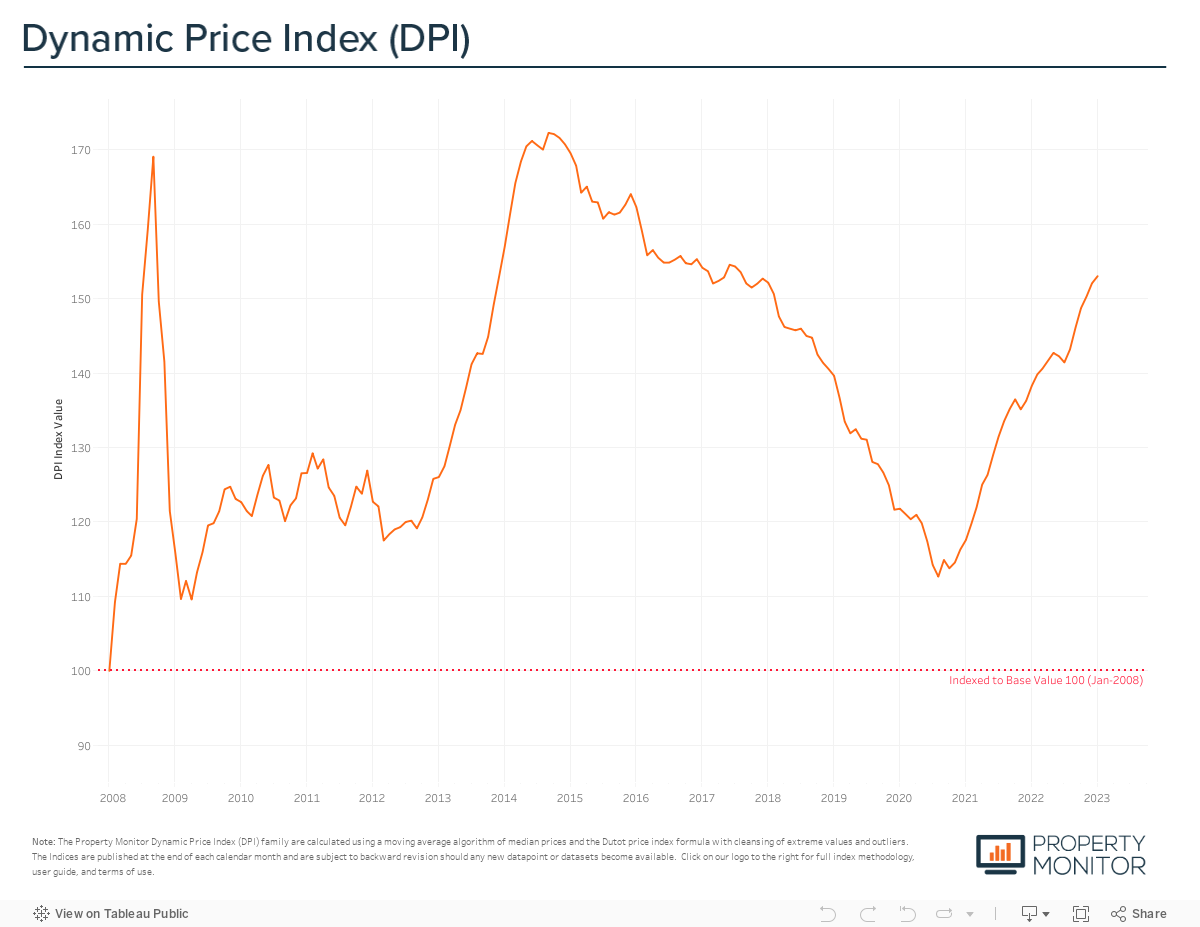

The Dubai real estate market kicked off the year with continued, albeit moderated, growth in property prices by recording a 0.62% increase in January. Dubai property values currently stand at AED 1,096 per sq ft according to the Property Monitor Dynamic Price Index (DPI), back to a level not seen since December 2013 during the last market upswing and in August 2017 on the downcycle.

In the 27-month period since the market bottomed out in November 2020, overall property price growth has now reached 29.9%, averaging 0.92% per month in 2022 and 1.33% per month in 2021. The diminishing monthly rate of price appreciation can be viewed as a positive sign, especially when compared to the previous market cycle—where the recovery and growth phases only lasted 24-months—and price appreciation was averaging 1.6% per month before topping out in September 2014.

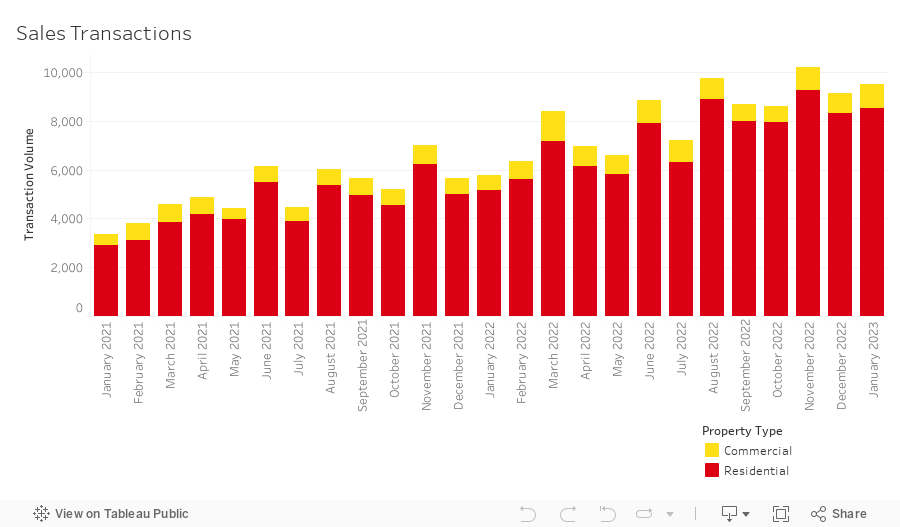

After surpassing 10,000 transactions in November 2022, the total volume of sales transactions declined for a second month in a row, falling a further 0.6% in January to 9,080 sales. However, transactions for the month still reached a level that marks the strongest January on record, eclipsing the record set only last year by over 3,000 transactions. Residential transactions—those for apartments, townhouses, and villas—accounted for 90.3% (8,195 sales transactions) of the total, with hotel apartments (4.2%), offices (2.1%), and land sales (2%) being the highest transacted commercial property types.

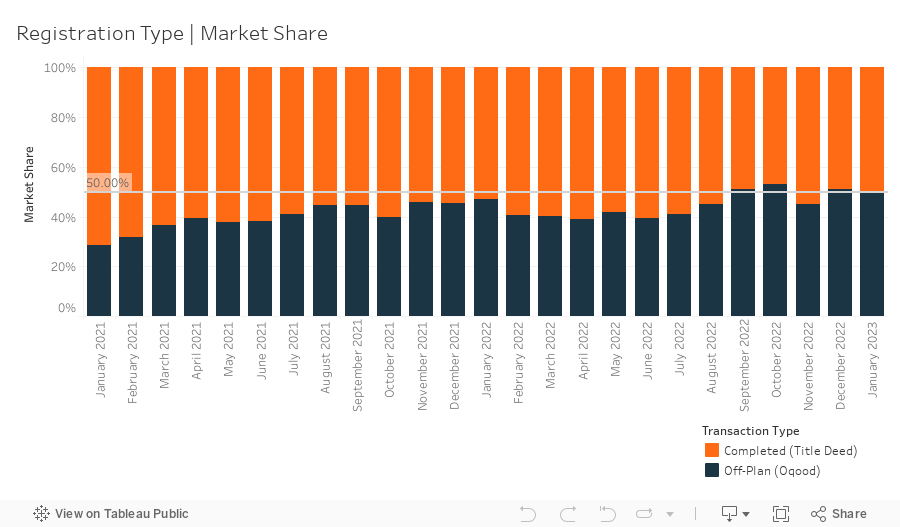

A total of 4,509 off-plan Oqood transactions were registered in January, decreasing by 3.1% month-on-month, yet increasing by a noteworthy 66.4% on a yearly basis. Oqood transactions now account for 49.7% of the market, while Title Deed sale volumes rose to 50.3%. As we’ve previously reported, first impressions may point to a market that is spilt relatively evenly between off-plan and completed properties, after we adjust for registration technicalities with the Dubai Land Department (DLD)—where several villa and townhouse sales are presented as being completed and with Title Deeds issued, when they are in fact under construction having been sold off-plan—the accurate breakdown of market share is 59.1% in favour of off-plan. This key market insight, exclusively provided by Property Monitor experts, is important to track and assists in understanding the changing market dynamics.

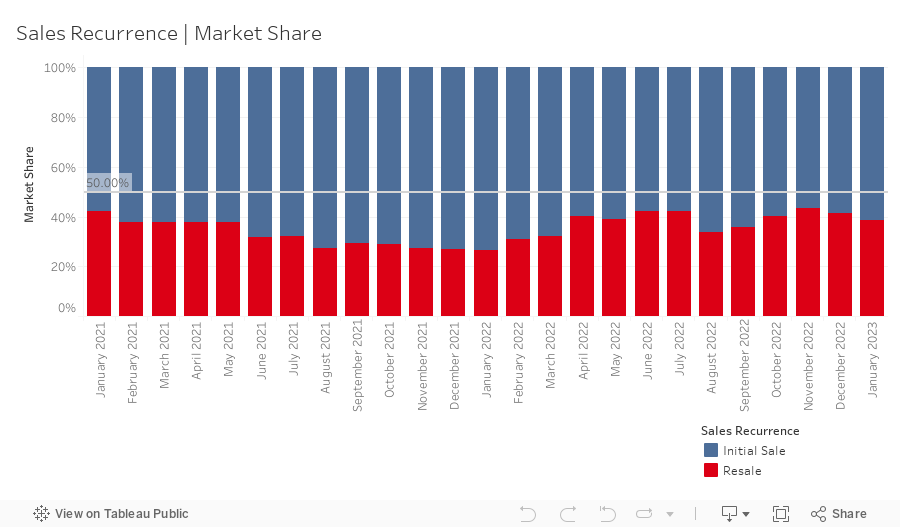

Meanwhile, resale transactions—any subsequent sale of a property that follows the initial first-time sale from the developer for an offplan or completed project—stood at 3,636 in January, representing a market share of 40%, falling 1.3% month-on-month. While overall resale activity has declined, the portion of off-plan resales continues to grow, shooting up significantly in January to 25.9% (from 19.7%). Offplan resales can be an indicator of an increase in speculative activity, particularly if it’s in the early days of construction, well before handover. Early-stage ‘flipping’ can cause price appreciation to accelerate at a pace that is not sustainable, which can ultimately lead to a shortening of the upward phases of the market cycle, and runs the risk of a bubble bursting scenario unfolding.

New off-plan development project launches remain at record highs, with just over 9,500 off-plan units added to the market for sale at an anticipated combined gross sales value of ~AED 24.8 billion. Apartments represent 73.7% by volume of this new inventory, while townhouses and villas represent 25.8% and 0.5% respectively. Over the last 12-months, new project launches exceeded just over 60,000 units and AED 173 billion in aggregate sales value, leading to an 8% increasein the total number of residential dwellings.

Despite ongoing interest rates hikes, several lenders in the UAE recently lowered rates on 3-year and 5-year fixed products by anywhere from 30- 50 basis points, and as a result the volume of mortgage transactions increased in January, up by 5.6% month-on-month to 2,421 loans recorded, reaching their highest monthly level since August 2021. A more detailed look at the mortgage market reveals that the highest growth segment was for loans for refinancing and equity release, increasing their market share by 2.9% month-on-month to 34.2%, while bulk mortgages—those taken by developers and larger investors with multiple units—fell slightly to 36.1% (down 0.5%), while the remaining 29.7% (down 2.4% from last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED1.84m at a loan-to-value ratio of 76.4%.

In January, Emirate-wide average gross rental yields for residentialproperties held relatively firm, increasing by just 0.01% month-on-month to 6.65%. Yields for apartments and townhouses both saw minor increases, rising by 0.02% and 0.01% to 7.03% and 6.31% respectively, while villa yields decreased by 0.09% to 5.31%. These yield results are in line with our predictions made last month for residential yields to experience small-to-moderate growth as we head into 2023. Furthermore, we expect to continue to see some downwards pressure on yields further into the year, with rental prices cooling off as several projects handover, bringing much needed ready supply to the market.

Looking forward, while we believe the market has further to run and that prices in 2023 will end the year higher than current levels, we anticipate continued moderation in price appreciation and gradual tapering down of transaction volumes through the year. The ongoing shift towards off-plan sales dominating the market seems set to continue for the

foreseeable future, with project launches moving full steam ahead and buyer demand remaining high.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |