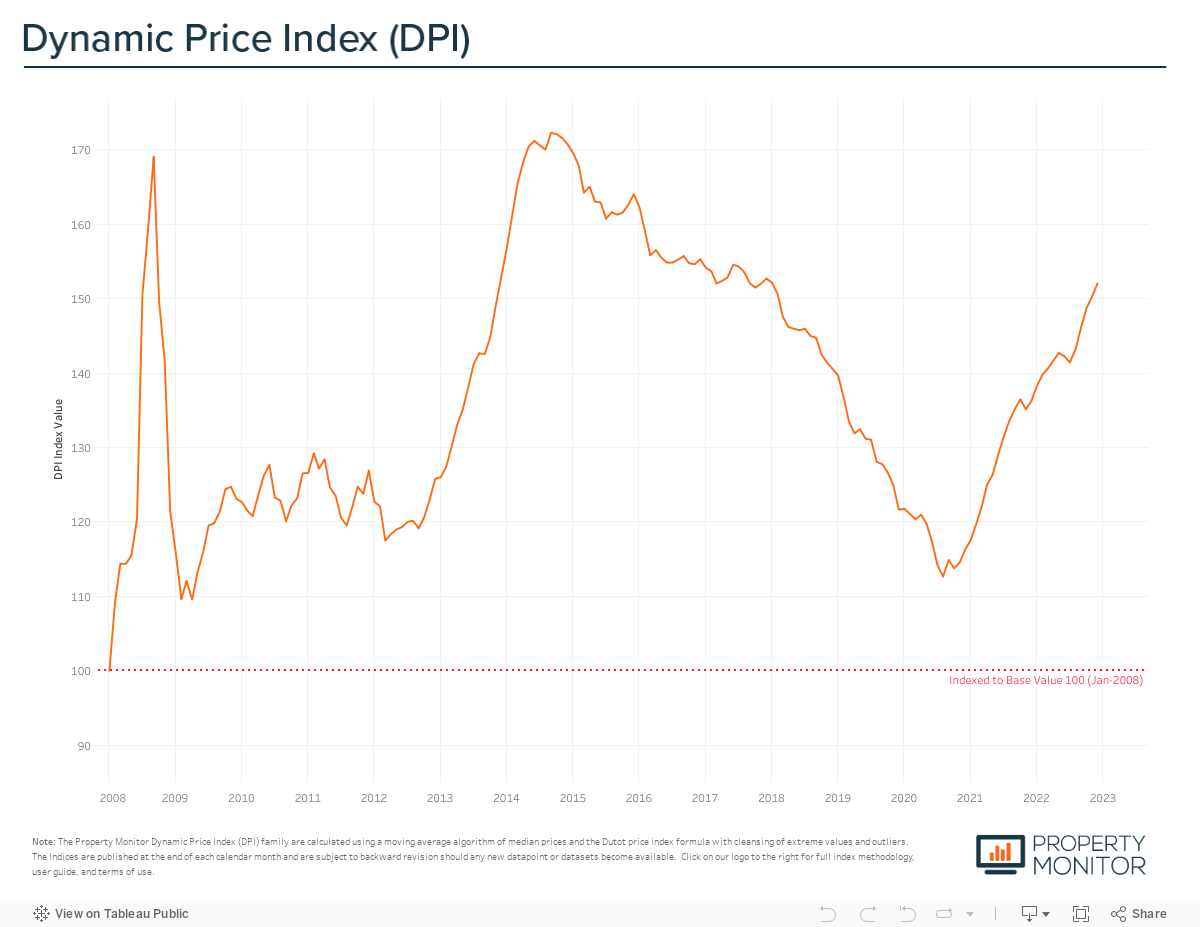

Ending on a high, what has been an incredibly strong year for the Dubai real estate market, property price growth continued by recording a 1.17% increase in December. Dubai property values now stand at AED 1,089 per sq ft according to the Property Monitor Dynamic Price Index (DPI), now back to a level not seen since December 2013 during the last market upswing and in January 2018 on the long pre-COVID downcycle.

Overall property price growth reached 11.05% in 2022, averaging 0.92% per month—down from 1.33% per month in 2021 when annual price growth was just shy of 16%, but still a very strong yearly performance. As previously reported, the diminishing monthly rate of price appreciation can be viewed as a positive sign, one that points to a market that is trending towards sustainable price growth that can help continue to carry the market upwards well into 2023.

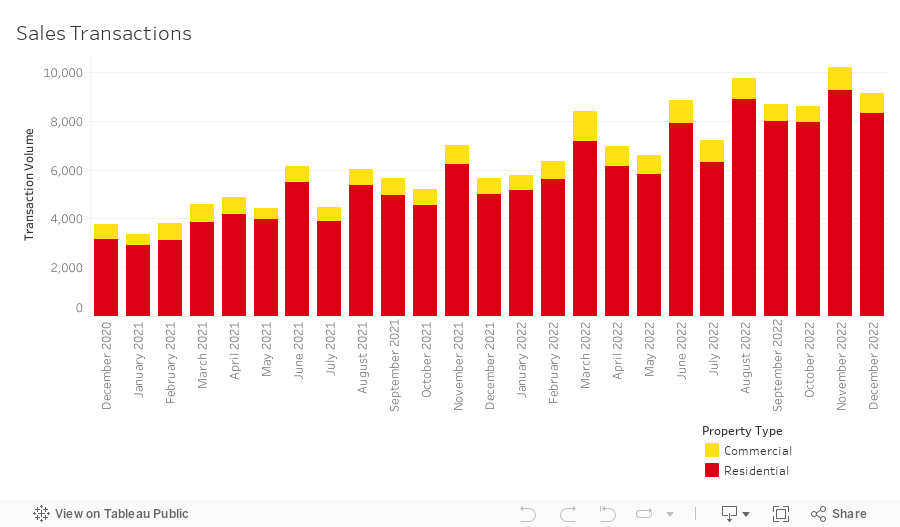

After surpassing 10,000 transactions last month, the total volume of sales transactions declined 10.4% in December registering a total of 9,131 sales. However, transactions for the month still reached a level that marks the strongest December on record and almost double that of every December since 2014. Residential transactions—those for apartments, townhouses, and villas—accounted for 91.1% (8,321 sales transactions) of the total, with hotel apartments (3.3%), office (2.1%), and land sales (1.9%) being the highest transacted commercial property types.

A total of 96,557 sales transactions were registered in 2022 (89.6% of which were residential), a 157.5% increase over last year and just 1,400 sales short of claiming the highest year ever witnessed in Dubai market history. While not reaching the all-time market record—which counts both residential and commercial transactions—sales performance in 2022 for the residential segment did indeed reach a new all-time high with 86,849 sales displacing the long-standing record of 80,831 sales set in 2009. Should the market be able to maintain the record-setting pace of 2022 we could see in excess of 110,000 transactions next year. Property Monitor analysis, however, predicts that this is unlikely and that some steam and investor froth will inevitably come off the market and transaction volumes should moderate throughout the year ahead.

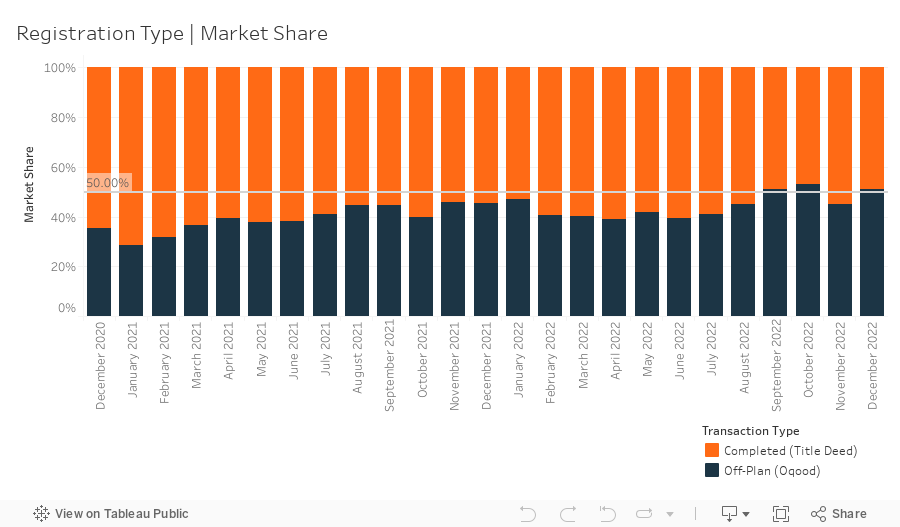

A total of 4,654 off-plan Oqood transactions were registered in December, increasing by 1.1% month-on-month and by an even more hearty 80.7% on a yearly basis. Oqood transactions now account for 51% of the market, while Title Deed sale volumes fell to 49% after witnessing a considerable decrease for the month, shrinking by 19.9%. While first impressions may point to a market that is spilt relatively evenly between off-plan and completed properties, after we adjust for registration technicalities with the Dubai Land Department (DLD)—where several villa and townhouse sales are presented as being completed and with Title Deeds issued, when they in fact under construction having been sold off-plan—the accurate breakdown of market share is 59.8% in favour of off-plan. This key market insight, exclusively provided by Property Monitor experts, is important to track and assists in understanding the changing market dynamics.

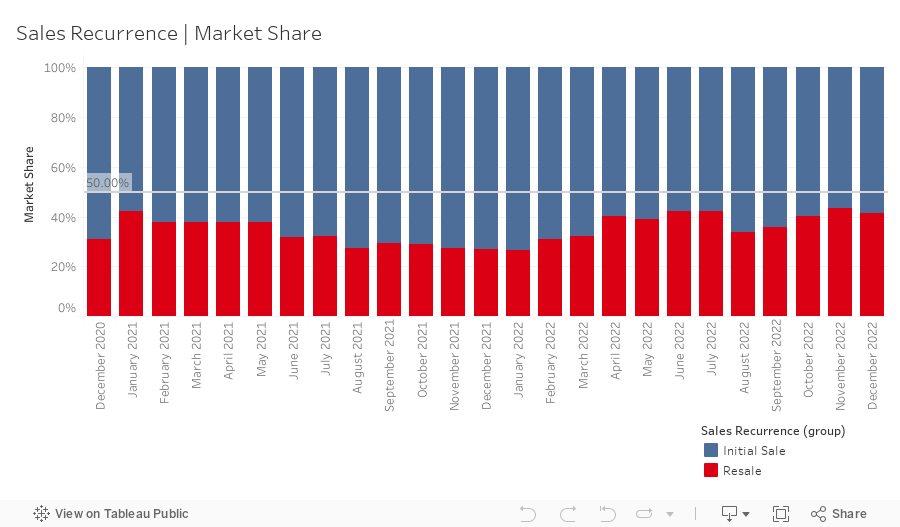

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 3,772 in December representing a market share of 41.3%, falling 2.1% month-on-month. A growing portion (19.7%) of this resale activity can be attributed to secondary sales of off-plan properties where the initial buyers, in most cases, are capitalising on the current market upswing and cashing out with a premium in hand. Should this number continue to grow, and more importantly become further driven by speculative purchasing, the market runs the risk of inflating to where a bubble bursting scenario could unfold. We will be watching this carefully.

New off-plan development project launches once again reached a record monthly high in December adding just over 9,500 units to the market for sale at an anticipated combined gross sales value of ~AED 23.3 billion. Apartments represent 81.7% by volume of this new inventory while townhouses and villas represent 14.5% and 3.8% respectively. Year-to-date new project launches have exceeded just over 53,000 units and AED 155 billion in aggregate sales value.

Mortgage transaction volumes declined slightly in December (down just over 1%), registering 2,293 loans for the month (with a total value of ~AED 17.7 billion), this remains unexpectedly high given the current interest rate environment and ever-increasing borrowing costs. A deeper investigation into these headline transaction numbers reveals that bulk mortgage registrations—those taken by developers and larger investors with multiple units—comprised 36.6% of loans, increasing market share by 13% from last month helping to maintain high monthly volumes. These bulk registrations were spread across several projects, most notably J One Tower 2 in Business Bay where 116 loans transactions were recorded under a combination mortgage transfer and delayed mortgage portfolio registration for a total of AED 9.08b. Additional analysis into these transactions reveals that actual loan volume was for only 96 units in a portfolio mortgage with a value of AED 350m and due to intricacies in the way DLD records various mortgage data the total value of the portfolio was inadvertently inflated.

Breaking down the mortgage market further, shows that a further 32.1% of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.76m at a loan-to-value ratio of 77.4%, while the remaining 31.3% of loans (down 7.4% from last month) were for refinancing or equity releases.

In December, Emirate-wide average gross rental yields stand at 6.64%, up by 0.11% month-on-month, with yields for all three residential property types increasing: townhouses up by 0.24% to 6.30%, apartments up by 0.11% to 7.01%, and villas up by 0.05 to 5.19%. In the months ahead we predict that yields for residential properties will experience small-to-moderate growth and likely face downwards pressure with rental prices cooling off as several projects finish construction and handover in the early part of the new year.

A retrospective view of 2022 paints a picture of a robust Dubai real estate market, one that has outperformed many expectations and continued to flourish at time when comparable global markets have been inescapably entangled in the thralls of inflation, energy prices, and rising interest rates that have ultimately led many into a downturn. It is perhaps that Dubai cannot be truly compared, on a like-for-like basis, with any other global market owing to its unique position, whereby it has become an oasis, not just in the desert but the world real estate sector. A particular feature of the current demand curve is the stream of interest from across the globe which seems to be fueled by a near endless number of taps, from the impact of the Arab Spring on the previous market cycle, to COVID-19, to the Ukraine-Russian conflict, and most recently the removal of restrictions in China and the reopening for travel abroad. Dubai and the UAE have strategically positioned themselves over the years to be a destination for all and as a result seem to be the net beneficiary of the events outside of its own borders.

Property prices in Dubai are up 29.3% since bottoming out in November 2020 yet they remain just over 8% below the peak of the last market cycle which topped out in September 2014. Typically, but not always, each market cycle sees prices power on to rise higher than the peak of the previous cycle. While the biggest gains are probably behind us with a strong prospect of price stability lying ahead, we predict that the Dubai market will continue to gently appreciate this year. However, as previously reported and being a spoiler alert, the current market boom can’t run indefinitely. Developers, investors, and consumers should keep this in mind and assess their unique situations and goals carefully.

Forward looking to 2023 we anticipate that the diverging tale of two markets will continue, with off-plan maintaining dominant market share for the foreseeable future with project launches to continue in full steam ahead mode so long as absorption can be sustained, while the ready property market will largely plateau across the majority of property types and prices points. Headwinds and downside side risks look firmly concentrated around affordability, availability, inflation, and mortgage interest rates.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |