Momentum in Dubai’s residential real estate market carried through October, though with noticeably softer monthly gains. Prices edged up by just 0.13%, easing back from the more pronounced increases seen in September and August. Even with this slower pace, the market continues to climb steadily. The Property Monitor Dynamic Price Index (DPI) places average prices at AED 1,683 per square foot—more than double their level at the October 2020 low point and comfortably above the previous market high set in 2014. The market’s long-term upward trend remains intact, even as monthly movements become more tempered.

A total of 19,760 sales transactions were recorded in October, a decline of 2.7% month-on-month and 4.9% year-on-year—the first annual decrease seen this year. Although October was also the first calendar month of 2025 not to set a new all-time high, activity remained near historic levels. It stands as the second-strongest October ever, surpassed only by October 2024, which still holds the highest monthly total in Dubai’s transaction history. The slight year-on-year decline therefore reflects the exceptionally elevated baseline set last year and may simply be a function of comparison rather than an indication of shifting market dynamics. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 93.5% (18,466 transactions). Commercial activity was led by office spaces (2.5%), followed by vacant land (1.3%) and retail units (0.9%).

Year-to-date transaction volumes have reached nearly 178,000, representing a 17.4% increase compared with the same period in 2024 and already surpassing 98% of last year’s full-year total. Monthly activity has remained consistently strong, averaging around 17,300 transactions over the past year, with only two months falling below the 15,000 mark. Should this momentum continue through December, total sales are projected to exceed 212,000—setting a new all-time annual record and extending Dubai’s record-breaking run into its third consecutive year.

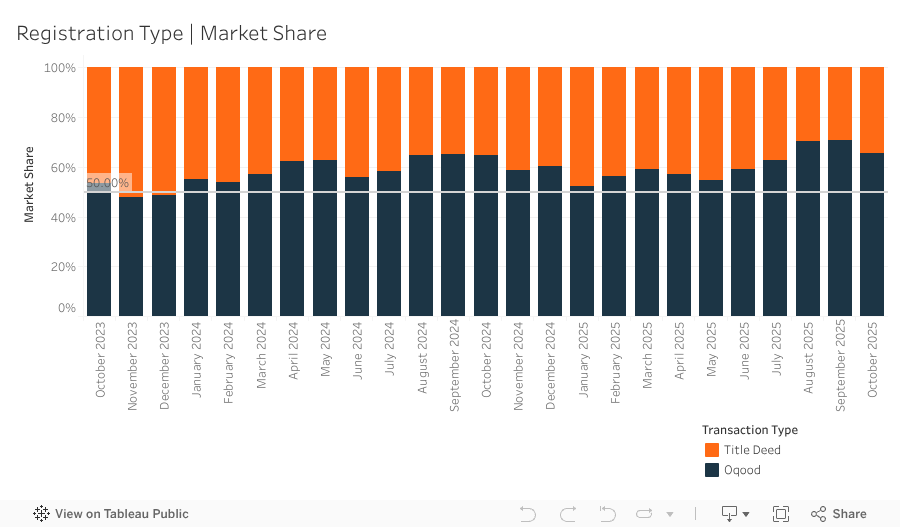

In October, 12,947 off-plan (Oqood) transactions were recorded, reflecting a 9.9% decline from the previous month. This pullback also reduced the off-plan market’s share of total sales to 65.5%, down 5.2% month-on-month. While Oqood registrations typically track off-plan activity, a portion of villa and townhouse sales are registered by the Dubai Land Department as Title Deed transactions—classified as completed properties despite effectively being off-plan. After adjusting for this technical classification gap, the true off-plan share rises to approximately 70.6%. Conversely, Title Deed transactions rose sharply in October—up 14.7% month-on-month—with their market share increasing to 34.5%. This lift was driven primarily by a surge in apartment sales within the completed market, which expanded the Title Deed segment as off-plan volumes settled from prior highs.

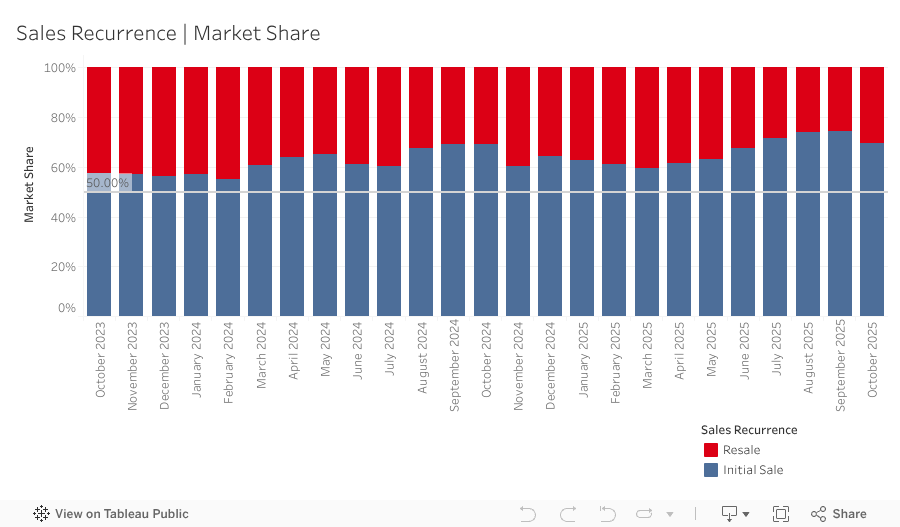

Meanwhile, resale transactions—defined as any subsequent sale of a property after its initial sale by the developer, whether that first sale was off-plan or completed—totaled 5,956 in October, up 4.6% month-on-month and representing 30.1% of the market. Off-plan resales edged higher as well, accounting for 21.7% of all resale activity, though the 12-month rolling average continued its downward trajectory, easing to 25.1%. After peaking above 33% in April, off-plan resales remain significantly below their earlier highs, even as initial developer sales continue to demonstrate sustained strength.

Dubai’s new project pipeline remained exceptionally strong in October, with 65 launches introducing more than 14,000 residential units valued at an estimated AED 33.5 billion. Year-to-date, 532 projects have been launched, bringing nearly 131,504 units to market—levels that far exceed what would traditionally constitute an entire year of activity. A total of 228 developers have launched projects so far in 2025, up from 163 during the same period in 2024, underscoring the expanding depth of supply-side participation. Apartments continued to dominate October’s launches, accounting for 99% of total supply, with only 144 units introduced across the villa and townhouse segments. Year-to-date, the mix stands at 91.2% apartments, 4.8% townhouses, and 4.0% villas. Looking ahead, the launch pipeline points to a meaningful expansion in single-family home supply, with new clusters already slated from Emaar at Grand Polo Club and The Valley, the redesigned launch of The Heights, the first phase of DAMAC Islands 2, and additional releases expected as Wasl advances its expansion of Jumeirah Golf Estates.

Mortgage activity rebounded in October, registering 4,885 loans, a 28.9% month-on-month increase and back towards levels seen since Q2 2025. New purchase mortgages accounted for 58.3% of transactions, up 7.4% from September, with an average loan size of AED 1.79 million and an average loan-to-value (LTV) ratio of 73.6%. Refinancing and equity release loans fell to a 20.1% share (down 23.1%), while bulk mortgages surged 15.7% to 21.6% of total activity. The 866 bulk loans recorded were spread across multiple projects, most notably Portfolio Mortgage Registration at Ayat Parkview in Liwan (99), Florus Residence (89) in Al Furjan West, Salim 1 (81) in Arjan, AB South Residence (57) in Dubai South Residential District, as well as Portfolio Mortgage Modification at La Perla Blanca (190) in Jumeirah Village Circle and Shakespeare Tower (78) in Living Legends. This renewed uptick in bulk mortgage activity also reinforces last month’s assessment: many institutional buyers and developers appeared to have delayed financing decisions in anticipation of the recent 25 basis-point rate cut, with October now capturing the release of that postponed demand.

As Dubai moves deeper into the final quarter of the year, market conditions continue to show signs of measured normalization. Price growth has steadied, and while October marked the first month in 2025 not to set a new all-time high, transactional activity remains exceptionally elevated by historical standards. The easing in monthly gains reflects a market shifting from rapid expansion toward a more sustainable trajectory.

Mortgage activity appears poised for further improvement in the coming months as the recent rate cut fully filters through and expectations build around additional reductions. This will support both end-user sentiment and investment activity—particularly among institutional buyers who had deferred financing decisions earlier in the year.

At the same time, new supply continues to build at an unprecedented pace. The overwhelming volume of off-plan launches signals that developers are preparing for sustained demand, even if absorption rates gradually normalize. With more than 130,000 units launched year-to-date and additional low-density communities on the horizon, the market’s next phase will hinge on how effectively supply balances against moderating sales velocity.

Despite selective pockets of cooling, Dubai’s underlying fundamentals remain exceptionally strong: continued population inflows, economic resilience, and the city’s global positioning as a secure, investment-led hub. These drivers should underpin stability as the market transitions into 2026, even as buyers become more price-sensitive and developers more strategic in their release schedules.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |