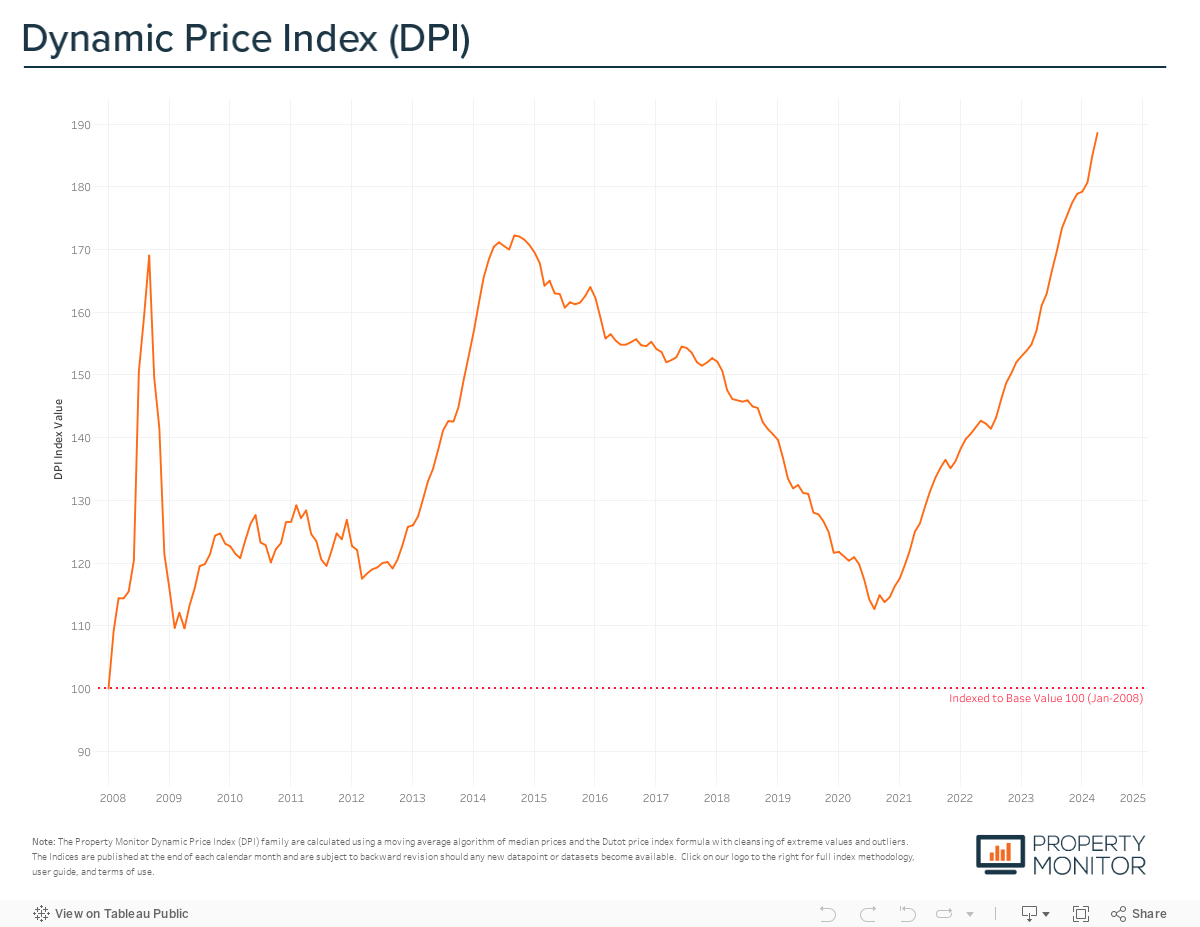

Following last month’s dramatic surge in price appreciation, Dubai’s property prices experienced another higher-than-average month of average price growth, recording a gain of 1.95% in April. According to the Property Monitor Dynamic Price Index (DPI), Dubai property prices currently stand at AED 1,351 per square foot, 9.5% over the previous all-time high and market peak of September 2014.

Delving further into the underlying data reveals that the recent uptick in price appreciation continues to be primarily driven by significant differences in trading prices between existing homes and newly developed off-plan properties. Among the 42 communities tracked by the index, 14 exhibited off-plan price premiums exceeding 20%, reaching levels as high as 80% and 70% in Dubai Sports City and International City respectively, where new apartment project launches differ drastically in quality and overall offering from some of the now ageing existing projects. Interestingly, at the bedroom level, the highest price per square foot premiums are predominantly observed in 1-bedroom units. These units also exhibit the largest disparity in average unit square footage, with new units being approximately 12.5% smaller than older ones. However, despite this reduction in size, sales prices only show a slight increase in comparison.

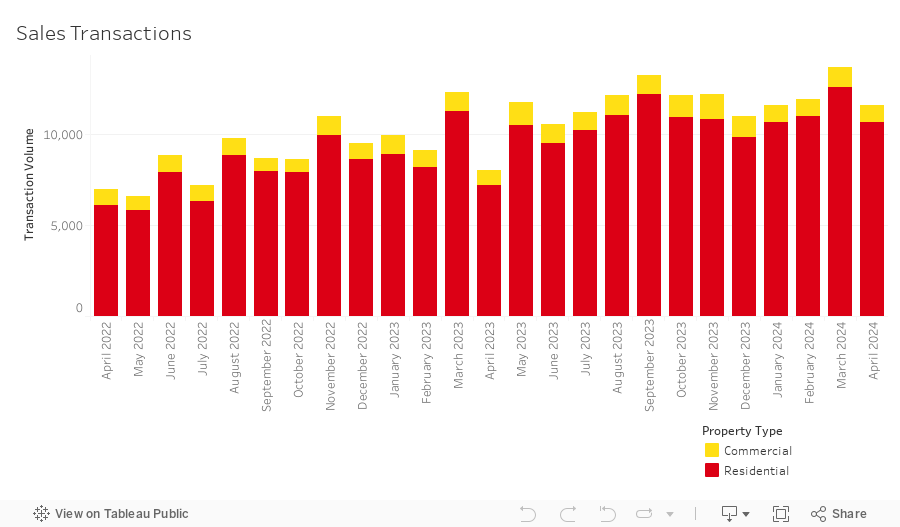

Sales transaction volumes fell by 15.1% in April to a total of 11,605 transactions. While at face value this may seem like a concerning dropoff in activity, month-on-month it still records as the second highest monthly sales volume ever recorded for the month of April as well as a 44.3% year-on-year increase. Given that the fundamental ability to transact was reduced by a weeklong public holiday break for Eid al-Fitr and several more days resulting from unprecedented storms which saw double the annual rainfall in a period of just 24hrs, on a pro-rata basis daily transaction volume was actually close to all-time highs. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 91.8% (10,659 transactions). The highest transacted commercial property types were hotel apartments (3.8%), office spaces (1.8%), and land sales (1.5%).

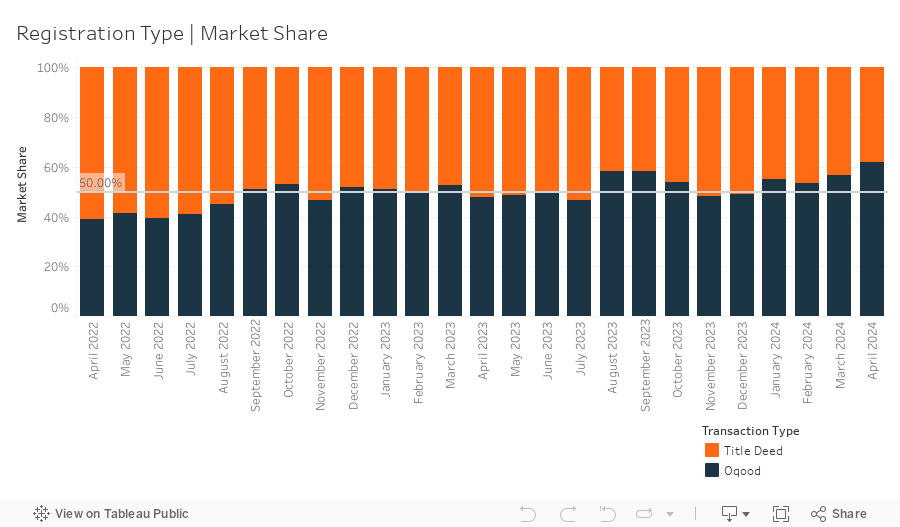

In April, 7,204 off-plan Oqood transactions were recorded, a marked decrease of 7.3% from the previous month yet a 5.2% uptick in market share to 62.1%. Meanwhile, Title Deed sale volumes also witnessed a decline, falling by 25.4% and now accounting for 37.9% of all sales transactions. The sharp drop-off in Title Deed sales can largely be attributed to the previously mentioned reduction in the ability to transact, during this period trustee offices and the means to transfer ready properties was temporarily halted, however developers were still able to manage self-registration of Oqood sales. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties— instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions secure an even larger market share of 67.4%.

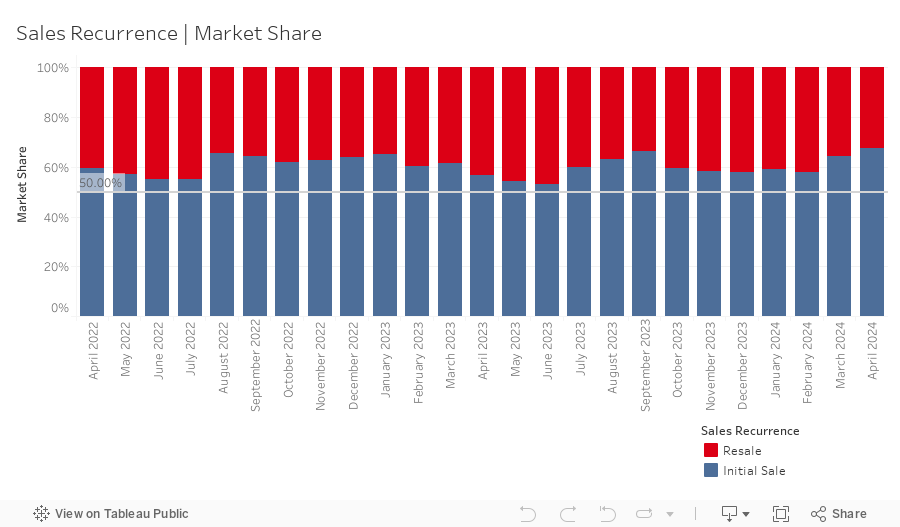

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 3,764 in April representing a market share of 32.4%, decreasing by 2.8% month-on-month, and propelling the market share of initial developer sales to 67.6%.

Initial figures for new off-plan project launches in April reveal the introduction of close to another 10,000 units to the market for sale during the month, adding to an already record total of ~34,000 units spread across 120 projects in Q1 2024. This remarkable level of activity within the off-plan market shows no signs of slowing down and is expected to persist for the foreseeable future, both in the newly announced master communities which will see the likes of master developers Aldar, DAMAC, Emaar, and Majid Al Futtaim bring their own projects to market, as well as specialist and smaller developers launch across several established communities. Expect to see a growing number of new developments in Meydan Horizon, Jumeriah Garden City, Jaddaf, Motor City, and Majan — a wide ranging geographic selection that will provide a variety of opportunities for investors and end-users alike.

Mortgage transaction volumes decreased by 23.8% in April with a total of 2,128 loans recorded. Loans taken for new purchase money mortgages accounted for 55.8% (up an additional 2.5% from last month) of borrowing activity, with the average amount borrowed being AED 1.82m at a loan-to-value ratio of 76.0%. Meanwhile, loans for refinancing and equity release saw their market share increase by 2.1% to 38.5%. The remaining 5.7% (down by 4.6% from last month) was due to bulk mortgages — those taken by developers and larger investors with multiple units. The 120 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at B2B Tower (12) in Business Bay and Mazaya Business Avenue (10) in Jumeriah Lakes Towers as well as portfolio mortgage modifications at Safeer Tower (13), in Business Bay. Even though the US Federal Reserve’s FOMC kept the target rate range unchanged, as did the UAE’s local interbank and mortgage rates, lending activity remains robust. The policy of “higher for longer” is expected to have minimal impact on borrowing activity in Dubai, particularly with new purchase loans.

Looking ahead to the coming months, we anticipate that the divergence between two market segments will persist. From one side, the ready property market largely continuing to plateau across the majority of property types and price points, save for the exception of the renovation effect in the single-family homes segment. This is particularly evident within the villa segment, where a number of properties were snapped up as the market began to recover and have since undergone complete renovations. Said properties have now been transformed from their original design aesthetic to modern homes with a price point to match.

On the other side, the off-plan property market is poised to maintain its dominant position for the foreseeable future, with project launches proceeding at a vigorous pace. Although recent off-plan launches have seen strong demand, ongoing monitoring of absorption rates is imperative. A slowdown in absorption could signal a potential oversupply issue, which may lead to a market slowdown.

Although we hold an optimistic outlook for the year ahead and foresee sustained growth, it’s crucial for decision-makers across developers, investors, and occupiers to remain mindful of the lessons learned from previous market fluctuations.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |