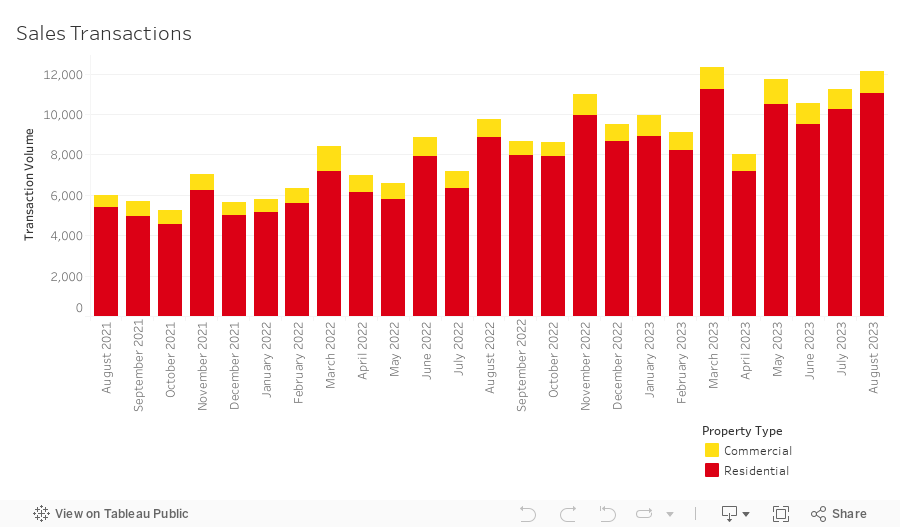

The typical seasonality of the Dubai market—which historically sees temperatures rise and real estate activity cool in the Summer—was well and truly amiss this year, with the period experiencing continued high price growth and record sales transaction volumes.

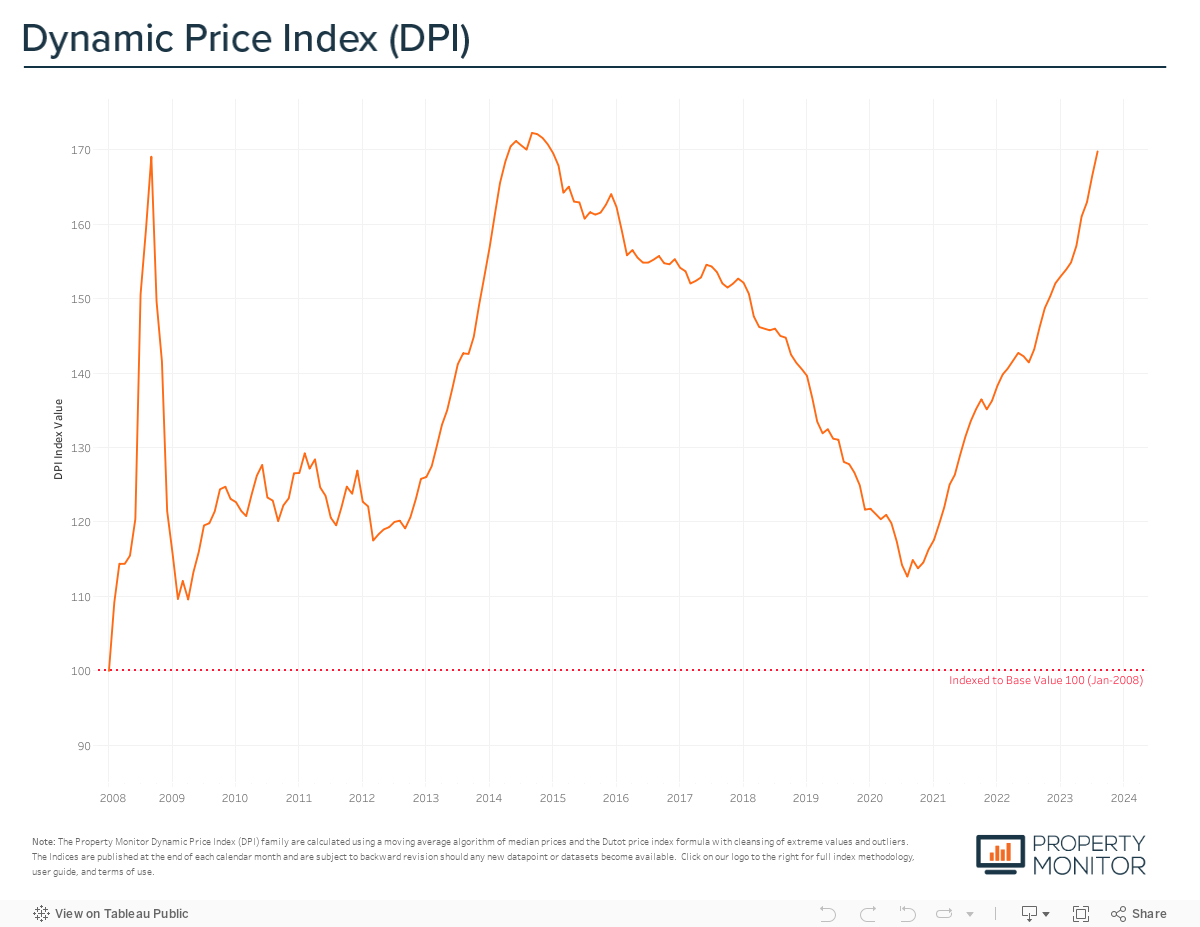

According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices grew by just under 2% in August and currently stand at AED 1,216 per square foot. Prices are now just a mere 1.4% lower than the peak of the previous market cycle (and the all-time high) of AED 1,234 per square foot.

The total volume of sales transactions increased 8.1% month-on-month, reaching a total of 12,134 sales and marks the highest volume ever for the month of August. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority at 91.1% (11,053 sales transactions). The highest transacted commercial property types were hotel apartments (4.1%), office spaces (2.1%), and land sales (1.9%).

Year-to-date there have been 85,060 sales transactions recorded, a 41.9% increase over the same period last year and a 125.4% increase of that for 2021. Average monthly transaction volumes for 2023 are far exceeding any previously recorded figures, setting the market on track to outperform the highest ever annual sales record established in 2009. We anticipate that we’ll see over 120,000 sales registered by the end of the year and that the record set in 2009 will be broken as early as next month, leaving a full quarter ahead of us.

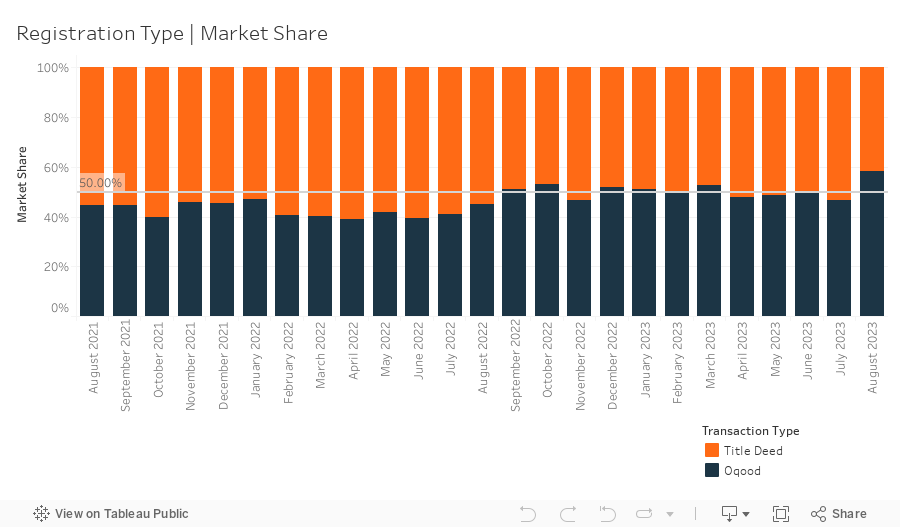

New development project launches, and the sale of off-plan properties have been significant drivers for the amplitude of transaction activity this year. In August, a total of 7,085 off-plan Oqood transactions were registered, increasing by a remarkable 35% month-on-month and 60.6% on a yearly basis. Oqood transactions now account for 58.4% of the market, while Title Deed sale volumes fell to 41.6%. Market share is now clearly in favor off-plan properties over completed, and after a correctional adjustment by the Property Monitor team for registration technicalities within the Dubai Land Department (DLD)—relating to how several villa and townhouse sales are recorded with Title Deeds, when they are indeed under construction and sold off-plan—this lead is further pronounced and in reality, off-plan transactions currently represent 64.7% of the market. Off-plan sales last held a dominant market share of this level only briefly in April 2020 when the COVID-19 pandemic limited the ability to transact completed properties due to mobility restrictions and the temporary closure of Trustee offices.

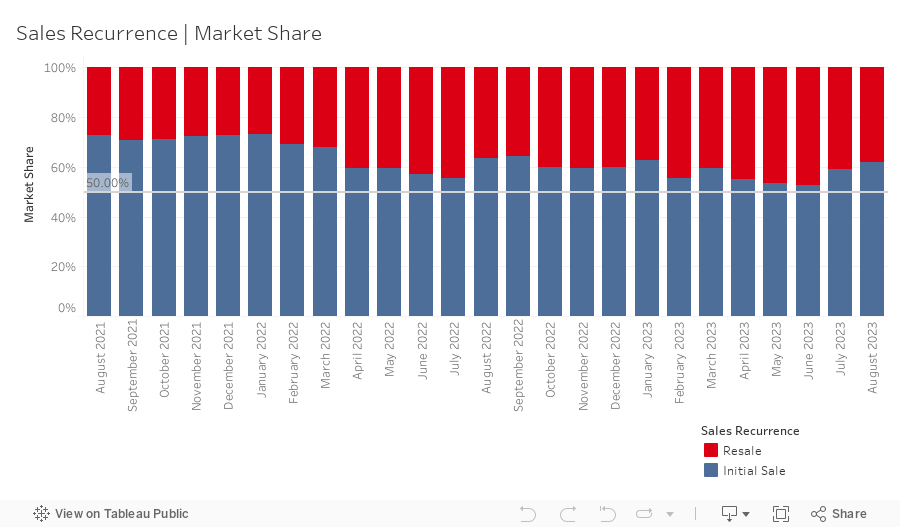

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 4,620 in August representing a market share of 38.1%, decreasing by 2.6% month-on-month. While overall resale activity decreased, the portion of off-plan resales increased marginally—up 1.3% in July—rising to 21.8%. Speculative activity is slowly making up a greater portion of off-plan resales, however most of these resales remain skewed towards properties that are within a year of anticipated completion. The restraint currently being witnessed in the market will likely not last, and inevitably a growing number of investors will roll the dice on what may seem like easy short-term gains, however this strategy should always be assessed with a high degree of caution and understanding of the risks involved. Bull markets do not run forever and flipping off-plan can be a dangerous game of hot potato.

Mortgage transaction volumes decreased by 7.8% in August with a total of 2,951 loans recorded. Bulk mortgage loans mortgages—those taken by developers and larger investors with multiple units—were a significant attributor to this decline, seeing their market share drop by 14.7% to 20.8%. The 613 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Sol Avenue in Business Bay (323), Rokane G24 in International City (77), and Micasa Avenue (62) in Al Furjan. Meanwhile, loans for refinancing and equity release saw their market share grow by 7.2% to 36.2%. The remaining 43% (up 7.5% from last month) of loans taken were new purchase money mortgages with the average amount borrowed being AED 1.73m at a loan-to-value ratio of 76.3%. Loans for new purchases and refinancing remain at historically high levels across all residential property types, this indicates continued strength in the overall mortgage market despite relatively high interest rates. While interest rate hikes have been paused, it remains unclear if further rate hikes are potentially on the horizon. For now, it appears that monetary policy measures implemented in the US have achieved some of their desired impact, inflation is tapering down and the days of aggressive rate increases are behind us, however, we anticipate that rate reductions will not transpire in the near future, likely at the earliest mid-2024.

Average gross rental yields for residential properties in the Emirate continued to remain relatively stable in August, increasing by just 0.1% to 6.74%. Yields for all three residential property types saw modest increases with apartments up 0.1% to 7.16%, townhouses up 0.35% to 6.42%, and villas up 0.09% to 4.97%. The marginal shifts in yields and general plateauing align with our forecasts, largely due to several communities seemingly hitting the peak in attainable rental rates, and sales prices levelling off at the same time in certain areas. With several new development project edging towards completion the rental market is poised to see an increase in available inventory towards the end of the year and with that a likely cessation in rampant rental price increases followed by a gradual decrease in rents going into 2024.

With four months remaining in the year and given the seemingly insatiable demand for off-plan projects, it is near certainty that we will see several new records set in the Dubai real estate market, however it’s tough to call which record will be the first to fall. Emirate-wide average property prices are less than 1.5% away from the historical peak of September 2014 and if price appreciation tracks with the current trend a new high will be reached either next month or the following. YTD sales transaction volume has already surpassed the YTD equivalent of any year before and now sits just 13,000 sales away from entering full-year record territory. With over 55,000 new units entering the market for sale through new off-plan project launches already in 2023, coupled with a consistent undersupply of suitably priced ready properties available, the market share for off-plan is also well positioned to continue its dominance and break records. And finally, the crown for the most expensive residential property sale could be claimed at any moment with several properties currently on the market at asking prices well above the current record holder of AED 600m. Which will be first? Will all have new records set? Or will the market take a turn and start to cool off?

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |