The only thing hotter than the weather in July is the Dubai real estate market, buoyed by the unwavering strength of the high-end market. After going into contract in late May this year, the most expensive apartment ever sold in Dubai–Penthouse 1402 at Jumeirah Marsa Al Arab–has closed and transferred for a whopping AED 420 million. July also saw sales of residential properties over AED 10m reaching unprecedented levels: doubling their market share month-on-month to 5.4%; and recording a total of 555 sales, out of which 305 were for ultra-luxury villas at the newly launched District One West community.

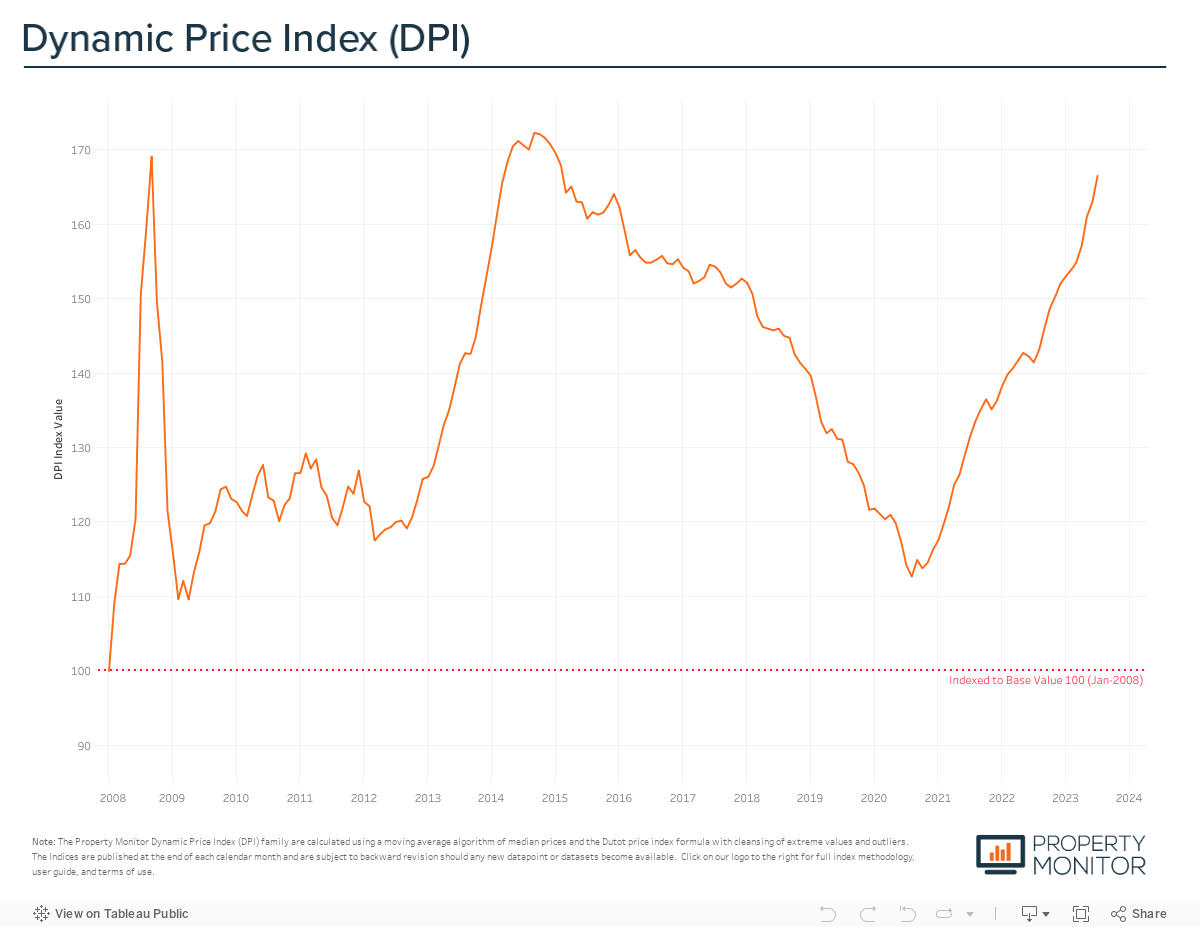

Meanwhile, following a brief period of stabilisation last month, emirate-wide property prices experienced a significant upswing, marking a 2.17% growth in July, which is the second-highest rate of price increase seen in the past two years. According to the Property Monitor Dynamic Price Index (DPI), Dubai property values currently stand at AED 1,192 per square foot, and are now only 3.4% lower than the previous market cycle’s peak in September 2014.

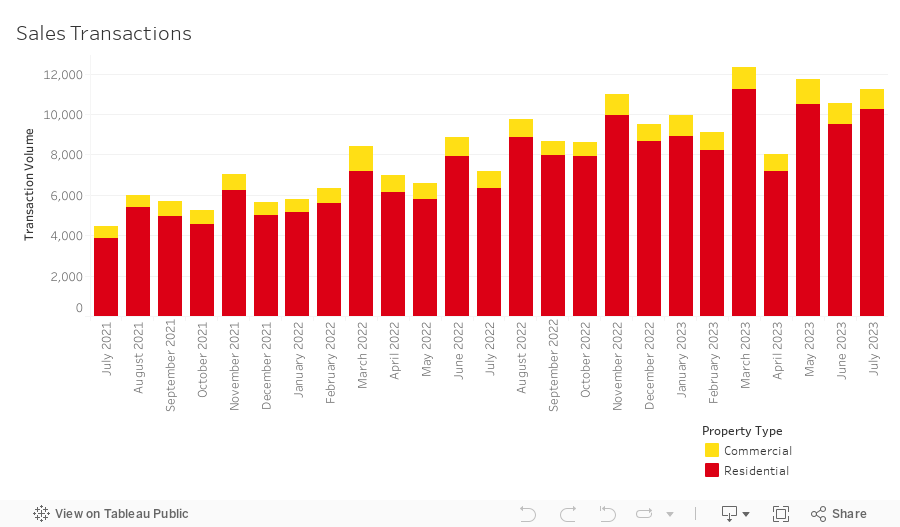

The total volume of sales transactions increased 6.6% month-on-month, reaching a total of 11,228 sales and marks the highest volume ever for the month of July. This further perpetuates the pattern of volatility in monthly transaction volumes that has been witnessed since February this year, frequently showcasing substantial shifts in the range of approximately 1,000 to 4,000 sales per month.

Nonetheless, average monthly transaction volumes for 2023 are exceeding any previously recorded figures, setting the market on track to outperform the highest ever annual sales record established in 2009. We anticipate that we’ll see nearly 120,000 sales recorded by the end of the year. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority at 91.4% (10,261 sales transactions). The highest transacted commercial property types were hotel apartments (3.6%), office spaces (1.9%), and land sales (1.8%).

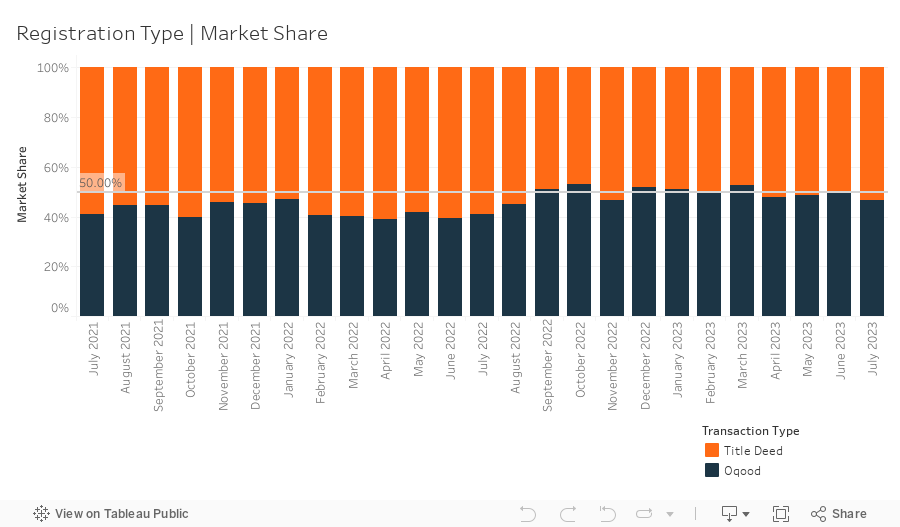

A total of 5,247 off-plan Oqood transactions were registered in July, increasing by 0.8% month-on-month and an impressive 77.4% on a yearly basis. Oqood transactions now account for 46.7% of the market, while Title Deed sale volumes grew to 53.3%. Although the market may appear to be slightly tilted in favour of completed properties over off- plan, after a correctional adjustment by the Property Monitor team for registration technicalities within the Dubai Land Department (DLD), several villa and townhouse sales, presented as completed with issued Title Deeds, were identified as under construction and sold off-plan. In reality, off-plan transactions have held a dominant market share since Q4 2021, currently standing at 60.4%, up from 55.6% last month.

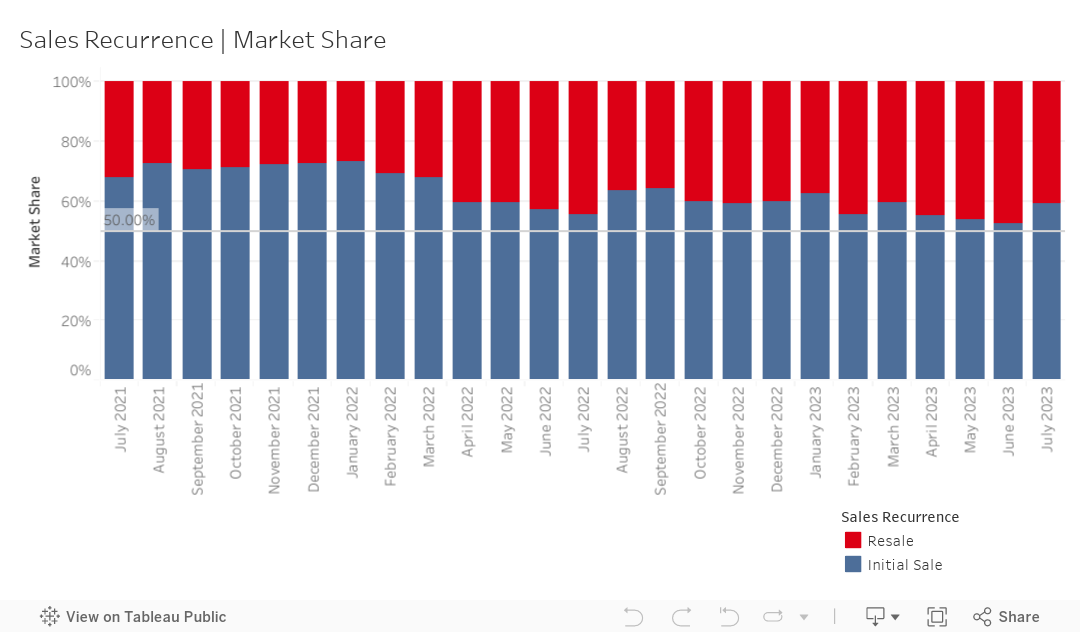

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer for an off-plan or completed project—stood at 4,570 in July, representing a market share of 40.7%, decreasing by 7.2% month-on-month and wiping out the preceding three months of steady growth. While overall resale activity decreased, so too did the portion of off-plan resales—down 1.9% in July—falling to 20.5%. Speculative activity is slowly making up a greater portion of off-plan resales, however most of these resales remain skewed towards properties that are within a year of anticipated completion. With new project launches showing no signs of slowing, and off-plan asking prices not aggressively increasing, there is set to be an ample pipeline of units direct from developer available for the foreseeable future, leaving little to be gained from buying a unit that’s being flipped soon after its initial purchase. It will, however, continue to make sense for those properties that are closer to handover being resold, and the buyer fairly paying a premium in exchange for a property that can be occupied in the near future.

Despite the continued high interest rate environment, mortgage transaction volumes increased by 17.4% in July, with a total of 3,199 loans recorded, marking the third highest monthly volume of mortgage transactions ever witnessed in the Dubai market. An in-depth look at these mortgage transactions reveals that the highest growth segment was for bulk mortgages—those taken by developers and larger investors with multiple units—which grew by 9.2% to 35.5% in July. The 1,134 bulk loan transactions were spread across several projects, most notably portfolio mortgage registrations at Nad Al Sheba Villas in Nad Al Sheba 3, with 909 loans and a total value just shy of AED 2 billion.This is followed by a portfolio of 30 villas and townhouses throughout The Springs and Meadows for a total value of ~AED 107 million. Meanwhile, loans for refinancing and equity release saw their market share drop by 4.6% to 29%. The remaining 35.5% (down 4.6% from last month) of loans taken were new purchase money mortgages, with the average amount borrowed being AED 1.74m at a loan-to-value ratio of 76.1%. While the market share for new purchase and refinance loans declined in July, the amount of loans taken for each remains at historically high levels across all residential property types, indicating strength in the overall mortgage market.

Average gross rental yields for residential properties in the emirate continued to remain relatively stable in July, decreasing by just 0.03% to 6.64%. Yields for both apartment and townhouses saw modest declines down 0.05% to 7.06% and 0.06% to 6.07% respectively, whilst yields for villas experienced a marginal gain, up 0.09% to 4.88%. The marginal shifts in yields and general plateauing align with our forecasts, largely due to several communities seemingly hitting the apex in attainable rental rates, and sales prices leveling off at the same time in certain areas. These areas primarily include those that experienced significant price appreciation in the initial stages of the market recovery. A reprieve for renters is on the horizon, though it might not immediately translate into drastically reduced rents. Instead, the upcoming quarter is likely to see a cessation in rampant rental price increases, followed by a gradual decrease as we approach the year’s end.

As we enter the second half of the year, with both the weather and real estate market scorching hot, what’s ahead in the coming months? As the weather cools will we see some of the steam that’s been driving the market evaporate, or will the market continue to set more records and reach new heights? Absent any extraordinary pressures or events, the latter is most likely with transaction volumes remaining high as a result of the increasing number of new project launches and seemingly endless demand driving sales absorption. The off-plan market is back, and back in an unprecedented fashion. As interest from aboard widens with the return of buyers from the Far East, it is unlikely we will see a slowdown by developers any time soon, however no bull run lasts forever and a shift is inevitable, so better to play it safe.

For investors, it’s important to keep in mind that selling out a project doesn’t guarantee future success, and markets can move in both directions during a 2-4 year construction period. Temper expectations for capital appreciation and yields to accommodate any potential slowdown in the market a few years from now.

For end-users, the most important consideration will generally be monthly affordability, and if you’re buying off-plan, carefully assess the payment plan of the project, plan ahead for any installments and, if you’re counting on taking a mortgage out to cover a balloon payment upon completion, run your numbers at various interest rates. The market may be hot but be sure to keep a cool head

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |