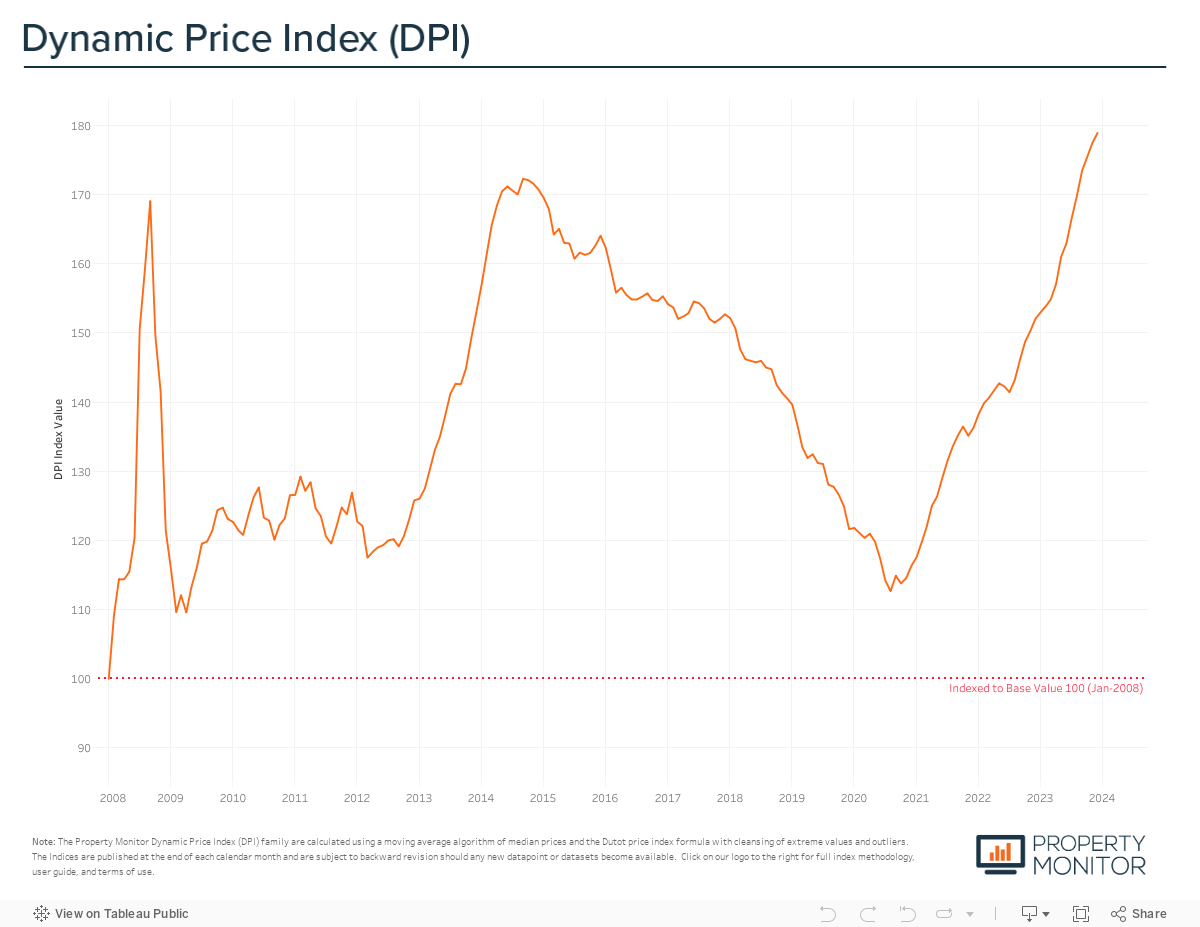

Average Dubai property prices increased an additional 0.8% in December to end the year up 16.4%—the largest annual increase in over a decade. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently stand at AED 1,281 per square foot, a little shy of 4% above the previous all-time high and market peak of September 2014.

In the 38-month period since bottoming out in October 2020, prices have gone on to increase 45.7%, averaging 1.37% per month in 2023, 0.90% in 2022, and 1.33% per month in 2021. The recent year-on-year uplift in the rate of price appreciation has largely been driven by the significant and sustained volume of new project launches—which for the majority of the year were skewed towards properties priced in the luxury to ultraluxury price tiers. Price growth for completed properties remains positive, however relatively subdued contrasted to price per square foot rates of new projects within the same communities.

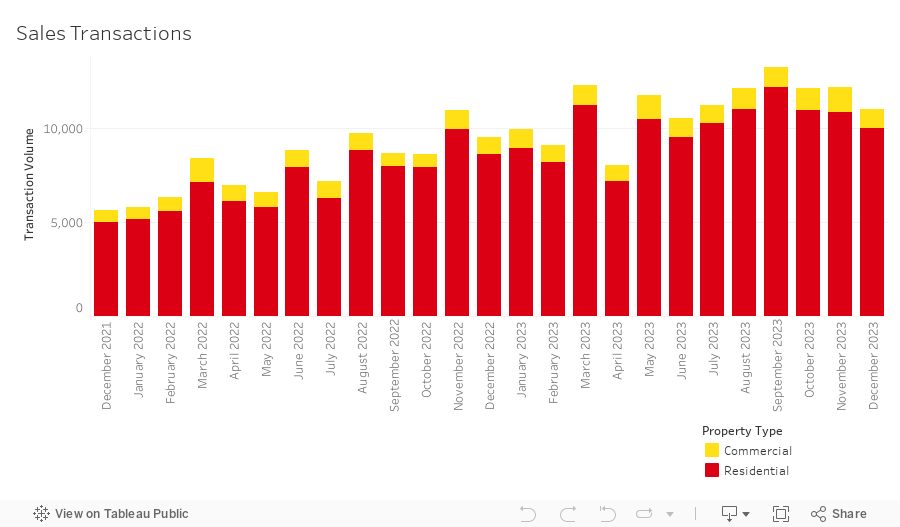

In December, the total volume of sales transactions decreased 9.9% month-on-month, falling to a total of 11,016 sales, yet still recorded as the highest volume ever for the month of December. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 91% (10,026 transactions).

The highest transacted commercial property types were hotel apartments (2.9%), and office spaces (2.6%), and land sales (2.3%). A total of 133,673 sales transactions were registered in 2023 (90.5% of which were residential), a 38.4% increase over last year and eclipses the long-standing record set in 2009 by more than 35,000 sales.

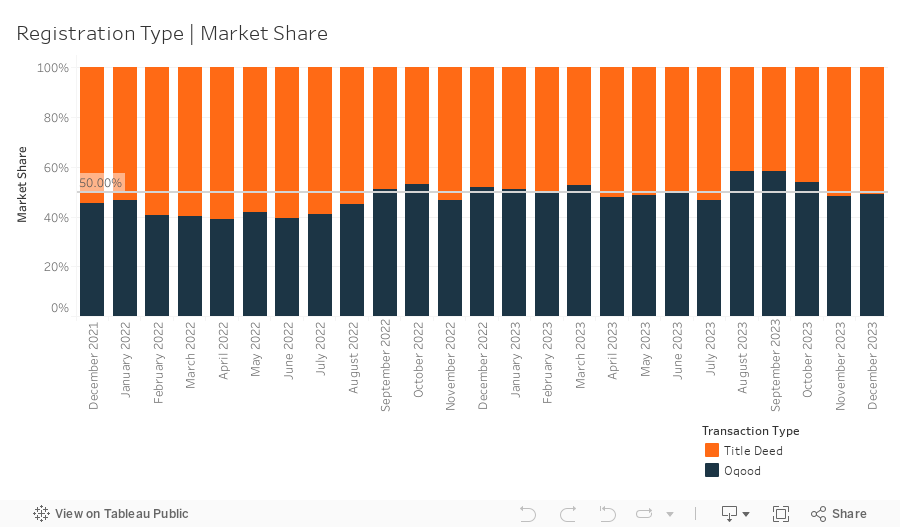

A total of 5,396 off-plan Oqood transactions were registered in December, marking an 8.3% month-on-month decrease in volume. However, there was a 0.8% increase in market share. Meanwhile, Title Deed sale volumes also witnessed a decrease falling by 11.3% and now account for 51.0% of all sales transactions. Although the market may appear to be slightly tilted in favour of completed properties over off-plan, a correctional adjustment by the Property Monitor team for registration technicalities within the Dubai Land Department (DLD), reveals that several villa and townhouse sales, presented as completed with issued Title Deeds, are indeed under construction and sold off-plan. In reality, off-plan transactions have held a dominant market share since Q4 2021, currently standing at 55.5%.

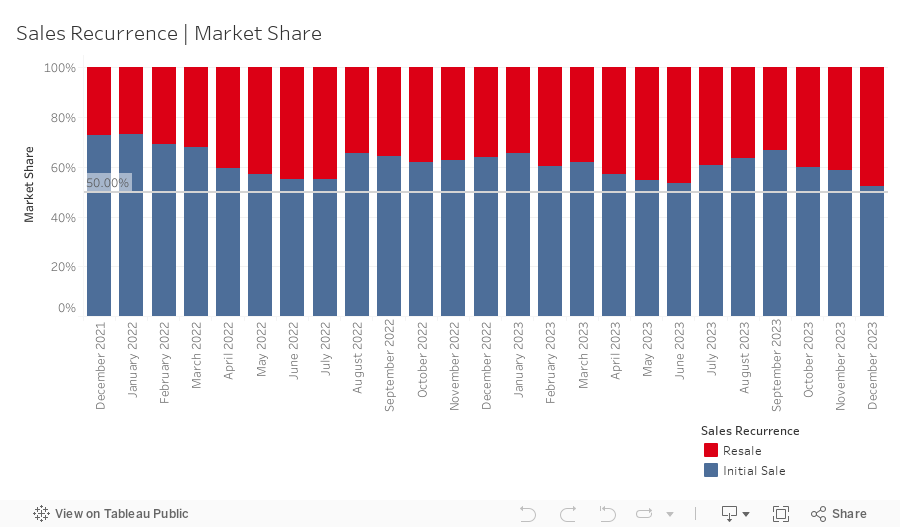

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an offplan or completed project—stood at 4,604 in December representing a market share of 41.6%, increasing marginally by 0.3% month-on-month and further regaining market share after falling to two-year lows back in September.

Mortgage transaction volumes decreased by 11.2% in December with a total of 2,589 loans recorded. While monthly volumes decreased, annual volumes reached new heights with just over 35,000 loans issued year-to-date, a 27.5% increase over all-time historic annual levels. Bulk mortgage loans mortgages—those taken by developers and larger investors with multiple units—were a significant attributor to this increase, seeing their market share grow by 5.5% to 19.0%.

The 491 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations in Rukan Tower 3 (51) in Rukan, South Residence 1 (42) in Dubai South, and Creek Views I (19) in Dubai Healthcare City II. Meanwhile, loans for refinancing and equity release saw their market share increase by 1.2% to 36.3%. The remaining 44.7% (down 6.7% from last month) of loans taken were new purchase money mortgages, with the average amount borrowed being AED 1.79m at a loan-to-value ratio of 75.4%.

Average gross rental yields for residential properties in the Emirate experienced their largest increase since December 2022, increasing by 0.11% to 6.79%; a small gain and only marginally above the 2023 average of 6.68%. Yields for both apartments and townhouses saw modest increases up 0.14% to 7.38% and 0.22% to 6.32% respectively, whilst yields for villas experienced a decrease, down 0.05% to 4.57%. The marginal shifts in yields and general plateauing align with our forecasts, and with numerous new development projects edging towards completion, the rental market is poised to see an increase in available inventory in the coming months and, with that, we should also see a gradual decrease in rents throughout 2024.

December 2023 brings what has been nothing short of a phenomenal year to a close for the Dubai real estate market. A year which saw new records set across several key market metrics, with some only to be broken again and again as the months went on. While many major markets across the globe continued to struggle or slowly began to recover, Dubai forged a path forward all of its own.

Forward-looking into 2024, we anticipate that the bull-run of the Dubai real estate market will continue well into the year, however, it is unlikely that we will see a record-breaking fashion comparable to that of this year, and there are headwinds on the horizon. Price appreciation of completed properties is already displaying signs of slow down and plateau, particularly for villas and townhouses, and new project launches are beginning to show greater diversity in offerings with notable growth towards the mid-market price tiers. Ending the year with single digit price growth is a likely outcome.

With over 150 projects in the planning and pre-launch phases being tracked by the Property Monitor team, the breakneck pace of new project launches is set to continue for at least the first two quarters of the year, and with it an increase of new and smaller developers bringing projects to market. On the back of close to 100,000 new residential units launched in 2023, these upcoming launches will continue to add to the robust pipeline of supply that will be handing over in the years ahead, with 40,000+ units on the horizon for this year, and increasing volumes over the next 3 to 5 years. As projects complete and units become available for occupancy, the supply-demand relationship will gradually move back in favour of buyers and tenants, putting downwards pressure on pricing.

As both occupiable and future supply increases, population growth will be one of the key measures to watch. Dubai experienced slightly less than 3% annual growth in population over 2023, with a relatively stable monthly growth trend of 0.25%. To absorb upcoming supply this year and in the coming years, this rate needs to increase to avoid oversupply issues and progression into the downwards phases of the market cycle.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |