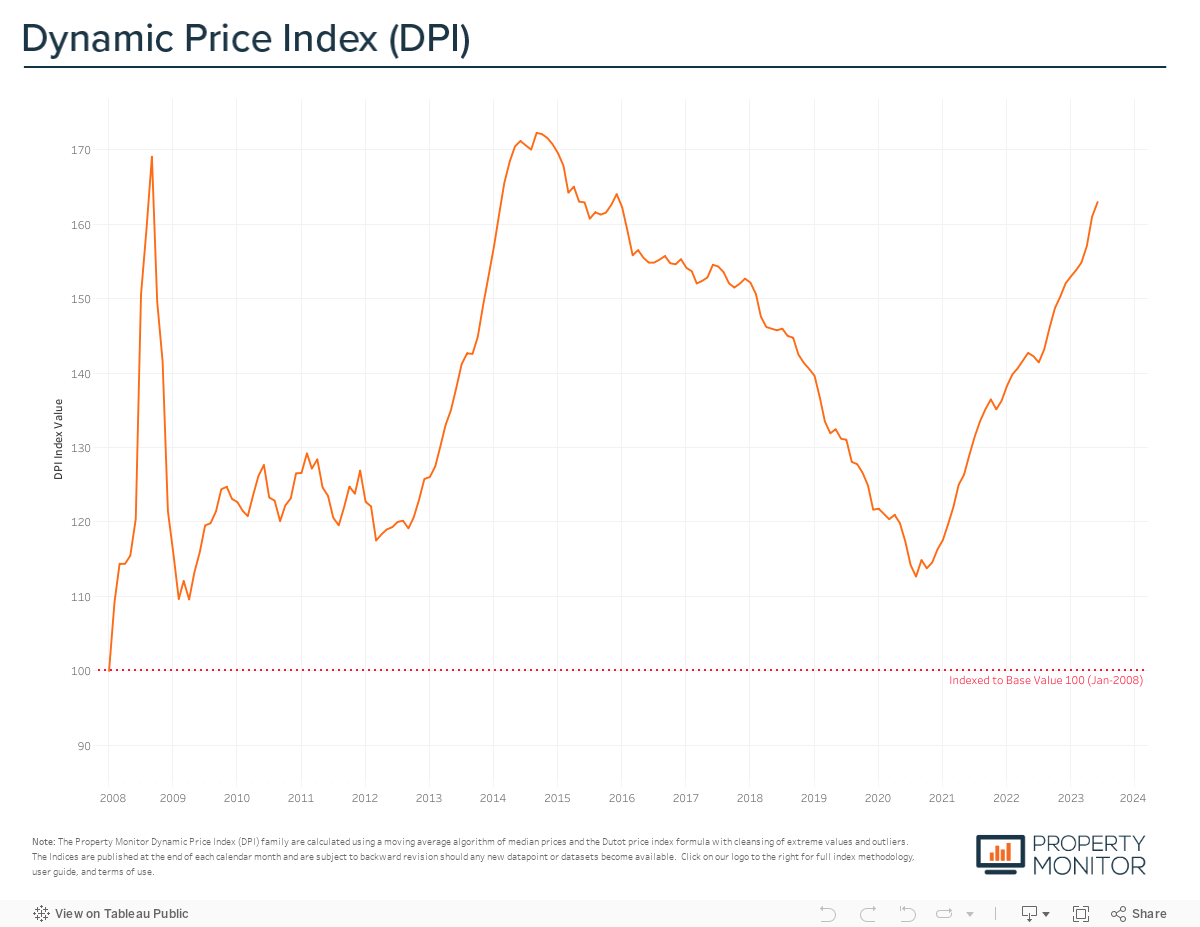

After skyrocketing to the highest rate of price growth seen in over 2 years last month, the rate of Dubai property price appreciation moderated and recorded an increase of 1.2% in June, less than half the increase recorded during May. Dubai property values currently stand at AED 1,167 per sq ft according to the Property Monitor Dynamic Price Index (DPI), and now sit just 5.4% below the September 2014 peak of the last market cycle.

The welcome month-on-month slowdown in the pace of price appreciation brings monthly growth back towards the more modest and sustainable rates witnessed earlier in the year. Over the coming months, Property Minitor predicts that we may well see ongoing market turbulence and price fluctuations, especially given that new project launches have not taken a pause for the summer and continue in full swing. It seems all but certain that property values in Dubai will reach, and most likely surpass, the previous 2014 market peak towards the tail end of this year.

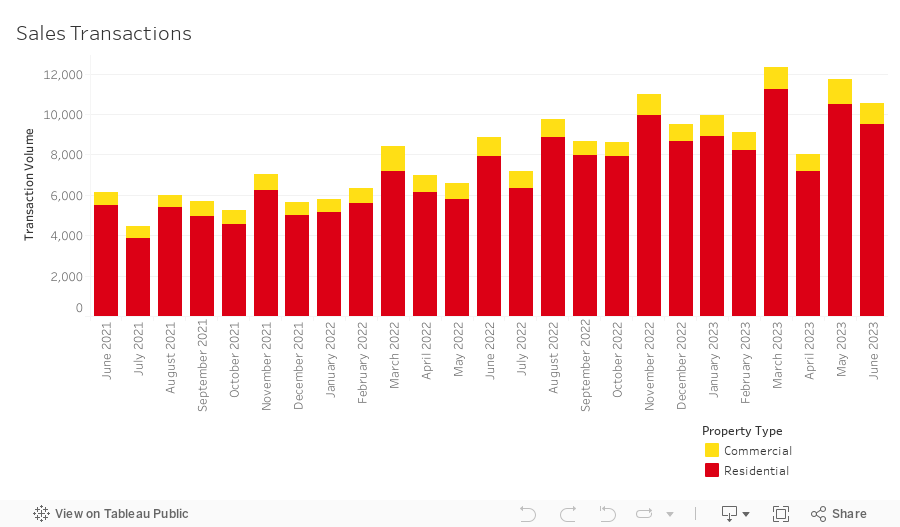

The total volume of sales transactions also moderated in June, decreasing by 10.4% month-on-month to 10,533 sales. This continues to mark the emerging trend of volatility in the volume of transactions occurring each month, with substantial swings in the range of ~1,000 to ~4,000 recorded sales having been a regular occurrence since February this year.

Average monthly transaction volumes in 2023 however, remain well above those ever previously recorded and currently have the market on track to eclipse the all-time annual sales record set way back in 2009. We currently predict close to 120,000 sales transactions this year.

Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 90.3% (9,507 sales transactions). The highest transacted commercial property types were hotel apartments (4.9%), land sales (1.9%), and office spaces (1.8%).

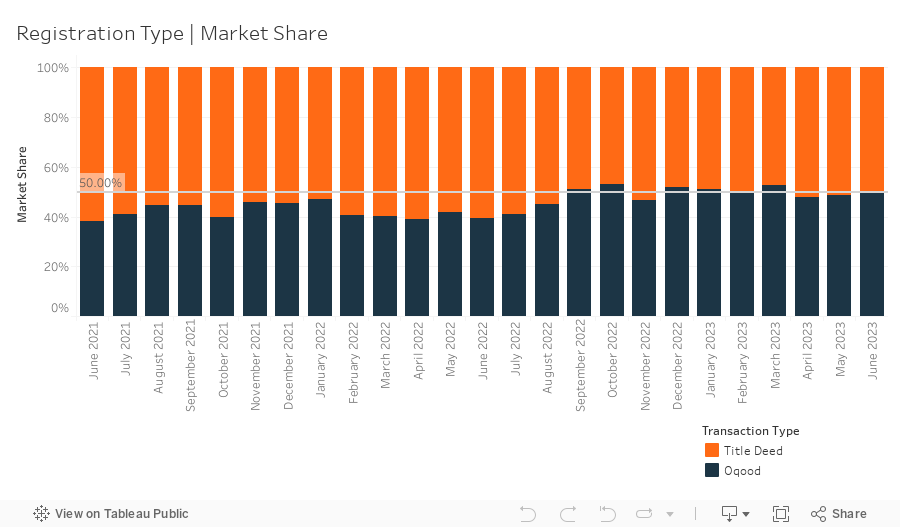

A total of 5,207 off-plan Oqood transactions were registered in June, decreasing by 8.6% month-on-month yet still increasing by a noteworthy 48.9% on a yearly basis. Oqood transactions now account for 49.4% of the market, while Title Deed sale volumes fell to 50.6%. Although the market may appear to be slightly tilted in favour of completed properties over off-plan, a correctional adjustment by the Property Monitor team for registration technicalities within the Dubai Land Department (DLD), reveals that several villa and townhouse sales presented as completed with issued Title Deeds are indeed under construction and sold off-plan. In reality, off-plan transactions have held a dominant market share since Q4 2021, currently standing at 55.6%.

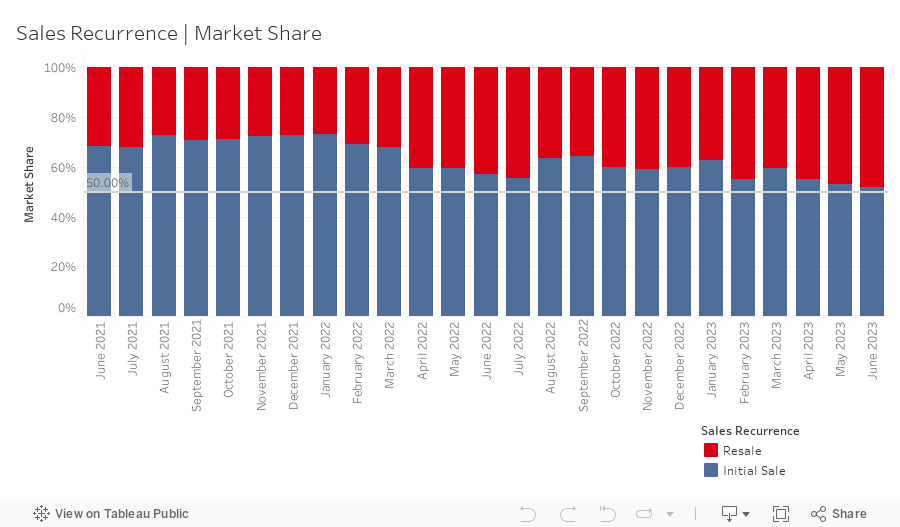

Meanwhile, resales transactions — any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 5,049 in June representing a market share of 47.9%, increasing by a further 1.2% month-on-month following increases of 2.1% and 3.9% recorded in the preceding months. With this increase in overall resale activity, the portion of off-plan resale also continued to increase — up 1.3% in June, rising overall to 22.4%. Speculative activity is slowly making up a greater portion of offplan resales, however most of these resales remain skewed towards properties that are within a year of anticipated completion.

With new project launches continuing to surge, and off-plan asking prices not increasing too aggressively, the scene is set for Dubai to provide an ample available pipeline of direct stock units from developers for the foreseeable future. This in turn means that it leaves little to be gained from buying a unit that’s being ‘flipped’ by a speculating investor soon after its initial purchase.

It will however continue to make sense for investors holding those properties that are closer to handover to consider reselling, with a potential buyer being willing to pay a premium in exchange for a property that can be occupied in the near future.

Mortgage transaction volumes decreased by 5.5% in June with a total of 2,724 loans recorded. Loans for refinancing and equity release were a significant attributor to this decline, seeing their market share drop by 6.7% to 33.6%. Meanwhile, bulk mortgages—those taken by developers and larger investors with multiple units—grew by 6.2% to 26.3% in June. The 717 bulk loan transactions were spread across several projects, most notably portfolio mortgage registrations at District One West (470), Orra Marina (33) in Dubai Marina, and City Walk Building 17 (31), as well as portfolio mortgage modifications at Shams 1 (64) in Jumeirah Beach Residence. The remaining 40.1% (up 0.5% from last month) of loans taken were new purchase money mortgages, with the average amount borrowed being AED 1.89m at a loan-to-value ratio of 75.9%.

Average gross rental yields for residential properties in the Emirate continued to remain stable in June, decreasing by just 0.05% to 6.67%. Yields for all three residential property types saw modest declines with apartments down 0.04% to 7.12%, townhouses down 0.13% to 6.14%, and villas down 0.02% to 4.79%. The decline in yields is looking very much as Property Monitor predicted in previous monthly commentary. As a result of many communities appearing to have reached their peak in achievable rental rates, coupled with sales prices plateauing in several communities – particularly those that saw the highest price appreciation in the early phases of the market recovery — some relief for renters is within sight. This most likely won’t be immediate in the form of significantly lower rents, but rather rental prices stabilising and showing a halt from the recent runaway increases over the coming quarter, with a further cooling off towards the end of the year.

With June recording month-on-month declines across the spectrum of measures analysed in this report it may at first appear that we are facing a seasonal summer slowdown. However, these same measures have all been setting records on a near monthly basis in recent times and it was inevitable that the trend would slow or revert at some point. Is the summer season the driving factor? Maybe, maybe not. What is more certain is that the Dubai real estate market is positioned to continue attracting investment from sources both locally and abroad. This is spurred on by the record number of new project launches with marketing campaigns that dominate the billboards and hoardings along Sheikh Zayed Road as well social media and digital channels. With several new master communities for villas and townhouses now making their way to launch, would be buyers who had decided to sit out from the completed market will have greater options in the off-plan segment and are likely to jump into the market and keep the demand faucet turned on for the remainder of this year. What happens in 2024 may be a different picture which we will return to as the third quarter numbers play out.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |