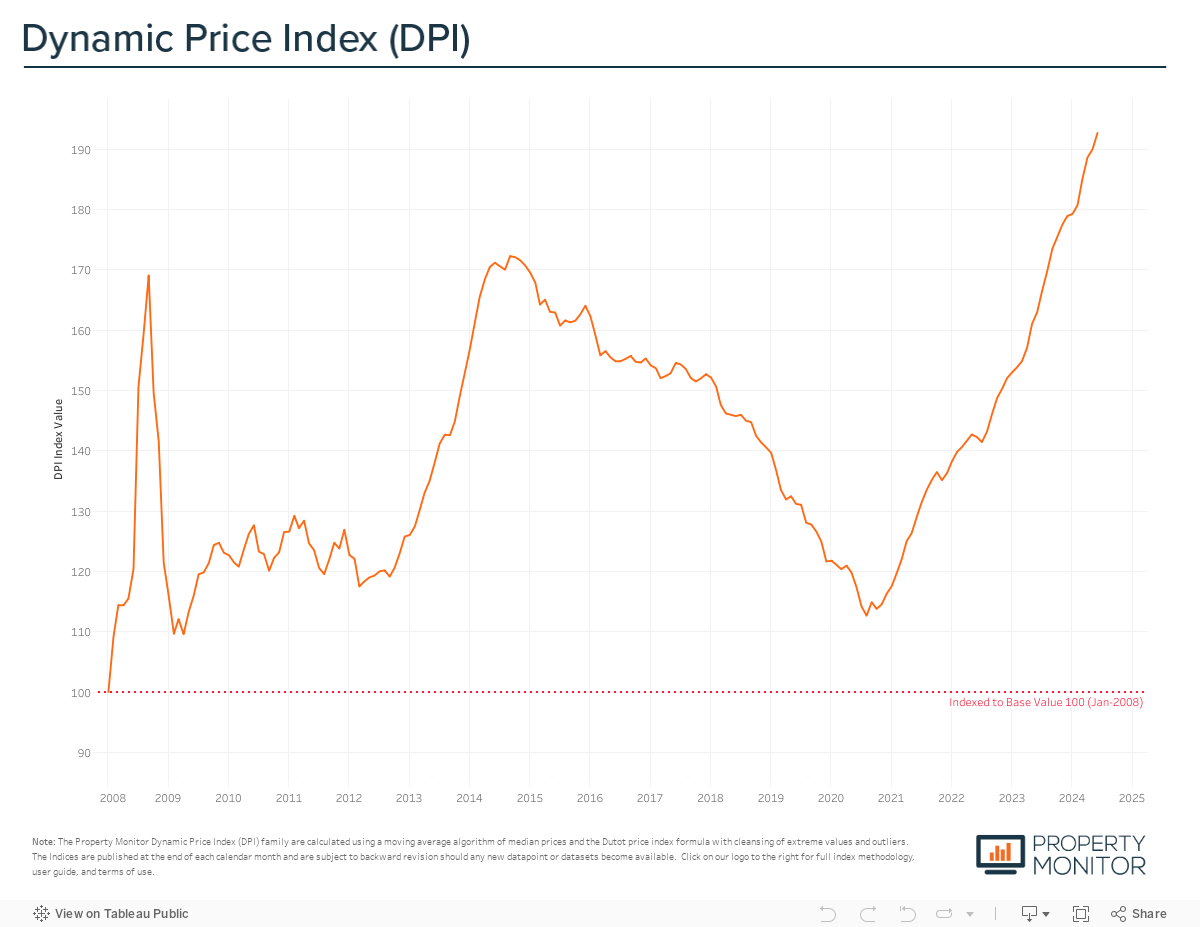

At the midway mark of the year, Dubai’s property price appreciation reached 7.5% with a gain of 1.46% recorded in June. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently stand at AED 1,380 per square foot, 11.9% over the previous all-time high and market peak of September 2014.

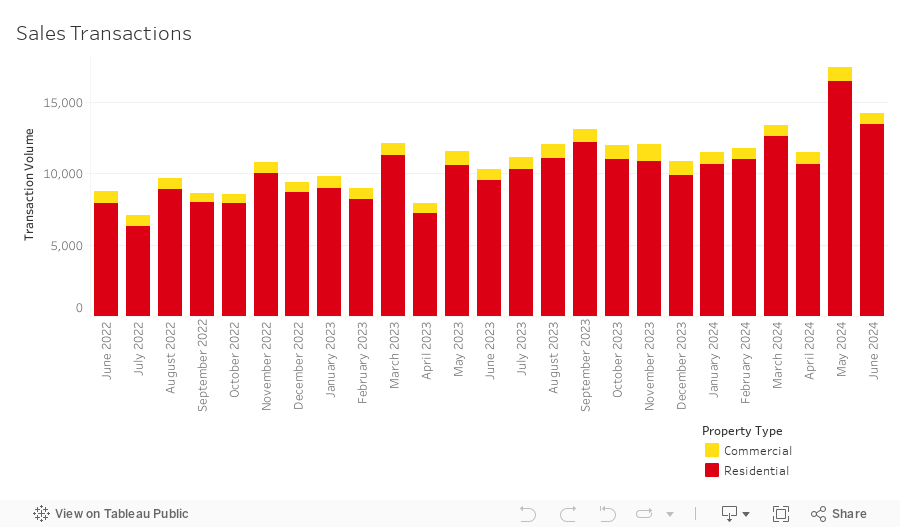

After an all-time record setting May, sales transaction volumes witnessed a significant drop of 19.3% in June, falling to a total of 14,285 transactions, yet still registered as the second highest level ever recorded. In June, residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 94.1% (14,435 transactions). The highest transacted commercial property types were vacant land (2.7%), office spaces (1.6%), and hotel apartments (1.6%). Year-to-date, overall sales transaction volumes have reached just shy of 81,000 and, given the current pace of sales, we are on track to eclipse last year’s record setting total of 133,673 sales by an additional 40,000 sales.

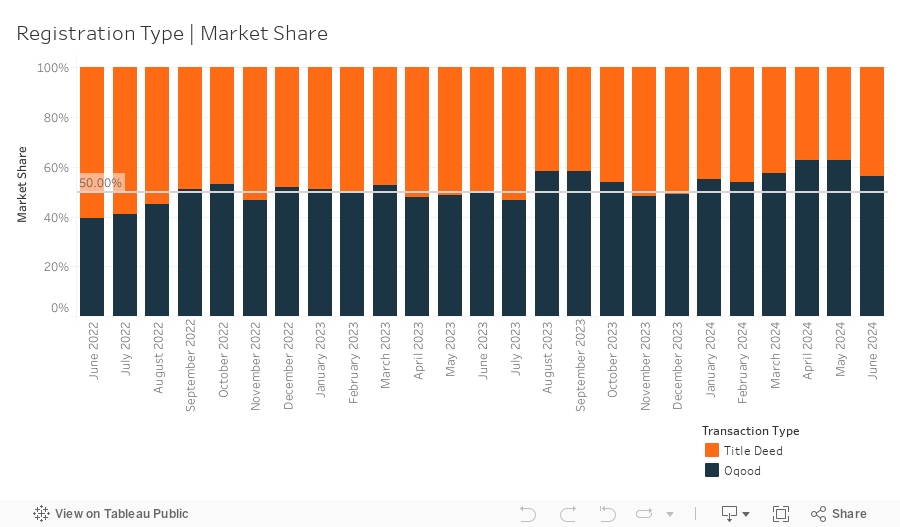

In June, 8,019 off-plan Oqood transactions were recorded, a decrease of 27.8% from the previous month and saw a slide in market share to 56.1%. Meanwhile, Title Deed sale volumes also witnessed a decrease, falling by 5.0% and now accounting for 43.69% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions secure an even larger market share of 68.0%.

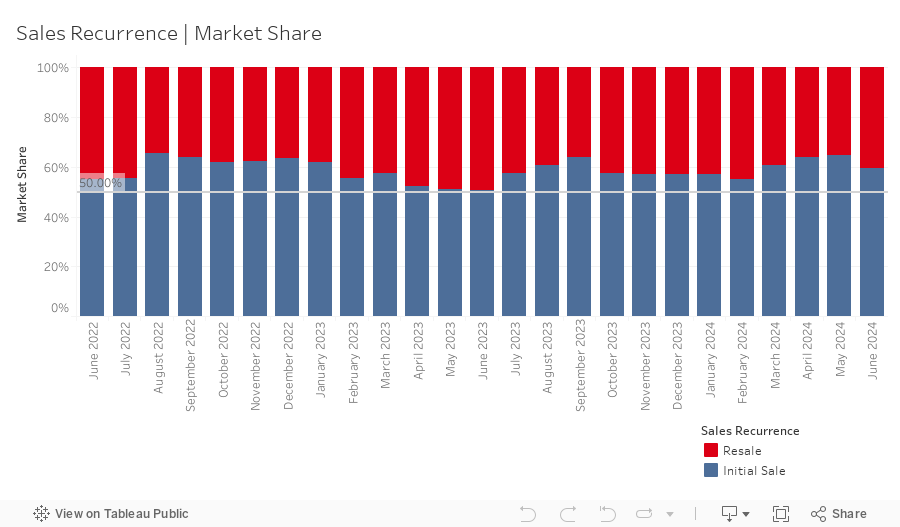

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 5,787 in June. This represents a market share of 40.5%, increasing by 5.2% month-on-month, driving initial developer sales market share down, likely temporarily, to just below 60%

New off-plan development project launches for June came in with just over 8,300 off-plan units added to the market for sale, with an anticipated combined gross sales value of ~AED 16.6 billion. Apartments represented 85.9% by volume of this new inventory, the remaining 14.1% was for single-family units—townhouses 13.5% and villas 0.6%. Year-todate, new project launches have exceeded just over 67,800 units and remain well on track to surpass last year’s ~96,000 units. Expect the fierce pace of project launches to continue with a summer slowdown unlikely, and gauging by recent land acquisition and project planning activities, keep an eye out for new opportunities across various pricing segments in a variety of communities, particularly: Meydan Horizon, Jumeriah Garden City, The Valley, and Motor City.

Mortgage transaction volumes decreased marginally by 0.15% in June with a total of 3,354 loans recorded–the third highest level trailing only March 2023 and May 2024. Loans taken for new purchase money mortgages accounted for 48.2% of borrowing activity (down 4.8% from last month), with the average amount borrowed being AED 1.8m at a loan-to-value ratio of 76.6%. Meanwhile, loans for refinancing and equity release saw their market share increase slightly by 0.5% to 29.5%. The remaining 23.3% (up by 4.3% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units.

The 748 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Barcelo Residences (232) in Dubai Marina, Binghatti Crystals (220) in Dubai Silicon Oasis, and Al Khail Heights 4A-4B (93). Despite the ongoing relatively high interest rate environment, borrowing activity remains strong and is not a deterrent for any of the mortgage market segments. We anticipate that mortgage volumes will remain consistent in the coming months, with a slight dip leading into Q4 in anticipation of a rate decrease on the horizon at either the November or December US FOMC meetings. Once there is an easing of interest rates, bulk loans and refinancing activity should see even greater volumes, with new records likely to be set.

As we edge closer to the end of Q2 and with the summer months ahead, we anticipate that the market will continue with high transactional activity and experience little to no negative impact of what has somewhat historically been a slower period. With Ramadan and the Eid breaks moving earlier in the year, the double punch of summer vacations and the holy period—which added to historic seasonality— will be mitigated. While we do not expect the market to slow overall, the divide between off-plan and completed property sales may widen further, in part due to the robust off-plan project pipeline, and in part due to unescapable seasonal net migration of Dubai residents escaping the summer heat.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |