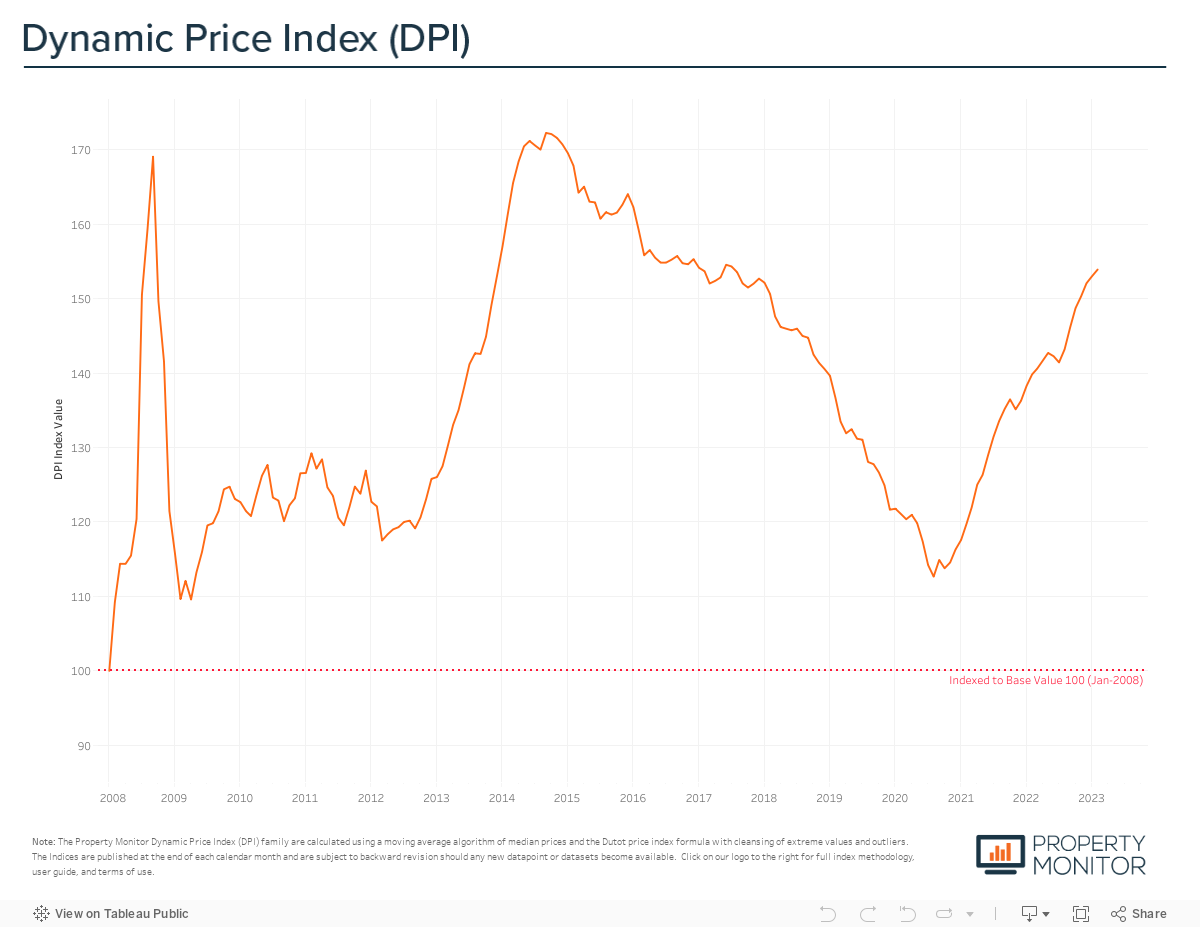

Property price growth in Dubai continued in February with monthly gains of 0.58% recorded, representing the smallest monthly increase since July last year, surely a welcomed point for many home buyers. Dubai property values currently stand at AED 1,102 per sq ft according to the Property Monitor Dynamic Price Index (DPI), up just over AED 100 per sq ft compared to the same time last year, and back to a level not seen since December 2013 during the last market upswing.

Since the market bottomed out in November 2020, overall property price growth has now reached 30.5%, averaging 0.60% per month this year, 0.92% in 2022, and 1.33% in 2021. The diminishing monthly rate of price appreciation can be viewed as a positive sign, especially when compared to the previous market cycle—where the recovery and growth phases only lasted 24-months—and price appreciation was averaging 1.6% per month before topping out somewhat abruptly in September 2014. At an emirate-wide level, property values now sit 10.7% below the previous market peak. Should the market continue to appreciate at a sustainable pace, we continue to believe the market has further to run and that the overall growth period will surpass that of 2014 before finding a new level.

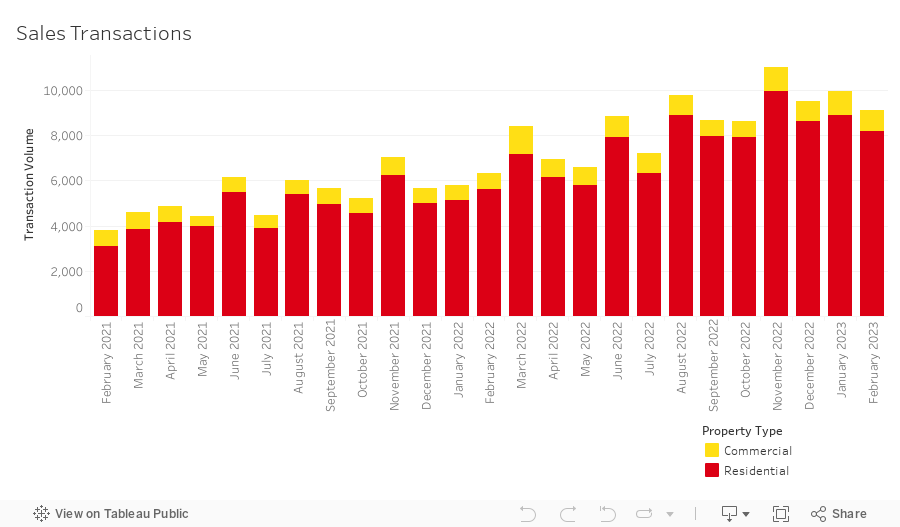

The total volume of sales transactions fell sharply in February, declining by 8.2% to 9,128 sales, however, still reached a level that marks the strongest February on record, eclipsing the record set only last year by a staggering 43.8%. This decline was anticipated as monthly volumes have been on an upwards trajectory for the past two quarters and it was inevitable that the pace would eventually be curtailed. Residential transactions—those for apartments, townhouses, and villas—accounted for 89.9% (8,203 sales transactions) of the total, with hotel apartments (4.8%), office (2.1%), and land sales (2%) being the highest transacted commercial property types.

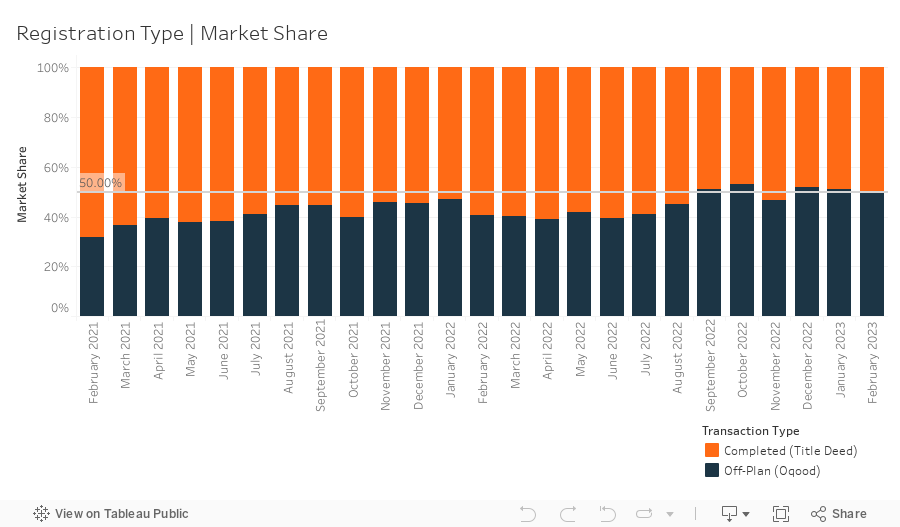

A total of 4,551 off-plan Oqood transactions were registered in February, decreasing by 10.2% month-on-month yet increasing by a noteworthy 76.7% on a yearly basis. Oqood transactions now account for 49.9% of the market, while Title Deed sale volumes rose to 50.1%. As we have previously reported, first impressions may point to a market that is spilt relatively evenly between off-plan and completed properties. However, after we adjust for registration technicalities with the Dubai Land Department (DLD)—where several villa and townhouse sales are presented as being completed and with Title Deeds issued, when they in fact under construction having been sold off-plan—the accurate breakdown of market share is 58.9% in favour of off-plan.

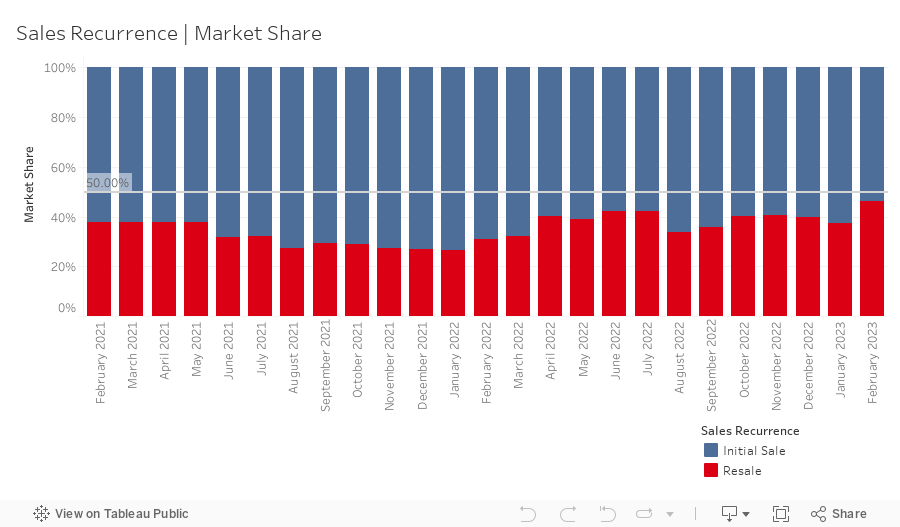

Meanwhile, resale transactions—any subsequent sale of a property that follows the initial first-time sale from the developer for an off-plan or completed project—stood at 4,230 in February, representing a market share of 46.3%, increasing 9.1% month-on-month. With this increase in overall resale activity, the portion of off-plan resales continues to grow—up an additional 1.8% in February—reaching 28.3%. Off-plan resale activity is an important metric to watch in the growth phase of the market, as it serves as an indicator of speculative activity which can drive prices up at an accelerated pace that is not sustainable. Whilst growing each month, this current level of activity is skewed towards properties that are within a year of anticipated completion, and the premium that sellers are making on such sales are relatively commensurate with overall market appreciation and the price of available ready comparable properties. Should activity move towards properties that are further away from handover, caution should be taken as this is likely driven by speculators looking for a quick flip at prices that may not be in line with market values at handover.

New off-plan development project launches continue full steam ahead with just under 5,200 off-plan units added to the market for sale at an anticipated combined gross sales value of ~AED 20.7 billion. Apartments represent 78% by volume of this new inventory, while villas and townhouses represent 11.3% and 10.7% respectively. Year-to-date new project launches are just shy of 15,000 units and have surpassed AED 45 billion in aggregate sales value.

Despite the high interest rates environment, the volume of mortgage transactions remained high in February with a total of 2,477 loans recorded, their second highest monthly level since August 2021. A more detailed look at the mortgage market reveals that the highest growth segment was for bulk mortgages—those taken by developers and larger investors with multiple units—increasing their market share by 2.3% month-on-month to 38.4%. The 951 loan transactions were spread across several projects, most notably Garden View Villas (392) in The Gardens, Al Ghaf Residence (142) in Arjan, and Warsan 1 (114). Meanwhile, refinancing and equity release also increased their market share, growing by 1.5% to 35.7%. The remaining 25.9% (down 3.8% from last month) of loans taken were new purchase money mortgages, with the average amount borrowed being AED 1.72m at a loan-to-value ratio of 77.2%.

In February, emirate-wide average gross rental yields for residential properties held relatively firm, decreasing by just 0.01% month-onmonth to 6.64%. Yields for apartments saw a minor decrease of 0.01% falling to 7.02%, while villa yields fell to their lowest level in seven months down 0.22% to 4.88%. There was no change for townhouses with yields holding at 6.31%. The fall in villa yields can be attributed to sale values remaining high with a bid-ask spread yet to narrow significantly and rental rates appearing to have reached their peak after rapidly increasing over the past 18-24 months. In general, our expectations for yields are for some minor fluctuations over the first two quarters of the year, followed by downwards pressure with rental prices cooling off as several projects, particularly apartments, finish construction and handover, increasing the available supply.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |