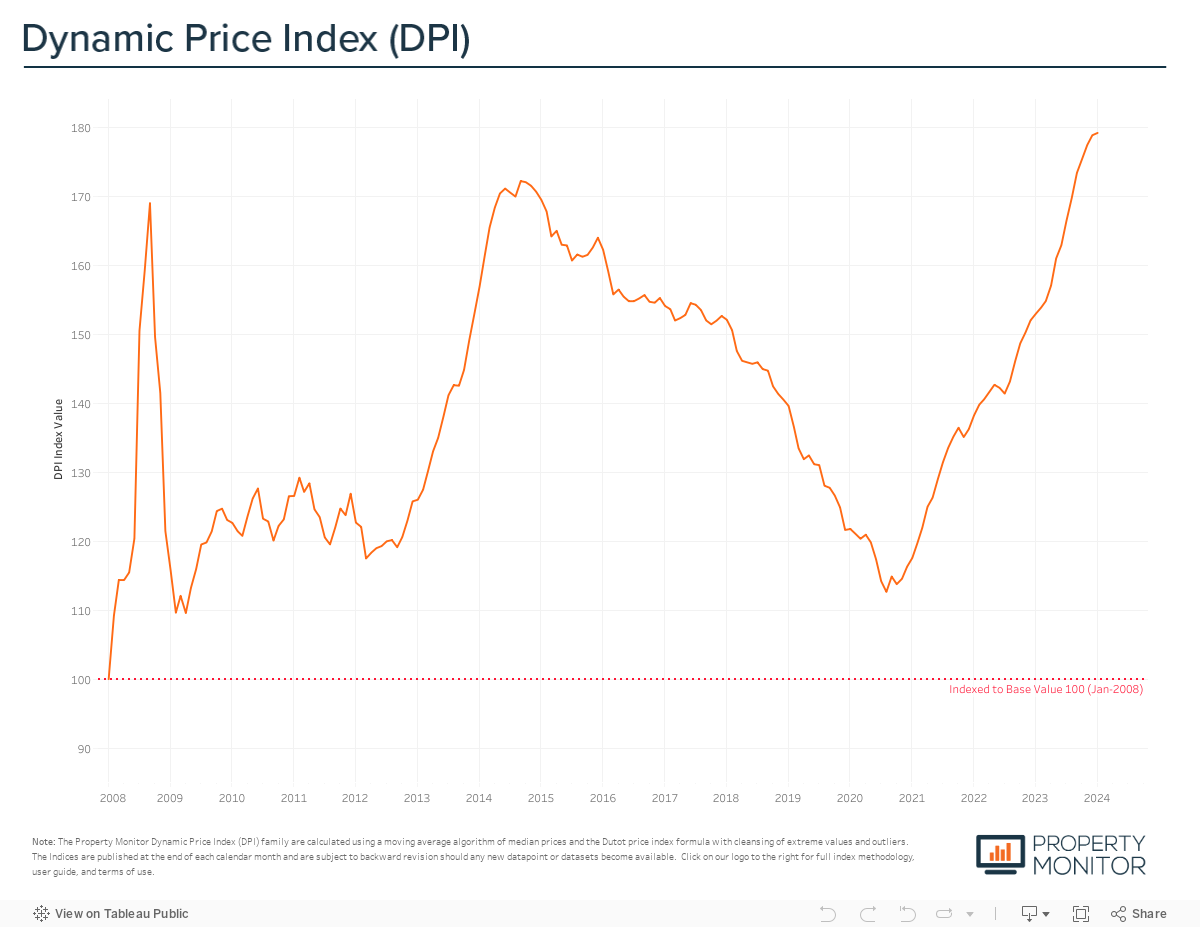

After ending 2023 with a decade high annual price growth of 16.4%, the Dubai real estate market opened the year with a meagre 0.2% month-on-month increase in average property prices. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently stand at AED 1,284 per square foot, just over 4% above the previous all-time high and market peak of September 2014.

In the 39-month period since bottoming out in October 2020, prices have gone on to increase 45.8%—averaging 1.2% per month—and while we anticipate the market to continue in a general upwards trajectory, our forecast for 2024 is that the pace of price appreciation will slow and end the year up between 5-8%.

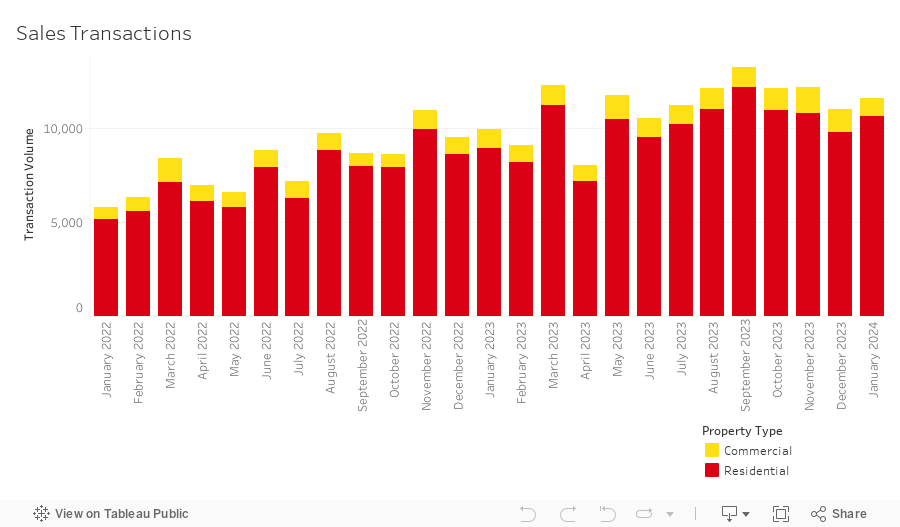

In January, the total volume of sales transactions increased 5.4% month-on-month, rising to a total of 11,615 sales and recorded as the highest volume ever for the month of January—surpassing the record that was set just last year by 16.8%. Residential transactions, encompassing apartments, townhouses, and villas, accounted for most sales at 91.7% (10,647 transactions), while the highest transacted commercial property types were hotel apartments (3.4%), land sales (1.9%), and office spaces (1.8%).

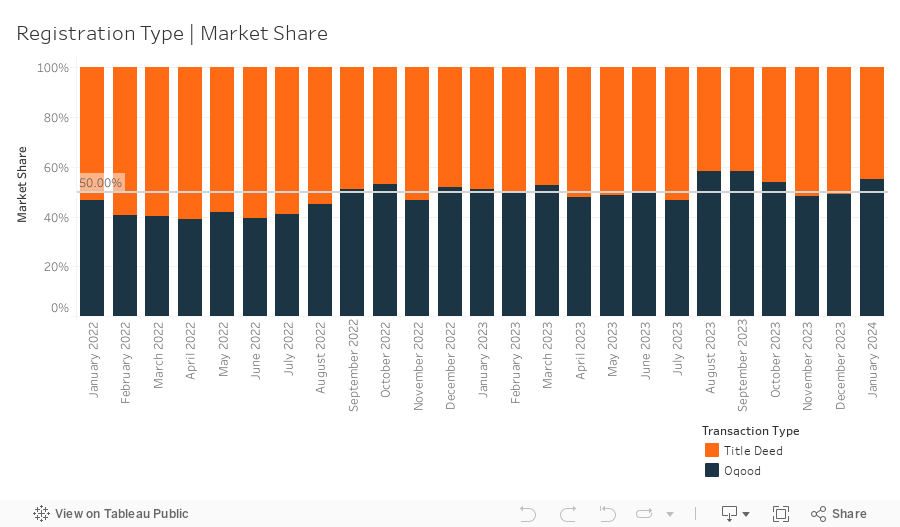

A total of 6,413 off-plan Oqood transactions were registered in January, marking an 18.8% month-on-month increase in volume and a 6.2% increase in market share to reach 55.2%. Meanwhile, Title Deed sale volumes witnessed a decrease, falling by 7.4%, and now account for 44.8% of all sales transactions.

While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions hold an even more dominant market share of 61.8%, returning to pre-pandemic levels.

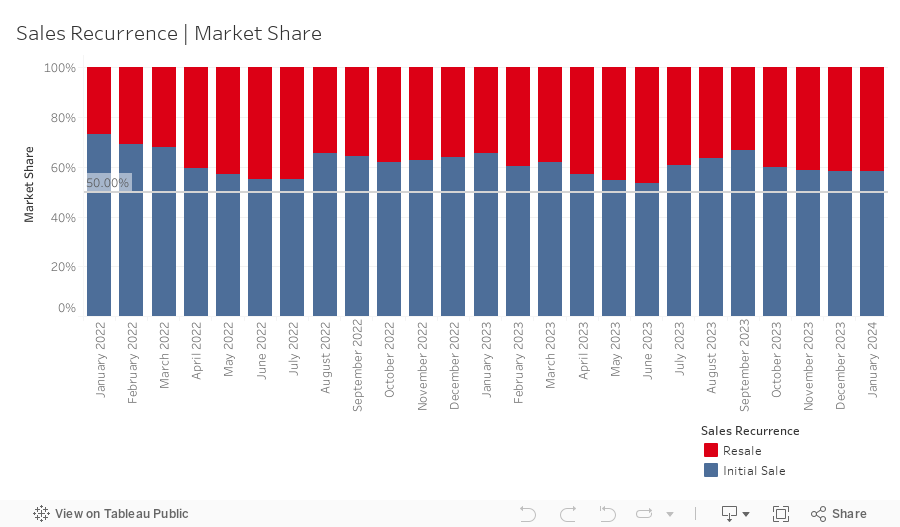

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 4,851 in January. This represents a market share of 41.8%, static month-on-month, with initial developer sales maintaining their dominant market share.

New off-plan development project launches remain at record highs in January, with just over 11,500 off-plan units added to the market for sale at an anticipated combined gross sales value of ~AED 31.1 billion. Apartments represent 93.3% by volume of this new inventory, while townhouses and villas represent 6.2% and 0.5% respectively. In 2023, new project launches exceeded just over 95,000 units and AED 272 billion in aggregate sales value which, when completed, will increase the total number of residential dwellings by almost 13%, adding to what is already slated to be a very robust pipeline of units entering the market in the years ahead.

Led by a 32.7% month-on-month increase in borrowing for apartments, mortgage transaction volumes increased 16.6% in January with a total of 3,018 loans recorded. Bulk mortgage loans—those taken by developers and larger investors with multiple units—were a significant attributor to this increase, seeing their market share grow by 3.3% to 22.3%. The 672 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations in Etlala Residence 1 (274) in Dubai Residence Complex, Sandy Avenue (85) in International City II, and RP Heights (72) in Downtown Dubai.

Meanwhile, loans for refinancing and equity release saw their market share increase by 1.6% to 37.9%. The remaining 39.8% (down 4.9% from last month) of loans taken were new purchase money mortgages, with the average amount borrowed being AED 1.62m at a loan-to-value ratio of 76.1%.

Looking forward, while we believe the market has longer to run and that prices in 2024 will end the year higher than current levels, we anticipate ongoing moderation in price appreciation and a greater divergence between the off-plan and existing homes markets. Price appreciation of ready single-family homes (villas and townhouses) continue to show signs of slow down and plateau, while ready apartments—particularly in popular established communities—appear on track to experience more pronounced rates of growth, with value purchases still prevalent after taking longer to begin their initial recovery.

Off-plan sales are poised to further dominate the market for the foreseeable future, with project launches moving full steam ahead and buyer demand remaining high. With over 150 projects in the planning and pre-launch phases being tracked by the Property Monitor team, the breakneck pace of new project launches is on course to continue for at least the first two quarters of the year, and with it an increase of new and smaller developers bringing projects to market. Additionally, tracking of recent land sales of both individual plots for multi-family buildings as well as large super-plots intended for development of master communities provides evidence for even greater growth of off-plan launches.

We expect to witness a new wave of development in several areas across the emirate with Majan, Motor City, Liwan, Dubai Land Residence Complex, and Jumeirah Garden City set to a see significant increase in apartment project launches. While District 11 MBR City, The Valley, Dubai South, and The Oasis will see new launches of villas and townhouses. New master communities are expected to be announced in the south-west areas of Dubai where the Arabian Canal was originally slated to be developed. Keep an eye on Al Yalayis 5, Al Selal, DIP 2, and other areas along the E611 corridor for the next phase of expansion of the emirate.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |