Dubai property prices began the year with a month-on-month decline of 0.57%, marking the first drop in price growth since the summer of 2022, when prices fell by a comparable 0.58% in July. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently average AED 1,484 per square foot, standing 20.3% above the previous market peak in September 2014.

Dubai’s current market cycle has now extended to 51 months, marking over four years of sustained price growth. During this period, monthly appreciation has averaged 1.19%, though price growth has shown clear signs of deceleration in recent months. After peaking in August 2024 with a 2.48% increase, monthly gains steadily moderated, dropping to just 0.48% in November and 0.88% in December, before turning negative in January 2025. This slowdown suggests the market may be approaching a plateau, with further price growth facing headwinds due to affordability constraints, particularly in the ready market. While demand remains strong, the trend indicates a shifting landscape where buyers may become more price-sensitive, and sustained appreciation could be increasingly difficult to maintain.

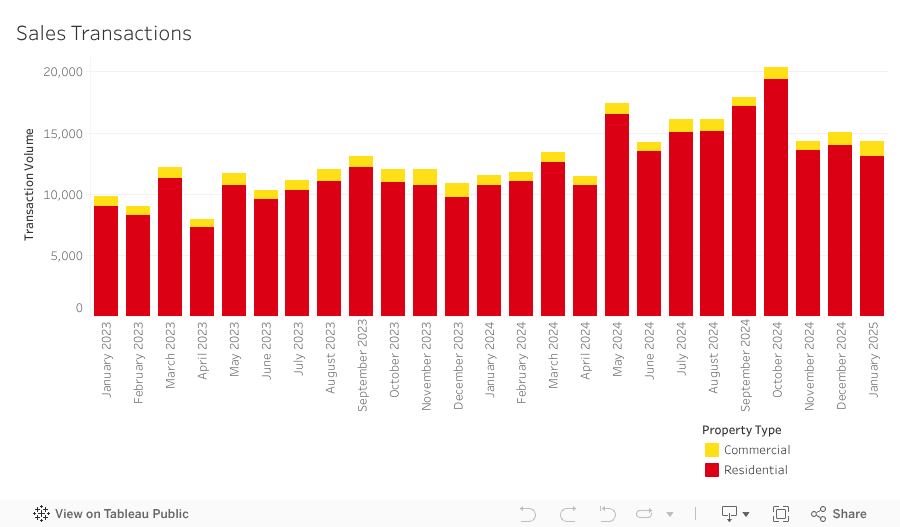

The total number of sales transactions declined by 4.6% in January, reaching 14,413. However, despite this dip, it still stands as the highest transaction volume ever recorded for the month of January. Looking at the broader trend, sales activity steadily accelerated throughout 2024, peaking at an all-time high of 20,460 transactions in October.

Since then, volumes have moderated, suggesting the market has likely settled into a more sustainable level of activity. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at just over 91% (13,124 transactions). The highest transacted commercial property types were vacant land (4.2%), office spaces (1.9%), and hotel apartments (1.2%). Notably, nearly 400 of the 613 land transactions were for plots at DAMAC Islands, likely tied to the subdivision of the master community. While this contributed to a sharp rise in overall land sales, it does not necessarily indicate a genuine surge in market-driven demand, but rather a procedural increase linked to the project’s development phase, temporarily inflating the overall land transaction figures.

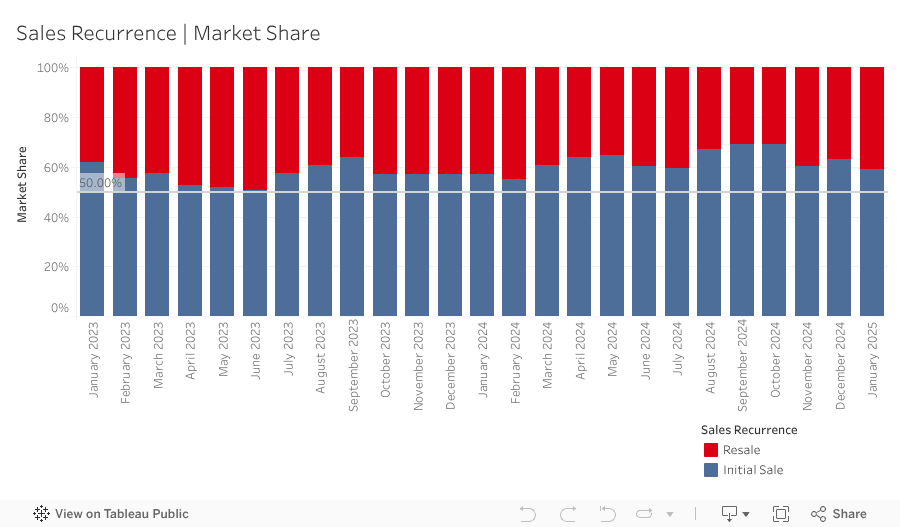

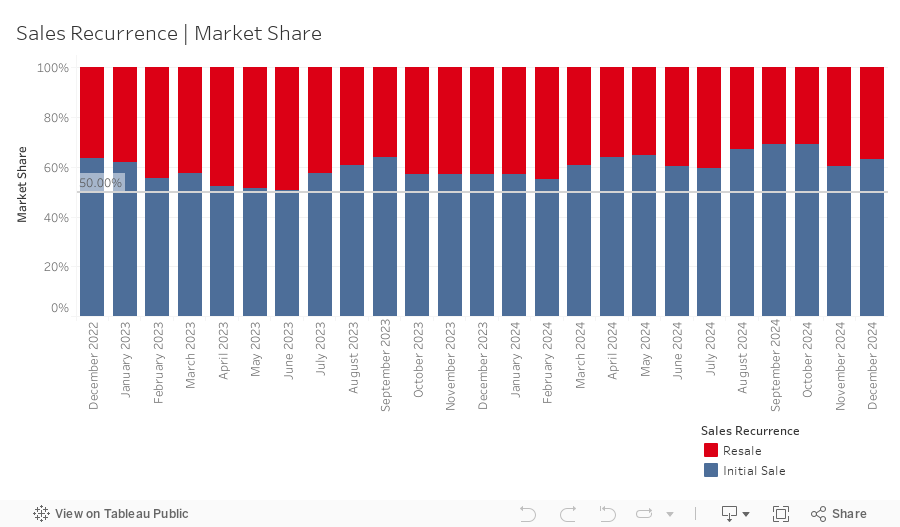

In January, 7,555 off-plan Oqood transactions were recorded, a decrease of 17.7% from the previous month and a decrease in market share to 52.4%. Meanwhile, Title Deed sale volumes witnessed a marked increase, rising by 15.7% and now account for 47.6% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions secure an even larger market share of 67.6%.

Meanwhile, resale transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 5,561 in January, accounting for 38.6% of the market. This marks a 1.7% increase month-on-month. While overall resale activity increased, the portion of off-plan resales decreased to 27.7%, bringing the 12-month rolling average to 24.3%. Off-plan resale activity has seen a steady yet gradual rise over the past three years. As in previous months, the bulk of these resales remain concentrated in properties nearing completion within the next 12 months, reflecting sustained end-user and investor demand rather than purely speculative trading. However, there are signs of a gradual expansion, with resale activity slowly extending to properties further from handover—around 15 to 16 months out—a trend that, if it continues, could signal a shift toward increased speculation in the market.

Preliminary figures for January indicate the introduction of just over 12,400 off-plan units to the market for sale, continuing the fierce pace witnessed throughout 2024. These units came from 53 project launches by 37 different developers, highlighting the broad and sustained expansion of the off-plan segment. Apartments again dominated the unit mix, accounting for 86.7% of new inventory, while townhouses and villas represented 11.6% and 1.7%, respectively. Activity in the off-plan market remains strong and shows no signs of slowing in the near term. With over 250 additional projects currently in the planning phase, as tracked by the Property Monitor team, this momentum is expected to continue well into the foreseeable future.

Mortgage transaction volumes increased by 6.8% in January with a total of 4,1341 loans recorded. During the month, loans taken for new purchase money mortgages accounted for 41.9% (down 1.9% from last month) of borrowing activity, with the average amount borrowed being AED 1.97m at a loan-to-value ratio of 76.4%. Meanwhile, loans for refinancing and equity release saw their market share increase by 3.0% to 28.4%. The remaining 29.7% (down by 1.1% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 1,228 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Sway Residences (217) in Dubai Hills, Domus Indigo 1 & 2 (209) Dubai Production City, and Blue Wave Tower (139) in Dubai Residence Complex.

Dubai’s real estate market remains on solid footing, however sustaining long-term growth will require a careful balance between supply and demand to avoid oversaturation. Government initiatives such as the Dubai Economic Agenda (D33) and the Real Estate Sector Strategy 2033 provide long-term confidence, but as the market matures, a shift toward stability over rapid gains is expected.

Affordability constraints in the ready market and stabilising transaction volumes suggest price appreciation may continue to moderate. Rather than the uninterrupted increases seen in recent years, 2025 is likely to bring a more measured trajectory focused on liquidity and strategic development

In the mortgage market, the UAE Central Bank’s recent reinforcement of regulations preventing broker fees and DLD transfer fees from being included in mortgage amounts has yet to impact LTV ratios. However, stricter enforcement could affect borrowing power in the coming months, adding further affordability pressures.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |