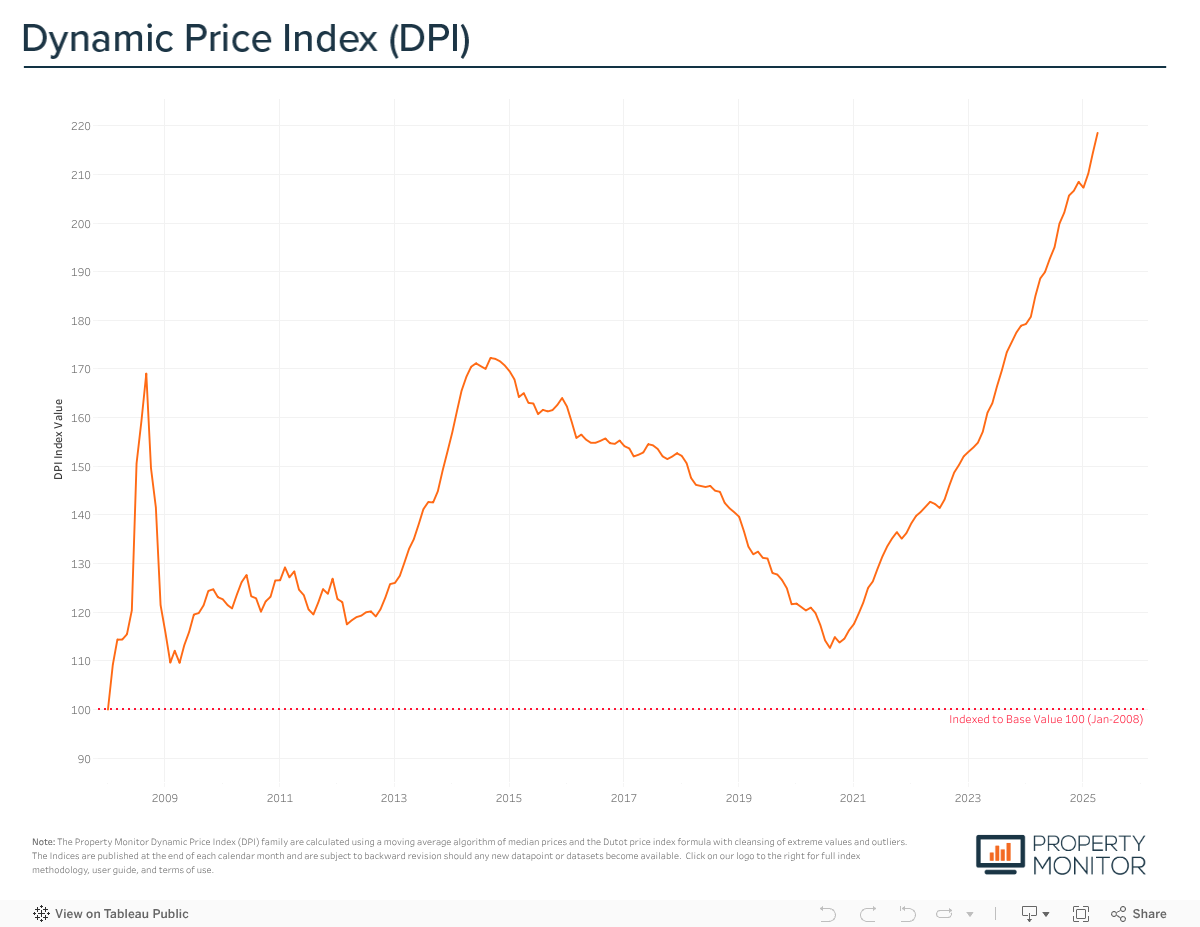

Continuing the trend of higher-than-average monthly price growth, Dubai’s property prices experienced yet another strong increase, recording a gain of 1.97% in April. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently average AED 1,565 per square foot, standing 26.9% above the previous market peak in September 2014.

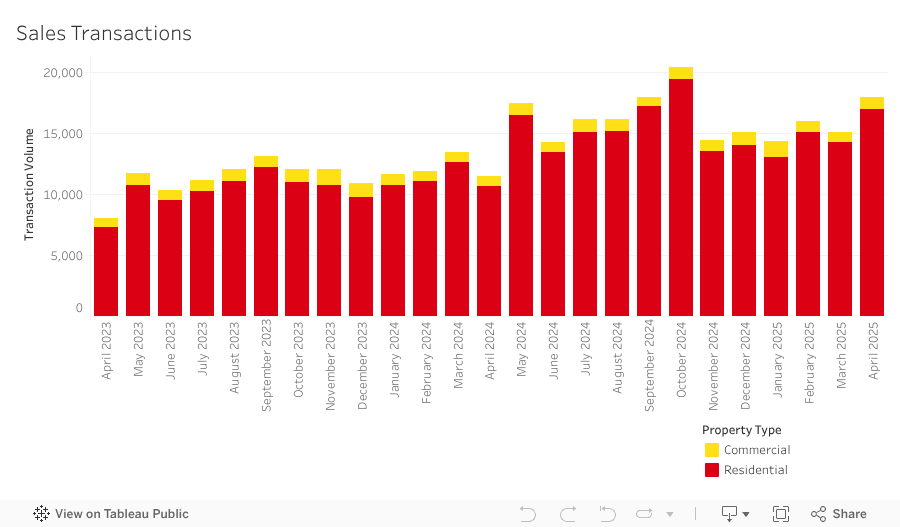

A total of 18,010 sale transactions were recorded in April, reflecting an 18.3% increase from the previous month and a 55.1% surge year-on-year. This marks a new record high for the month of April, exceeding the previous peak set in 2009 by nearly 28%. However, it’s worth noting that April 2024’s transaction volume was significantly dampened by severe rains and flooding, which curtailed market activity for a substantial part of the month. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 94.3% (16,976 transactions). The highest transacted commercial property types were vacant land (2.4%), office spaces (1.7%), and hotel apartments (1.0%).

Year-to-date sales transaction volumes have now surpassed 63,000 and are over 30% higher compared to the same period 2024. At the current pace of transaction velocity, we are on track to see year-end sales volumes reach ~195,000 and set a new all-time high.

In April, 10,277 off-plan Oqood transactions were recorded, an increase of 14.1% from the previous month, brining market share to 57.1%, down 2.1% month-on-month. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions represent an even larger market share of 70.5%. Meanwhile, Title Deed sale volumes also witnessed an increase, rising by 24.8% and now accounting for 42.9% of all sales transactions.

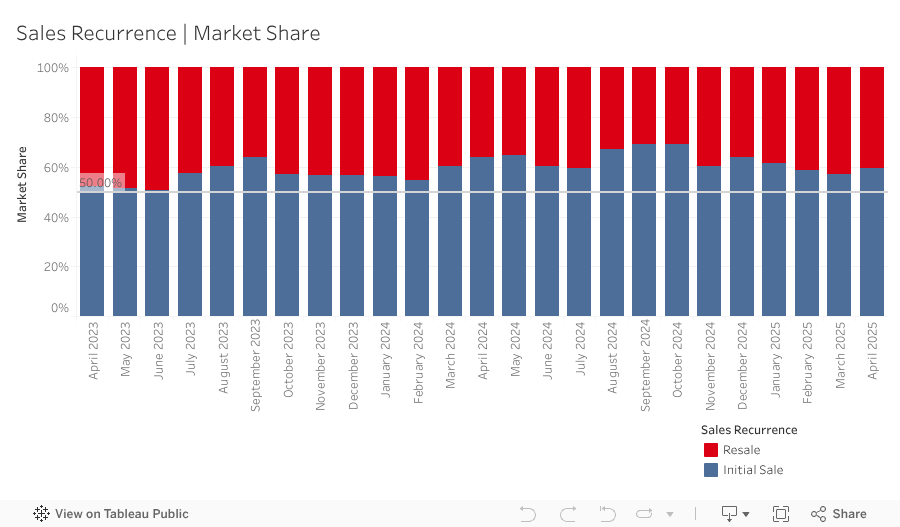

Meanwhile, resale transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 7,062 in April, accounting for 39.2% of the market. This marks a 3.6% decrease month-on-month. While overall resale activity decreased, the portion of off-plan resales continued to rise, reaching 33.5% and bringing the 12-month rolling average to 26.2%.

New off-plan project launches remain near record levels, with just over 10,500 units introduced to the market in April, carrying an estimated combined gross sales value of approximately AED 32.8 billion. Apartments account for 81.1% of this new supply, while townhouses and villas represent 9.8% and 9.1%, respectively. Year-to-date, nearly 49,000 units have been launched with a total sales value approaching AED 166 billion. A notable trend emerging in 2024 is the sharp rise in villa launches—within the first four months alone, villa volumes have already reached 85% of the total recorded for all of last year. Given the ongoing shortage of single-family homes in both the off-plan and ready segments, the absorption of this new supply is expected to be exceptionally strong.

Mortgage transaction volumes increased by a remarkable 30.3% in April with a total of 4,473 loans recorded. During the month, loans taken for new purchase money mortgages accounted for 48.0% (down 8.9% from last month) of borrowing activity, with the average amount borrowed being AED 1.81M at a loan-to-value ratio of 75.1%. Meanwhile, loans for refinancing and equity release saw their market share decrease by 4.1% to 32.2%. The remaining 19.8% (up by 13.0% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 884 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at AA Tower (169) Trade Center 1, Grand Heights (146) Jumeirah Village Circle, and Berlin Group 1 (97) in International City II, as well as portfolio mortgage registration pre-registrations at Avenue Residence 7 (43) in Al Furjan.

As Dubai’s property cycle enters its 54th month of expansion, the market continues to display remarkable resilience, though signs of maturity are becoming more apparent. The current cycle has been underpinned by diverse demand sources and broad-based investor confidence, but the pace of growth—particularly in prices and off-plan activity—warrants close attention. April’s 1.97% price appreciation remains within a manageable range, but any sustained acceleration beyond the 2% mark could signal a shift toward speculative momentum, especially in segments where pricing may be decoupling from end-user fundamentals.

The market’s capacity to absorb record volumes of off-plan launches—particularly in the villa segment—remains a key strength. However, with year-to-date launches nearing 50,000 units and off-plan resales on the rise, a more discerning investor base may soon begin prioritizing quality, location, and handover timelines over sheer novelty or price appreciation potential. Maintaining demand at current levels will increasingly depend on the strategic phasing of new inventory, effective differentiation, and realistic pricing aligned with evolving buyer expectations.

Looking ahead, sustained stability will require both demand- and supply-side discipline. Developers and policymakers must continue to balance growth with caution, ensuring that delivery pipelines are matched with genuine absorption capacity. Product diversity, transparent timelines, and affordability will be central to maintaining market confidence. With the global macroeconomic outlook still mixed and interest rates likely to remain elevated, Dubai’s ability to navigate this next phase thoughtfully will determine whether the current cycle extends further—or begins to plateau.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |