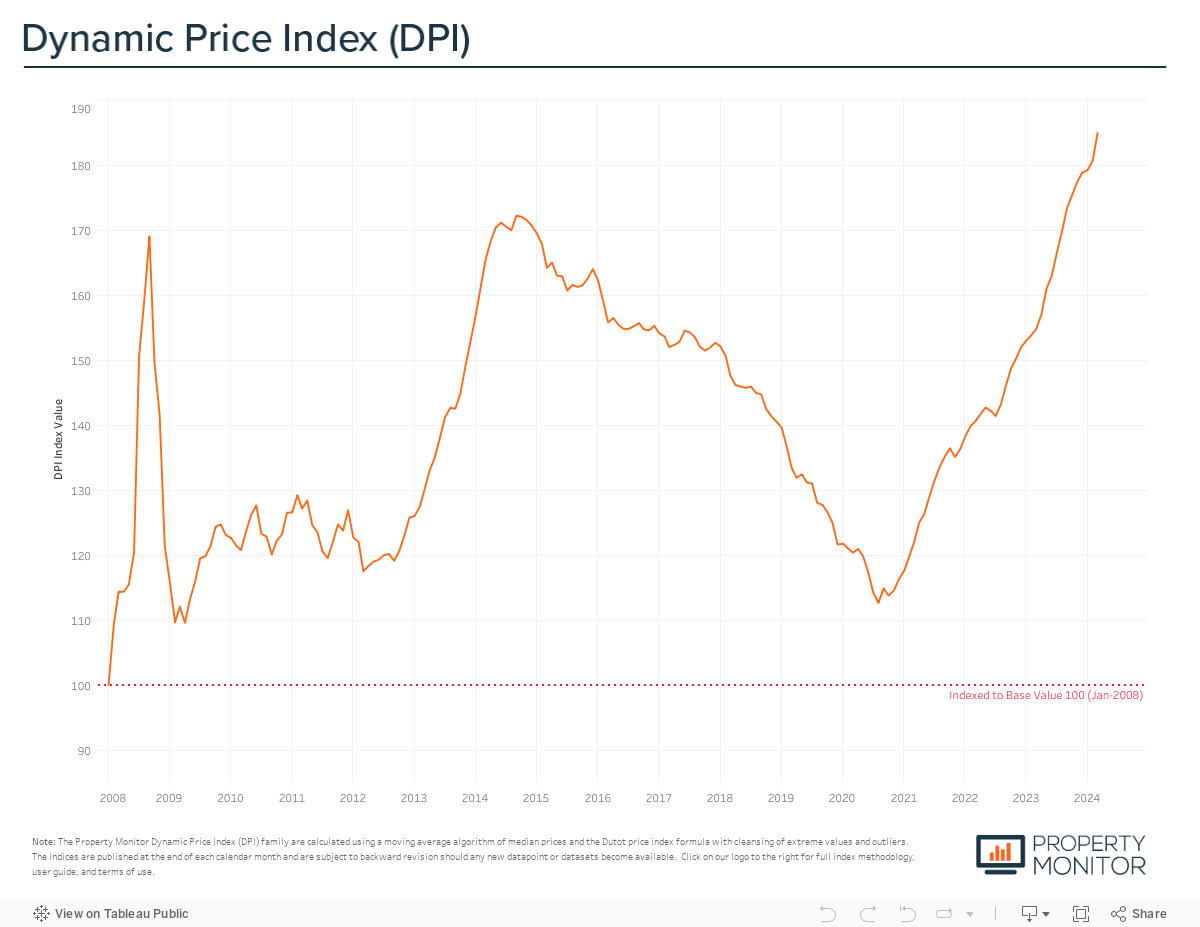

Following several months of modest price appreciation, Dubai’s property prices experienced a dramatic surge in March, recording a monthly gain of 2.37%—the largest month-on-month rise seen since May 2023. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently stand at AED 1,325 per square foot, 7.4% over the previous all-time high and market peak of September 2014.

This significant increase, and departure from the trend that began in late 2023, can largely be attributed to the considerable variations in trading prices between existing homes and new off-plan properties. Out of the 42 communities that the index is tracked against 15 saw price per square foot premiums for off-plan in excess of 20%, with premiums as high as 93% and 91% in Dubai Sports City and Liwan respectively, where new apartment project launches differ drastically in quality and overall offering from some of the now ageing existing projects. In addition to this quasi gentrification in the apartment segment, price growth was also buoyed up by the renovation effect in the single-family homes segment, particularly with villas. Several villas which were snapped up as the market began to recover have undergone total renovations and been transformed from their original design aesthetic to modern homes, with many rivalling the newly launched counterparts.

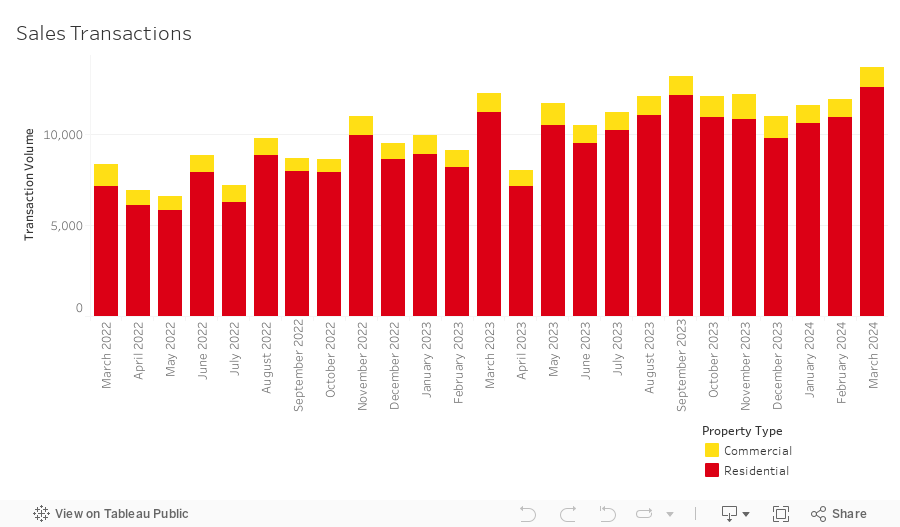

Sales transaction volumes continued their seemingly unstoppable ascent, surging by an impressive 14.7% in March to reach a total of 13,664 transactions. Not only does this set a new all-time record for the month of March but it also registered as the second highest monthly sales volume ever recorded. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 92% (12,565 transactions). The highest transacted commercial property types were hotel apartments (3.8%), office spaces (1.6%), and land sales (1.4%).

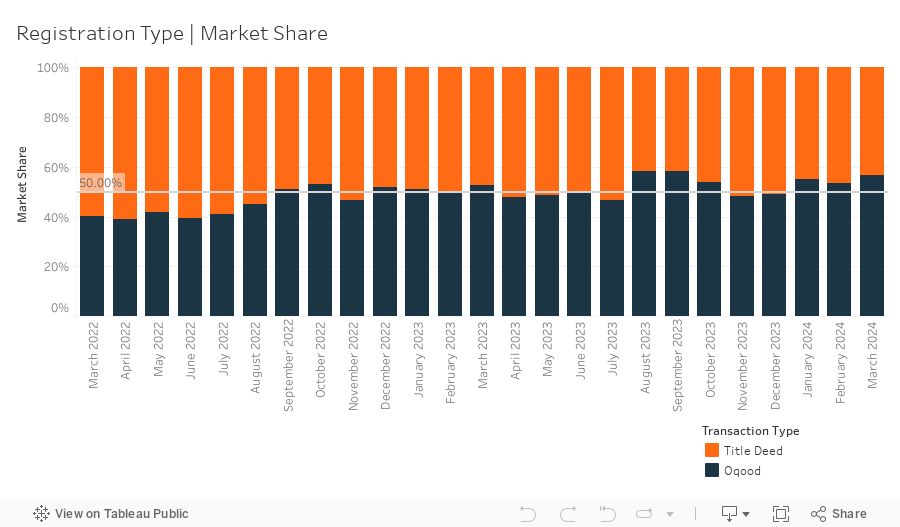

In March, an impressive 7,768 off-plan Oqood transactions were recorded, boasting a substantial 21.7% increase from the previous month and a 3.3% uptick in market share to 56.9%. These figures represent levels of activity not witnessed since 2009, highlighting the magnitude of resurgence in the off-plan market. Meanwhile, Title Deed sale volumes also witnessed an increase, rising by 6.6% and now account for 43.1% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, offplan transactions secure an even larger market share of 63.7%, further demonstrating the incredible dominance of new project sales.

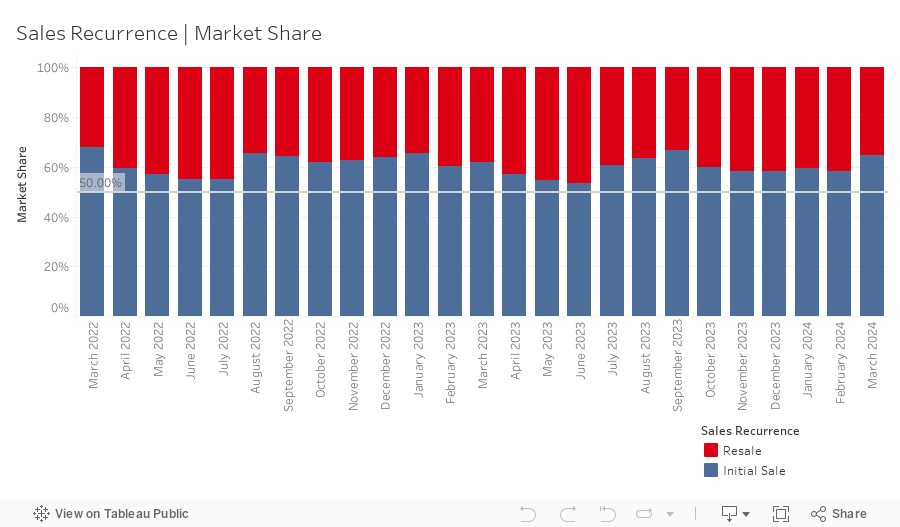

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 4,818 in March representing a market share of 35.3%, decreasing by 6.5% month-on-month, and propelling initial developer sales market share to 64.7%.

Preliminary numbers for new off-plan project launches in March show close to 30 projects and 10,000 units being added to the market for sale throughout the month. These projects now bring the total number of launches in Q1 2024 to an unprecedented ~34,000 units spread over 120 projects—an average of a new launch every 18 hours. This phenomenal level of activity in the off-plan market shows no signs of abating anytime soon, and will likely continue for the foreseeable future, with the pipeline of projects in the planning phase being tracked by the Property Monitor team well exceeding 100 additional projects across existing master communities. With the three new master communities which we reported last month as well as a fourth, Ghaf Woods by Majid Al Futtaim, soon to launch, the options for hungry investors and forward-looking end-users to choose from will grow even further. This plentiful buffet of projects and the choice that comes with it may present an increasing challenge for developers, as competition will be fierce, buyer expectations high, and greater scrutiny given in selecting the best investment. Well-established and larger developers will be best positioned to capitalise on the mass-market across the majority of price points, while niche developers that focus on the luxury and ultra-luxury segments will also be in positions of strength, with fewer projects launched and a laser focus on their target markets. The newer entrants to the market who are going head-to-head with the aforementioned group of developers may struggle to stand out, and may need to revert to offering traditional commercial terms skewed towards buyers, such as giveaways, post-handover payment plans, and developer paid DLD transfer fees.

Mortgage transaction volumes decreased by 2.6% in March with a total of 2,793 loans recorded. Loans taken for new purchase money mortgages accounted for 53.3% (up an additional 7.2% from last month) of borrowing activity, with the average amount borrowed being AED 1.68m at a loan-to-value ratio of 76.6%. Meanwhile, loans for refinancing and equity release saw their market share decrease by 1.2% to 36.4%. The remaining 10.3% (down by 6% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 288 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at FIVE Luxe (121) in Jumeirah Beach Residence as well as portfolio mortgage pre-registrations at Shakespeare Tower (82), Rapunzel Tower (38), and Queen Sheba Tower (19) in Legends. As predicted, the US Federal Reserve FOMC kept the target rate range unchanged at 5.25-5.50% for a 5th consecutive meeting, leading to the equivalent local UAE intrabank rates also holding steady. Although these rates have remained the same since July 2023, some mortgage offerings from lenders have seen a drop, with 3-year and 5-year fixedrate products falling by as much as 50 basis points. This reduction has likely enhanced purchasing power and affordability for numerous borrowers and is one of the reasons we continue to witness high mortgage volumes led by new purchase activity.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |