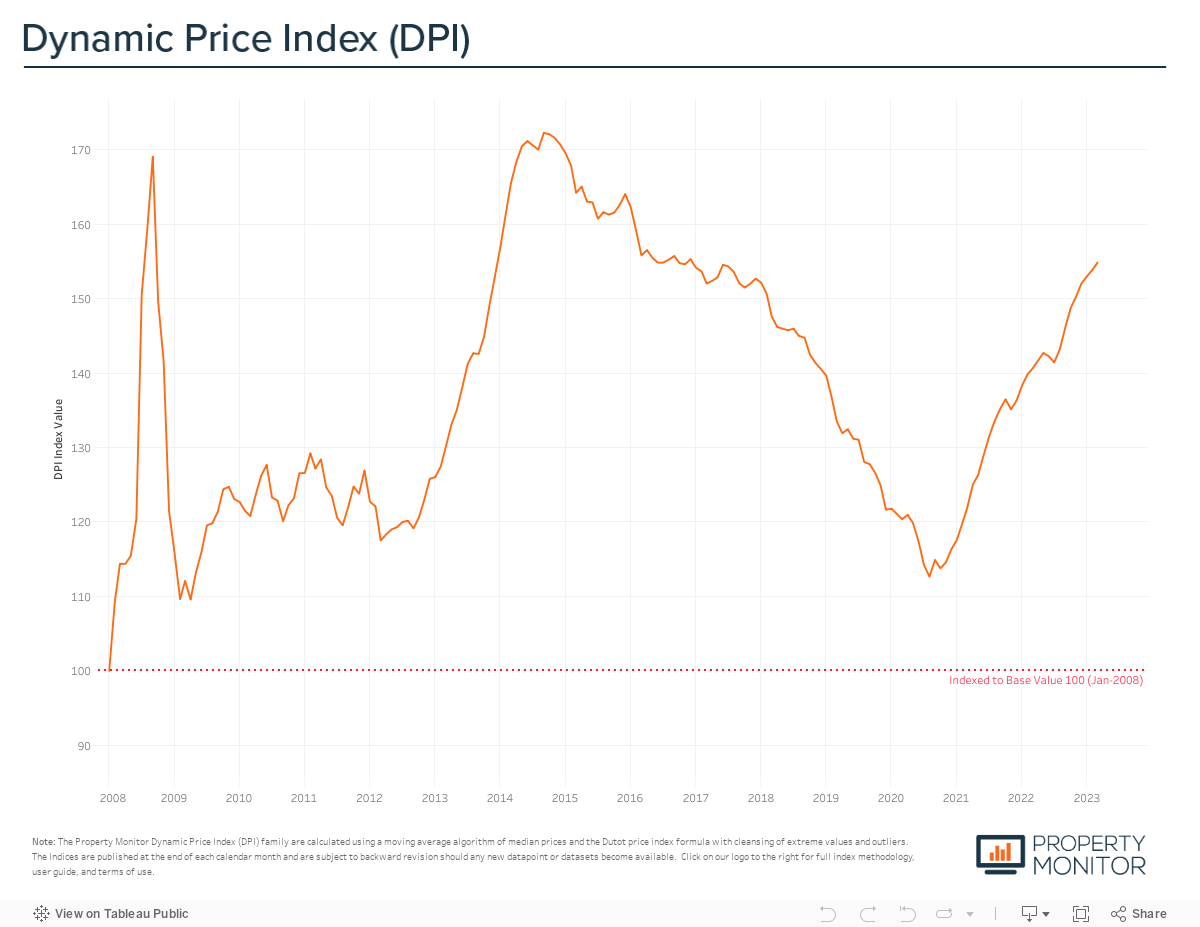

In March, the Dubai real estate market witnessed a continuation of the last 2 years’ upward trend in residential property prices, with values increasing 0.62% on a monthly basis. This marks the third consecutive month where price growth has remained steady at around 60 basis points, indicating a healthy and measured market expansion. In contrast, the early stages of the current growth cycle saw monthly price appreciation averaging 1.33% and 0.92% in 2021 and 2022 respectively. This growth pattern is exactly as predicted by Property Monitor last year and we expect relative price stability to be the emerging trend, with small upward and downward month-on-month changes during the remainder of 2023.

Dubai property values currently stand at AED 1,109 per sq ft according to the Property Monitor Dynamic Price Index (DPI). These values were last seen in July 2018 when the market was falling and were touched again during a previous upward cycle in January 2014.

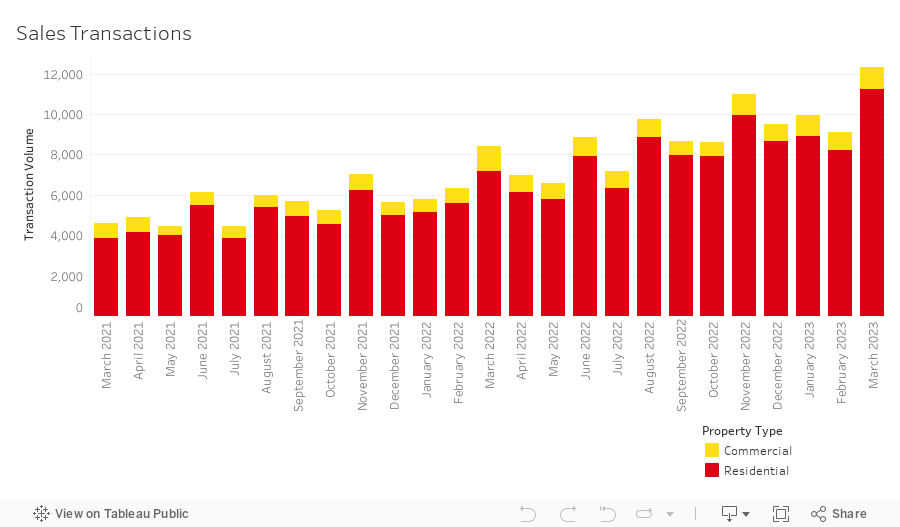

The total volume of sales transactions soared in March, increasing by a remarkable 34.8% month-on-month to 12,304 sales. This represents the strongest March on record and the fourth-highest monthly sales figure ever recorded. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority at 91.5% (11,253 sales transactions), with apartment sales alone experiencing a nearly 50% month-on-month increase and contributing significantly to the overall surge in transaction activity. The highest transacted commercial property types were hotel apartments (3.7%), office spaces (2.2%), and land sales (1.6%).

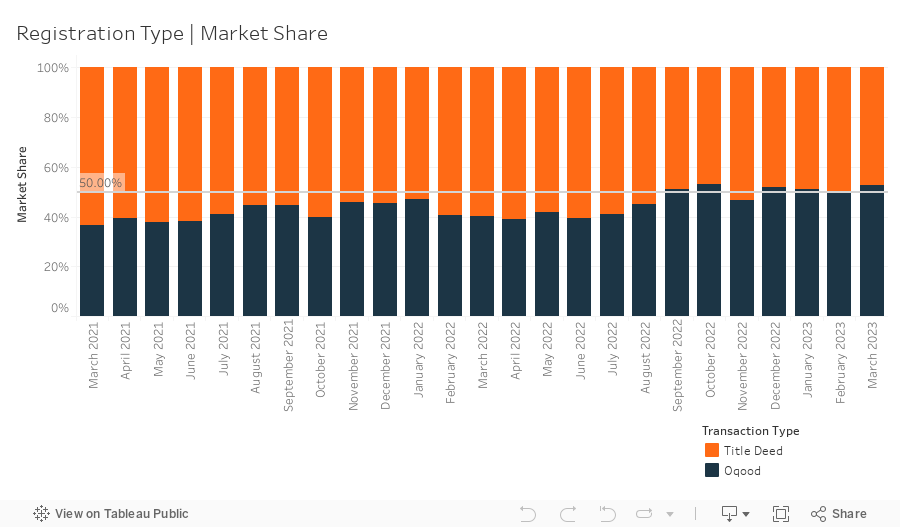

In March, a record-breaking total of 6,509 off-plan Oqood transactions were registered, marking a 43% month-on-month increase and representing the highest monthly figure in 13 years. Oqood transactions now account for the majority of the market at 52.9%, with Title Deed sale volumes falling to 47.1%. Although the market may appear to be only slightly tilted in favour of off-plan sales over completed properties, a correctional adjustment by the Property Monitor team for registration technicalities within the Dubai Land Department (DLD), reveals that several villa and townhouse sales, presented as completed with issued Title Deeds, are actually under construction and sold off-plan. In reality, off-plan transactions hold a more dominant market share of 59.2%.

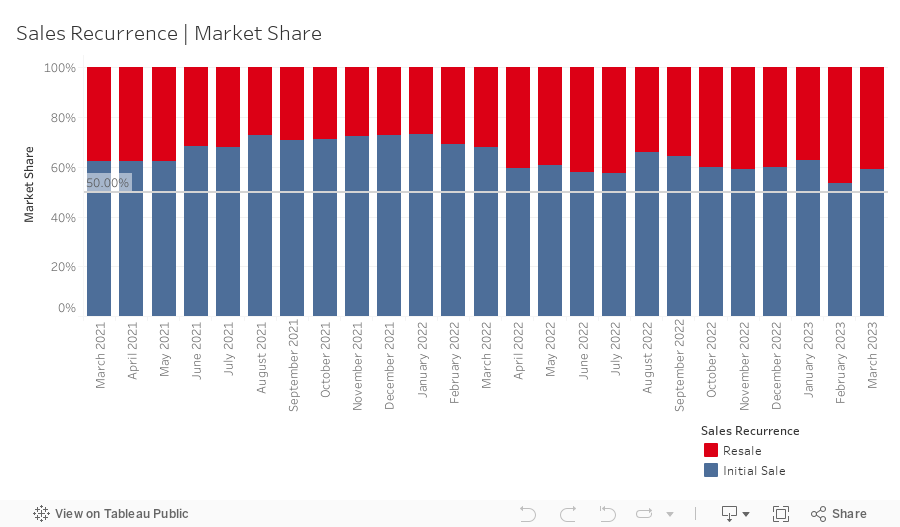

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 6,011 in March representing a market share of 40.7%, decreasing 5.6% month-on-month. With this decrease in overall resale activity, the portion of off-plan resales also decreased—down 6% in March—falling to 22.2% after reaching a notable high of 28.3% last month. Monitoring off-plan resale activity is crucial during this market growth phase as it serves as an indicator of speculative activity that can drive prices up at an unsustainable pace.

An analysis of the monthly data trend suggests a slowdown in off-plan resales, however it’s important to consider that this is based on a percentage of overall activity for the month—in a month where sales volumes grew considerably. If we look at the simple volume of off-plan resale transactions, the number of off-plan resales still remains at a comparable level to the previous month, with 1,114 resales recorded in March compared to 1,196 in February. At this stage we believe there is no cause for alarm. The current activity is mostly focused on properties expected to be finished within a year, with the premiums sellers receiving on these sales being in line with overall market appreciation and the pricing of comparable ready properties. However, if activity shifts toward properties that are further away from handover, caution should be exercised, as it is likely driven by speculators seeking a quick flip at prices that may not be in line with market values prevailing at handover, if our expectation that a moderating and sustainable market lies ahead is correct

The volume of mortgage transactions hit an all-time record high in March with a total of 4,261 loans recorded, which at face value completely defies any market expectations given the high interest rate environment and general downward pressure on all forms of borrowing and debt. However, a more detailed look at mortgage transactions reveals that the highest growth segment was for bulk mortgages—those taken by developers and larger investors with multiple units—increasing their market share by a considerable 16.6% month-on-month to 55%. The 2,345 loan transactions were spread across several projects, most notably portfolio mortgage registrations for villas in Al Furjan (412), apartments at Lucky Residence 1 (148) in JVC, and the retail and office units across Golden Mile in Palm Jumeriah (163), as well as over 1,000 transactions for units included in portfolio mortgage modifications. These bulk mortgage transactions are more commercial in nature and not a representation of the general mortgage market and typical day-to-day home financing.

Meanwhile, refinancing and equity release also decreased their market share, shrinking by 13.6% to 22.1%. The remaining 22.9% (down 3% from last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.79m at a loan-to-value ratio of 76.6%.

The average gross rental yields for residential properties in the Emirate remained steady in March, with a slight increase of only 0.05% to 6.69% compared to the previous month. Yields for apartments and townhouses saw modest increases, with rises of 0.09% and 0.07% respectively, reaching 7.11% and 6.38%. However, villa yields continued to decline and hit their lowest level in eight months, decreasing by 0.11% to 4.77%. The decline in villa yields can be attributed to multiple factors, including the ongoing bid-ask spread delta on sales prices, rental rates in many villa communities appearing to have reached their peak, and much needed new single-family rental supply entering the market and easing demand.

Looking forward, despite the recent surge and strength of sales transaction volumes, we still anticipate that the market will lose some steam and the record setting pace of sales volumes will dissipate with the diverging tale of two markets continuing. The dominance of off-plan will likely continue, if not grow further, with the rate and number of off-plan launches remaining in high gear throughout the year. To mitigate the risk of oversupply and the market being pushed from growth to decline, developers will need to closely monitor demand and absorption rates and be willing and able to adapt if needed. We do not see prices falling any time soon, but equally do not believe that overall Dubai prices will show significant further appreciation over the rest of the year, when taken as a whole. Steady as she goes…

The ready villa and townhouse market is already somewhat constrained with prices having reached their peak in several communities, and days-on-market beginning to increase unless sellers are priced close to recent sales. The trajectory of sales in these communities will be the ones most affected by the interest rate environment, and with potential further rate increases ahead and no reprieve likely until early-mid 2024, more buyers will be sidelined or move towards purchasing off-plan in a new launch, or a resale that is nearing completion and handover.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |