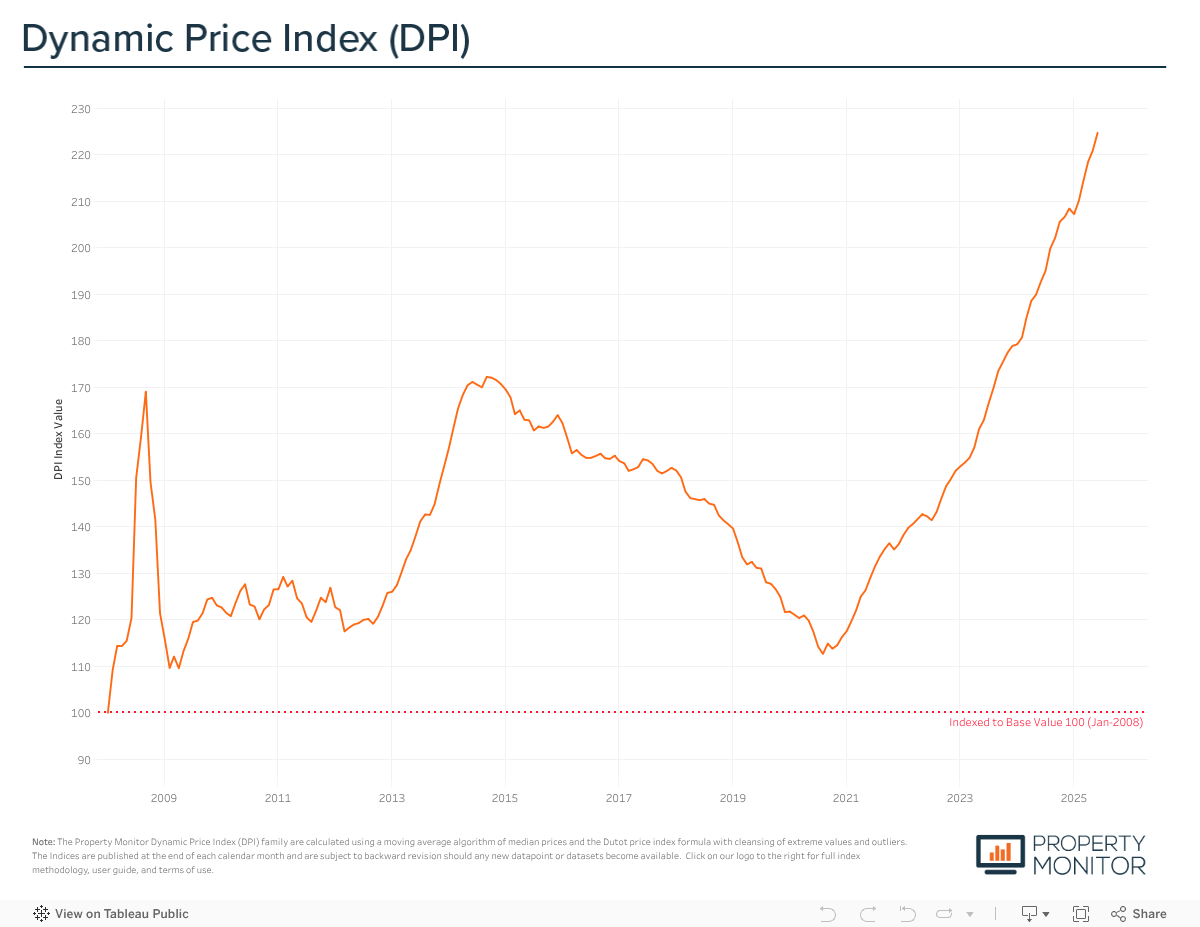

Maintaining its upward trajectory, Dubai’s real estate market registered another month of solid price appreciation recording a gain of 1.71% in June. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently average AED 1,609 per square foot, standing 30.5% above the previous market peak in September 2014.

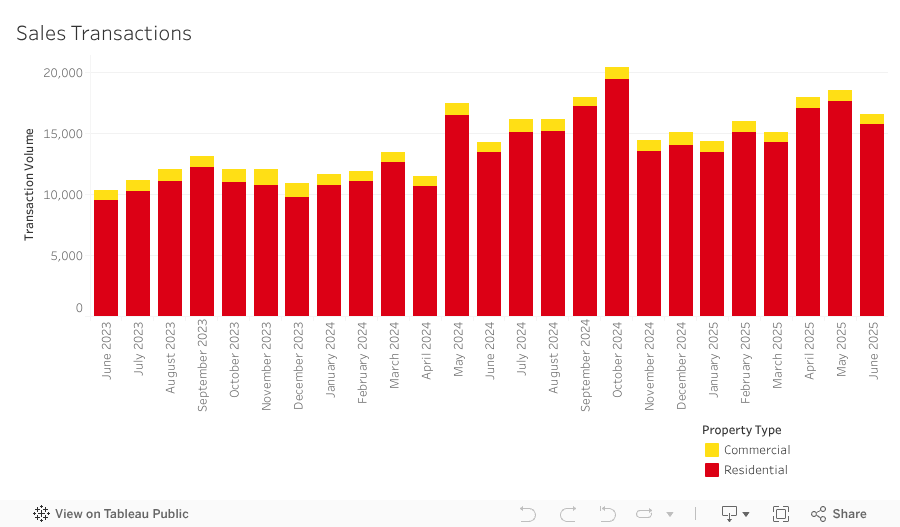

A total of 16,584 sale transactions were recorded in June, reflecting an 11.3% decrease from the previous month. This follows the recent two-month surge in April and May, during which transactions spiked to over 18,000 per month. While activity cooled from the extraordinary pace of the preceding months, June nonetheless outperformed historical norms—setting a new record for the month and surpassing last June’s previous high by 15.8%. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 94.2% (15,625 transactions). The highest transacted commercial property types were vacant land (2.0%), office spaces (1.6%), and hotel apartments (1.1%).

Year-to-date sales transaction volumes have surpassed just over 99,000 and are over 22.6% higher compared to the same period 2024. At the current pace of transaction velocity, we are on track to see year-end sales volumes reach ~198,000 and set a new all-time high.

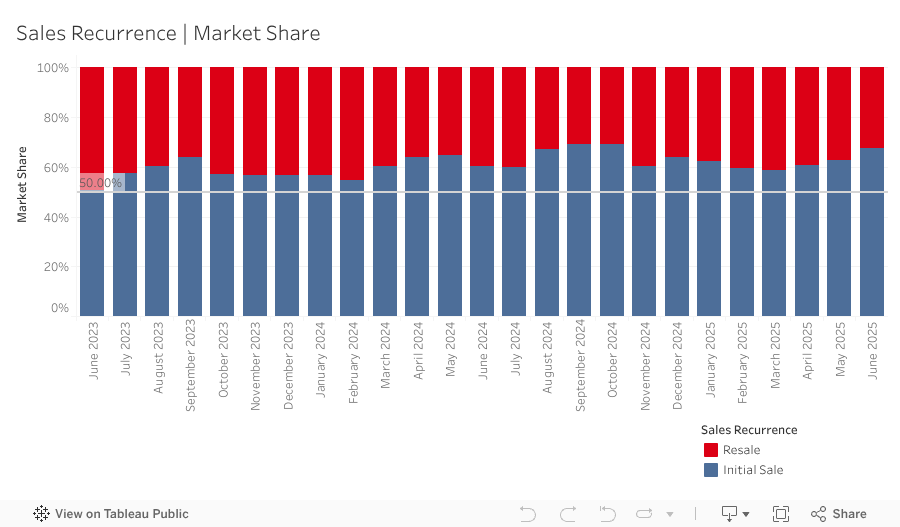

In June, 9,819 off-plan Oqood transactions were recorded, a decrease of 3.9% from the previous month, however, overall market share rose to 59.2%, up 4.6% month-on-month. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions represent an even larger market share of 69.6%. In contrast, Title Deed sale volumes witnessed a decrease, falling by 20.2% and now account for 40.8% of all sales transactions.

Meanwhile, resale transactions—any subsequent sale of a property following its initial sale by the developer—regardless of whether the first sale was off-plan or completed—stood at 5,288 in June, accounting for 31.9% of the market. This marks a 5.2% decrease month-on-month. In line with the decrease in overall resale activity, the portion of off-plan resales also moderated, falling to 22.1% and bringing the 12-month rolling average down to 26.0%.

June sustained the high volume of new project launch activity seen throughout the year, with more than 17,300 units introduced to the market in June, carrying an estimated combined gross sales value of approximately AED 33.7 billion. Apartments account for 90.7% of this new supply, while townhouses and villas represent 7.6% and 1.7%, respectively. Year-to-date, just over 79,000 units have been launched with a total sales value approaching AED 231 billion. Questions continue to mount about how—and for how long—the Dubai market can absorb this ongoing wave of massive new project launches. Early signs of softening absorption are beginning to emerge, with projects from developers that previously saw inventory snapped up within days now showing notable availability in the weeks following launch. This suggests that buyer urgency may be easing as supply continues to swell.

Mortgage transaction volumes decreased in June, falling by 4.15% with a total of 4,478 loans recorded, yet remain above the 12-month average of ~4,000. During the month, loans taken for new purchase money mortgages accounted for 43.3% (down 4.7% from last month) of borrowing activity, with average borrowings of AED 1.81M and a loan-to-value ratio of 73.5%. This marks the lowest LTV ratio recorded in over three years, dipping well below the typical 75–77% range seen consistently throughout that period. The decline may reflect the impact of recent Central Bank regulations prohibiting the financing of associated fees and costs within the loan amount—effectively increasing the upfront cash burden on buyers. Meanwhile, loans for refinancing and equity release saw their market share decrease by 1.4% to 30.8%. The remaining 25.9% (up by 6.1% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 1,158 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Armada Tower 1 (204) in Jumeirah Lakes Towers and Windsor Manor (103) in Business Bay, as well as portfolio mortgage registration pre-registrations at La Perla Blanca (190) in Jumeirah Village Circle, Uptown Mirdif Retail (160) in Mirdif, and Buildings 4A-4B (93) in Al Khail Heights.

As we move into the second half of the year, Dubai’s real estate market remains firmly in expansion, with both prices and transaction volumes on pace to set new records. However, beneath the headline numbers, subtle changes are beginning to emerge. The steady rise in new launches and signs of slowing absorption, particularly among developers that previously sold out within days, may indicate a gradual normalization in demand. Buyer urgency, while still elevated, appears to be easing. This makes pricing discipline and product differentiation increasingly important as competition for buyers intensifies.

The drop in average loan-to-value ratios to 73.5%, the lowest in more than three years, also reflects shifting market dynamics. New Central Bank regulations prohibiting the financing of transaction fees within mortgage structures are likely contributing to this decline, effectively raising the upfront cost of purchase and impacting buyer leverage. While mortgage activity remains relatively strong, a sustained reduction in borrowing capacity could start to weigh more heavily on transaction volumes, especially in segments driven by end-user affordability.

With more than 79,000 units launched so far this year and resale activity beginning to taper, developers may need to reassess their launch strategies to better align with actual market absorption. The pace of launches has become a defining feature of the current cycle, but its sustainability depends on how well supply is matched to real and timely demand.

The second half of 2025 will be defined by how effectively the market balances continued growth with greater selectivity from both investors and end-users. Continued growth is achievable, but it will require a shift toward greater discipline from developers and policymakers. Confidence will increasingly rest on realistic pricing, clear handover timelines, and genuine product value. If these elements come into sharper focus, the market can extend its current run into a more mature and sustainable phase of expansion.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |