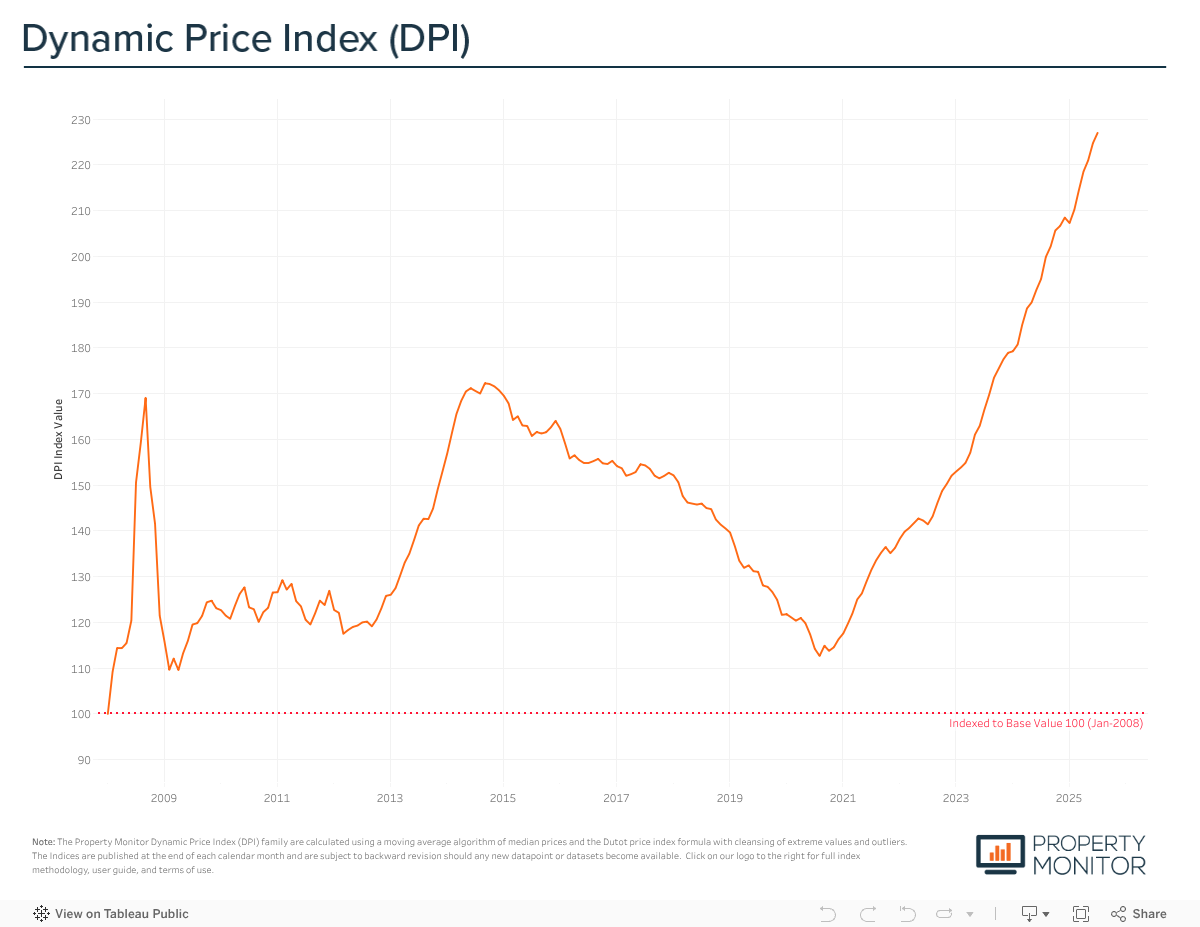

Dubai’s real estate market continued its upward momentum in July, posting a more measured price increase of 0.99% following June’s stronger gain of 1.71%. According to the Property Monitor Dynamic Price Index (DPI), average property prices now stand at AED 1,625 per square foot, standing 30.5% above the previous market peak in September 2014. A deeper look into the sub-categories of the index reveals that apartment price growth is softening while the trajectory of villas and townhouses is moving with greater momentum.

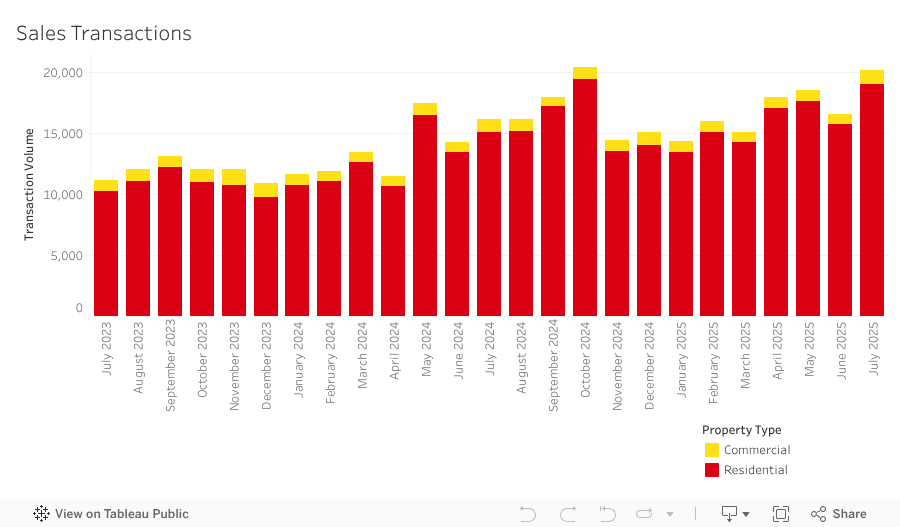

A total of 20,116 sale transactions were recorded in July, reflecting a 21.3% increase from the previous month. This marks yet another record-breaking month, continuing the 2025 trend of each month surpassing its previous all-time high. While the sharp month-on-month jump may appear dramatic at first glance, it is more likely a normalization following June’s dip, which was influenced by reduced working days and many extending time off around the Eid break. When viewed in the context of Q2’s overall volume trend, the combined figures for June and July suggest a smoothing effect rather than a sudden spike in market activity. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 93.7% (18,843 transactions). The highest transacted commercial property types were office spaces (2.2%), vacant land (1.3%), then hotel apartments and retail spaces (both 0.9%).

Year-to-date sales transaction volumes have surpassed just over 119,000 and are over 23.0% higher compared to the same period 2024. At the current pace of transaction velocity, we are on track to see year-end sales volumes surpass 200,000 and set a new all-time high.

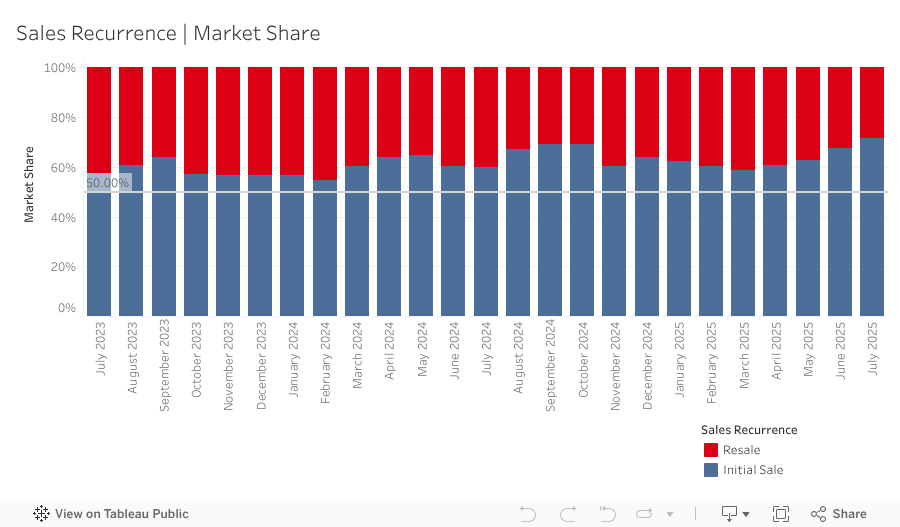

In July, 12,595 off-plan Oqood transactions were recorded, a marked increase of 28.3% from the previous month, in in tandem with the increase in volume, the overall market share also rose to 62.6%, up 3.4% month-on-month. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions represent an even larger market share of 72.1%. Title Deed sale volumes also witnessed a monthly increase, climbing by 11.2% and now account for 37.4% of all sales transactions.

Meanwhile, resale transactions—any subsequent sale of a property following its initial sale by the developer—regardless of whether the first sale was off-plan or completed—stood at 5,564 in July, accounting for 27.7% of the market. This marks yet another monthly decrease, falling by 5.2%. In line with the decrease in overall resale activity, the portion of off-plan resales also moderated, falling to 19.9% and bringing the 12-month rolling average down to 25.7%. After climbing to a high of over 33% in April, off-plan resales have dropped considerably—an interesting development given that initial developer sales market activity remains robust. While this may appear to reflect softer momentum, it also points to a maturing market dynamic. With developers offering attractive incentives and flexible payment plans, resale listings—often priced at a premium to original purchase values—are facing tougher competition. Buyers are becoming more selective, and many are opting for the certainty and benefits that come with buying directly. This trend reinforces the importance of realistic expectations for off-plan investors looking to exit early and highlights that quick resale gains before handover are never a sure thing.

Dubai’s new project pipeline showed no signs of slowing in July, as more than 50 launches brought over 13,800 residential units to market with a combined estimated gross sales value of AED 38 billion. This brings the year-to-date tally to nearly 93,000 units and AED 270 billion in potential sales, levels that would have once defined a full-year cycle but are now being reached in just seven months. Apartments accounted for 95% of July’s new supply, with villas and townhouses contributing 2.5% each. While the continued wave of new supply underscores developer momentum, it is also beginning to test the depth of demand. With many launches offering comparable concepts and pricing, standing out has become more difficult. The result is a market where buyer urgency is easing, and projects that once sold out in hours are now taking longer to move. Rather than a sign of weakening demand, this shift reflects a market that is becoming less hype-driven and more value-focused—one where buyers are taking time to evaluate, compare, and invest more deliberately. Of course, the possibility that seasonal effects are also playing a role shouldn’t be ruled out, particularly during the traditionally quieter summer months.

Mortgage transaction volumes surged in July, setting a new record with a total of 4,891 loans—a 9.2% increase month-on-month. New purchase money mortgages accounted for 45.6% of activity, up 2.3% from June, with average loan amounts of AED 1.8 million and a loan-to-value (LTV) ratio of 73.7%,slightly above June’s 73.5%.Although LTV ratios edged up slightly in July, they remain lower than the historical average of 75–77%, likely reflecting the ongoing influence of Central Bank measures restricting fee and cost financing. These tighter conditions raise the upfront cash hurdle for buyers, but the fact that mortgage volumes hit a new record suggests strong confidence among buyers and a more resilient, well-capitalized demand base. Meanwhile, loans for refinancing and equity release saw their market share increase by 7.5% to 38.3%. The remaining 16.1% (down by 9.8% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 785 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Rabdan Building (311), Shorooq Land 2 (227) in Dubai Land Residence Complex, and England Cluster Building 10 (54) in International City, as well as portfolio mortgage modifications at Silver Tower (26) in Business Bay.

As the third quarter gets underway, Dubai’s real estate market continues to operate at historically high levels of activity, but signs of strain are beginning to emerge beneath the surface. Price growth remains positive, and transaction volumes are on pace to break new records, yet the pace of new supply—particularly from the off-plan segment—raises questions about the market’s capacity to absorb this wave in a sustainable manner.

With nearly 93,000 units launched year-to-date, buyer selectivity is rising, and early indicators of softening absorption are becoming more pronounced. Developers will need to shift focus from velocity to viability, with increased emphasis on product differentiation, delivery timelines, and realistic pricing strategies. Meanwhile, mortgage market dynamics remain a key factor to monitor. Although borrowing activity is strong, the persistence of lower loan-to-value ratios suggests that affordability pressures may start to shape demand more directly in the months ahead.

While the market remains fundamentally strong, sustaining this momentum will depend on aligning supply with end-user demand and placing greater focus on product differentiation and genuine value. The second half of the year will reveal whether the market can adapt to these evolving dynamics or begin to encounter meaningful friction.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |