For the second consecutive year, the typical seasonality of the Dubai market—which historically sees rising temperatures and cooling real estate activity during the summer—was notably absent. Instead, this period experienced continued price growth and significantly high sales and mortgage transaction volumes.

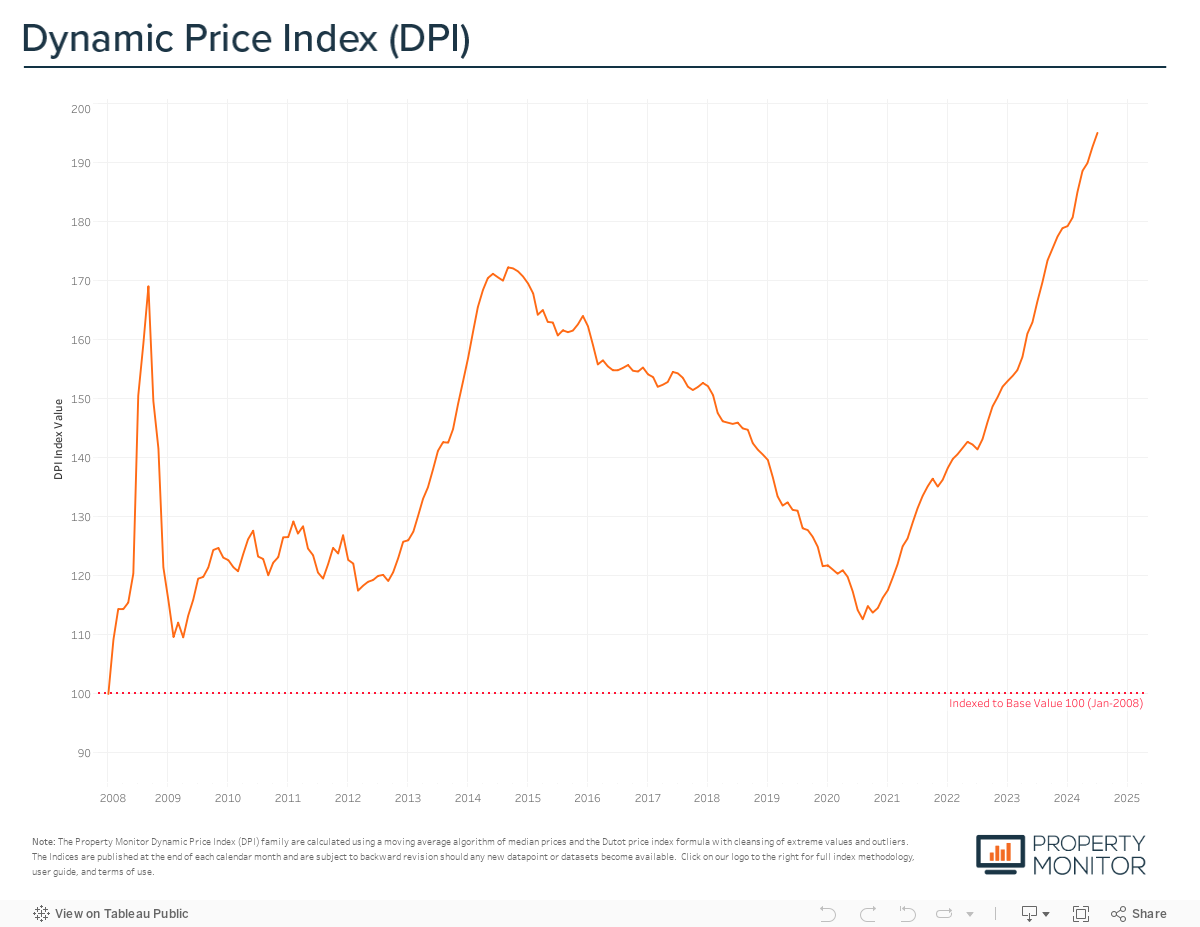

According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices grew by 1.22% in July and currently stand at AED 1,397 per square foot, 13.2% over the previous all-time high and market peak of September 2014.

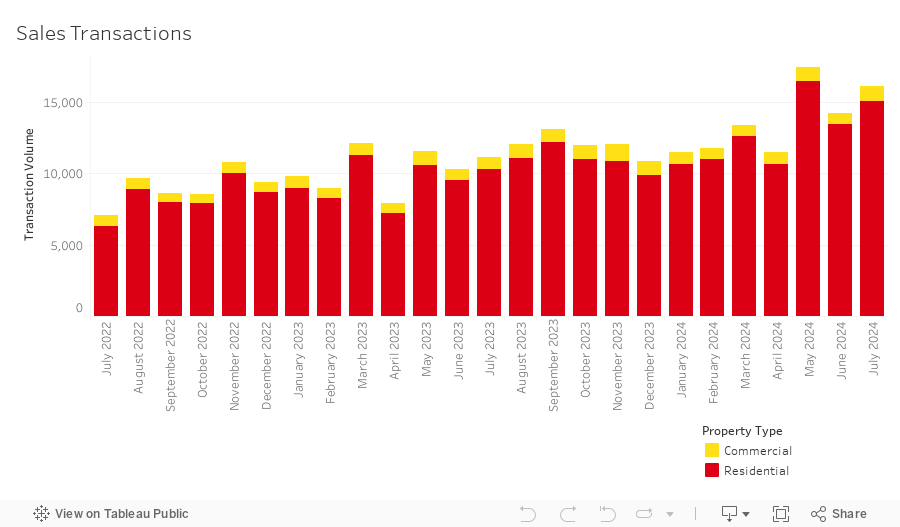

The total volume of sales transactions witnessed an increase of 12.8% in July reaching a total of 16,113 transactions. This sets the mark as the highest volume ever for the month of July and registered as the second highest level ever recorded. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 93.4% (15,046 transactions). The highest transacted commercial property types were hotel apartments (2.5%), office spaces (1.6%), and vacant land (1.3%).

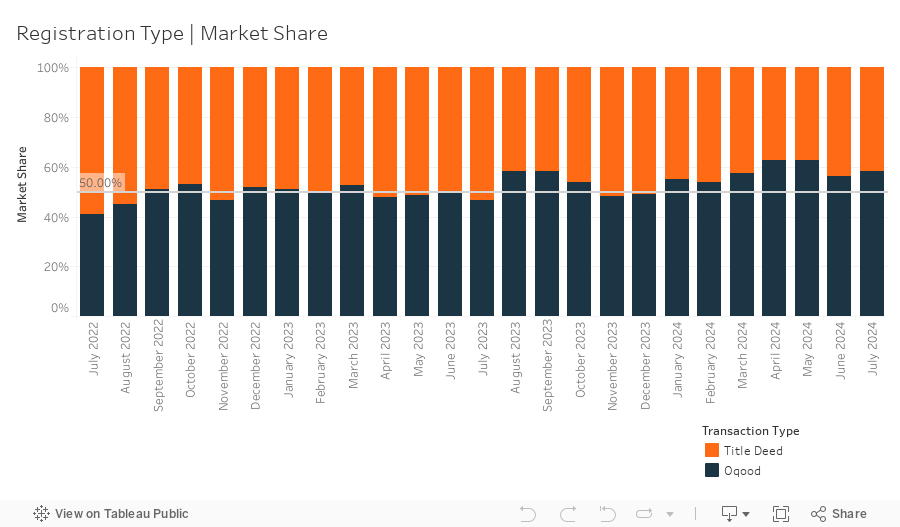

In July, 9,393 off-plan Oqood transactions were recorded, an increase of 17.1% from the previous month and saw a jump in market share to 58.3%. Meanwhile, Title Deed sale volumes also witnessed an increase, growing by 7.2% and now account for 41.7% of all sales transactions. While Oqood transactions are used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions secure an even larger market share of 67.1%.

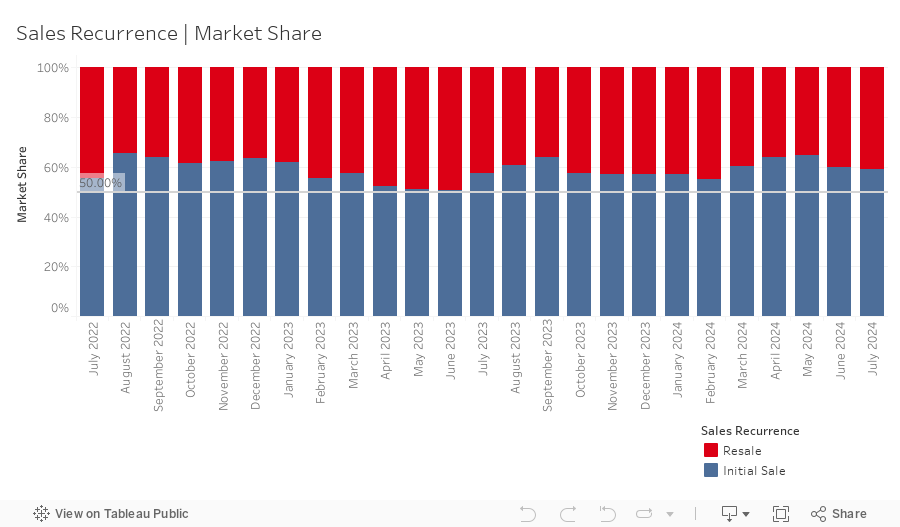

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 6,612 in July representing a market share of 41.0%, increasing slightly by 0.5% month-on-month. With this increase in overall resale activity, the portion of off-plan resales also continued to increase, reaching 25.6% for the month and further pushing the 12-month moving average up to a historic high of 23.8%. We continue to stress that closely monitoring this activity remains important as off-plan resales can be an indicator of increasing speculative activity, particularly if it is in the early days of construction, well before handover. For now, whilst the current level of activity is skewed towards properties that are within a year of anticipated completion, this helps to support a view that there is no immediate cause for alarm.

Preliminary figures for July indicate the introduction of nearly 9,000 new off-plan units to the market, contributing to an already record-breaking total of approximately 68,000 units across over 220 projects this year. This extraordinary level of activity in the off-plan market shows no signs of abating, and is projected to continue at this pace, well on track to surpass last year’s total of ~96,000 units.

Mortgage transaction volumes increased by 20.2% in July with a total of 4,033 loans recorded–the second highest level on record, surpassed only by March 2023. Loans taken for new purchase money mortgages accounted for 53.0% (up 4.8% from last month) of the overall borrowing activity, with the average amount borrowed being AED 1.83m at a loan-to-value ratio of 76.7%. Meanwhile, loans for refinancing and equity release saw their market share increase by 4.3% to 33.8%. The remaining 13.2% (down by 9.1% from last month), was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 534 bulk loans issued for the month were spread across several projects, most notably lease finance registrations at Paradise Views 1 (203) in Majan, Portfolio Mortgage Registrations at Al Ayyan Tower (99) in International City II, and Platinum Tower (34) in JLT, as well as Portfolio Mortgage Development Registrations at Binghatti Views (29) in Dubai Silicon Oasis. Looking ahead, we expect mortgage volumes to stay consistent in the coming months, with the potential for a slight dip as we approach Q4. This dip is likely to be a momentary pause as borrowers wait for rates to fall, anticipating an imminent rate decrease as early as the next US The Federal Open Market Committee (FOMC) meeting in September, with additional cuts likely to follow well into next year. Once interest rates begin to ease, we foresee even greater monthly volumes driven by refinancing activities as rate differentials and refinancing costs begin to make sense.

As we enter the second half of 2024 we anticipate the market will continue its upward trajectory, with moderate price growth and high transaction volumes. While we do not foresee an overall slowdown, the gap between off-plan and completed property sales is likely to widen further. This is partly due to the robust pipeline of off-plan projects, and partly due to the availability of suitably priced inventory.

So far, 2024 has witnessed unprecedented activity in the Dubai real estate market, with transaction volumes reaching record highs every month, except for April, and on track to surpass 170,000 sales by year- end. This exceptional activity has been driven by the expansion of the new development market, with more off-plan launches than days in the year—encouragingly, robust demand from both investors and end- users has resulted in high absorption and sales velocity rates for the majority of projects. As long as these absorption rates remain high, any major shift in the market seems unlikely in the near term. However, bull runs cannot last forever, and it is only a matter of time until the balance of supply and demand starts to shift.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |