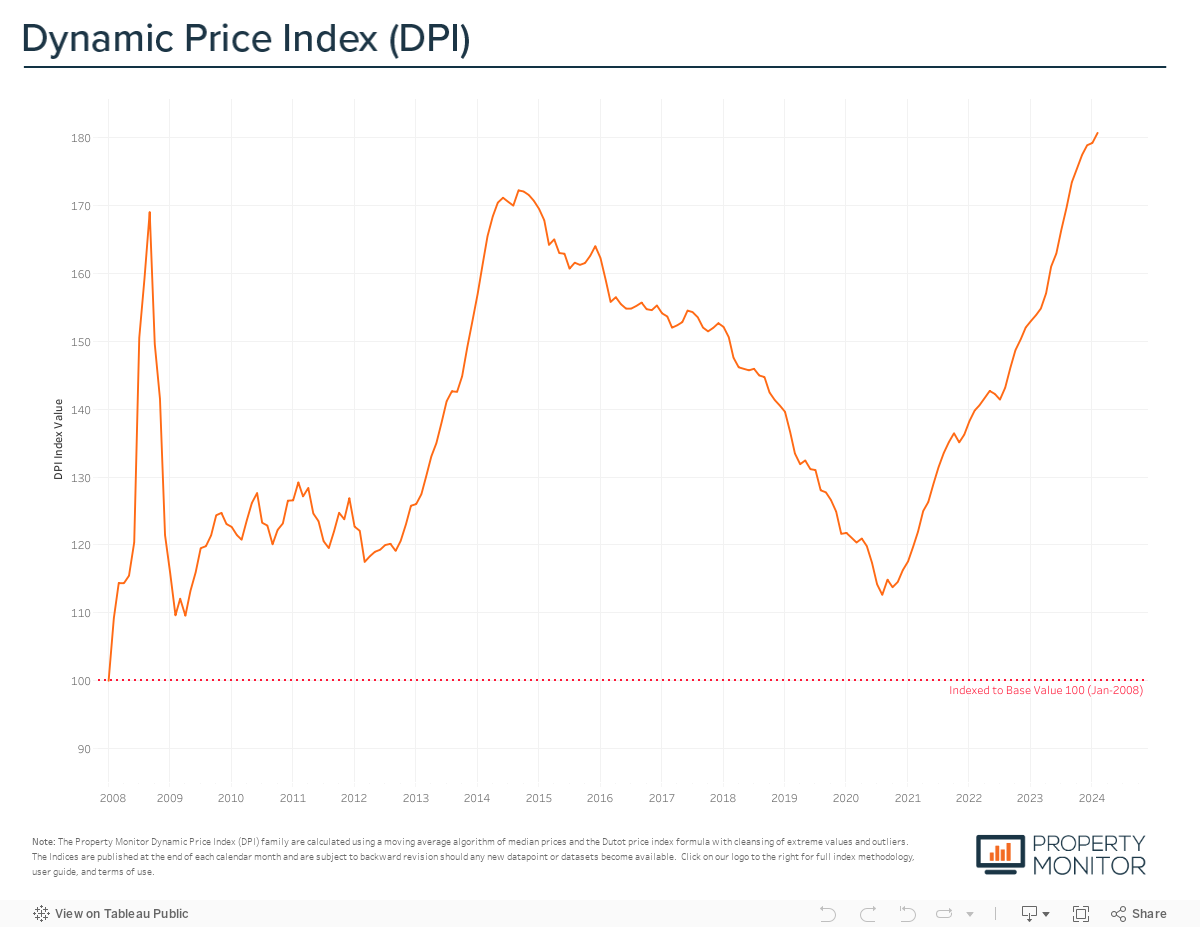

Dubai property price growth continued its modest trajectory in February with a monthly gain of 0.83% recorded. This follows last months’ meagre 0.2% increase and aligns with our forecast for an overall slowing in price appreciation and annual gains anticipated to reach between 5-8%. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently stand at AED 1,294 per square foot, a little shy of 5% over the previous all-time high and market peak of September 2014.

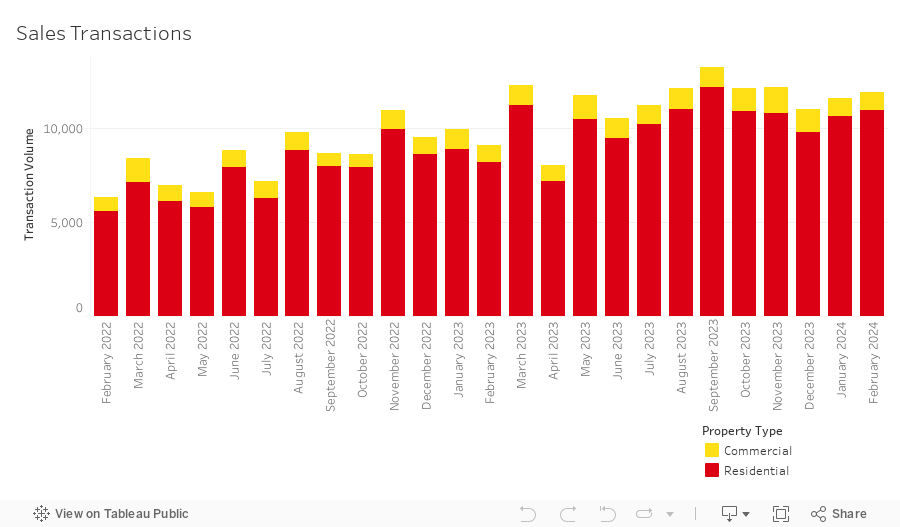

While price appreciation remains subdued, the monthly volume of sales transactions continues to power on, increasing by 2.6% in February, rising to a total of 11,913 sales and recording as the highest volume ever for the month of February. This new record eclipses that which was set just last year by a whopping 30.4%. Residential transactions, encompassing apartments, townhouses, and villas, accounted for most sales at 92.1% (10,966 transactions). The highest transacted commercial property types were hotel apartments (2.8%), office spaces (2.2%), and land sales (1.7%). The consistently high sales volume is fueled by seemingly endless demand for off-plan properties, with particular strength in the apartment segment where sales volumes are moving in an uninterrupted upwards direction. Meanwhile, villa and townhouse activity remain flat by comparison, however we believe this has more to do with supply constraints than any shortfall in buyer demand.

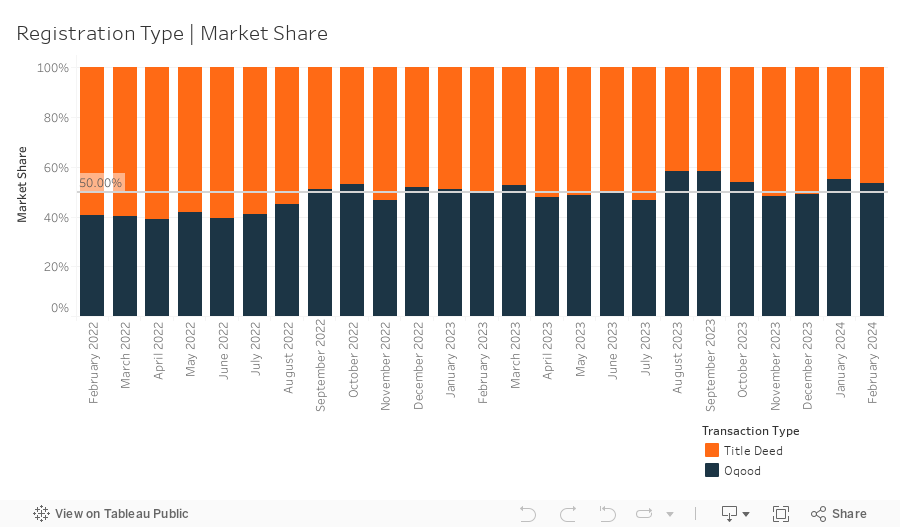

A total of 6,384 off-plan Oqood transactions were registered in January, marking a minor 0.5% month-on-month decrease in volume and a 1.6% decrease in market share, falling to 53.8%. Meanwhile, Title Deed sale volumes witnessed an increase, rising by 6.3% and now account for 46.4% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, offplan transactions hold an even more dominant market share of 59.8%, sitting right at the general long-term split between the off-plan and existing sales segments.

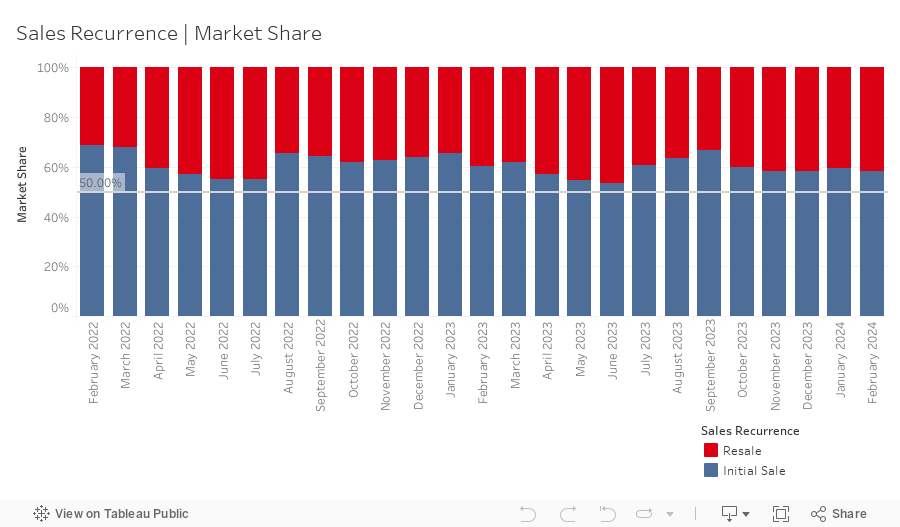

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 4,970 in February. This represented a market share of 41.7%, relatively static month-on-month, with initial developer sales maintaining their dominant market share of 58.3%, up just 0.1%.

Preliminary numbers for new off-plan project launches in February show close to 10,000 units being added to the market for sale throughout the month, with the bulk of launches being for apartments. Launches for single-family homes (villas and townhouses) have represented roughly 15% of new units brought to market in the current market cycle and remain a segment that is undersupplied, however this may soon be addressed.

As we reported last month, our tracking of recent land sales, and more specifically large “super” plots provided an indication that new master communities were on the horizon, something which has now been confirmed with Emaar announcing two new communities—The Heights Country Club and Grand Club Resort—as well as one other forthcoming in May from DAMAC. These projects, all located in southwest areas of Dubai along the E611 corridor, are set to add much needed villa and townhouse supply to the market, as well as usher in the next phase of expansion for the emirate.

Mortgage transaction volumes decreased by just under 5% in February with a total of 2,868 loans recorded. Loans taken for new purchase money mortgages accounted for 46.1% (up 6.3% from last month) of borrowing activity, with the average amount borrowed being AED 1.77m at a loan-to-value ratio of 75.6%. Meanwhile, loans for refinancing and equity release saw their market share decrease by 0.3% to 37.6%. The remaining 16.3% (down by 6% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 468 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at The Neighborhood (48) and Ashjar (46) in Al Barari, as well as portfolio mortgage modifications at Domus Indigo (216) in Dubai Production City and The Sustainable City (34). With the US Federal Reserve holding rates steady at their last 4 meetings and unlikely to change tack until the tail end of the year, overall mortgage activity will likely remain close to current levels with some minor fluctuations. As rates begin to fall, we anticipate that mortgage activity will surge to reach all-time highs, initially with new purchases and then, once rates drop by 75-100 basis points, refinancing will overtake and dominate lending activity.

Looking ahead, our perspective remains optimistic, anticipating a sustained and reasonable growth in property values, with a minimal likelihood of a market bubble. Nevertheless, there will come a juncture when the expansion phase plateaus, transitioning into a phase characterised by hyper-supply. During this period, the delicate equilibrium between supply and demand will shift, leading to a decline in prices. Such fluctuations are inherent in any real estate market and form part of its natural cycle. The critical questions revolve around the timing of this transition, the characteristics of the market downturns, and the duration of these phases.

Despite the seemingly rapid pace of new project launches, raising concerns about potential supply imbalances, the absorption rate remains robust. Both end-users and rental investors are swiftly acquiring the newly launched units. Notably, speculative activity has not gained significant traction, with off-plan resales primarily occurring for units nearing the 12-month handover mark—a crucial aspect to monitor closely.

In addition to off-plan resales, key data-driven indicators warrant careful attention in the coming months. These include a notable deceleration in monthly sales transaction volumes, a slowdown in the absorption of new units from prominent developers, and a general uptick in developer incentives and concessions, such as giveaways, post-handover payment plans, and developers covering DLD transfer fees. The occurrence of several of these indicators could signal an impending market shift.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |