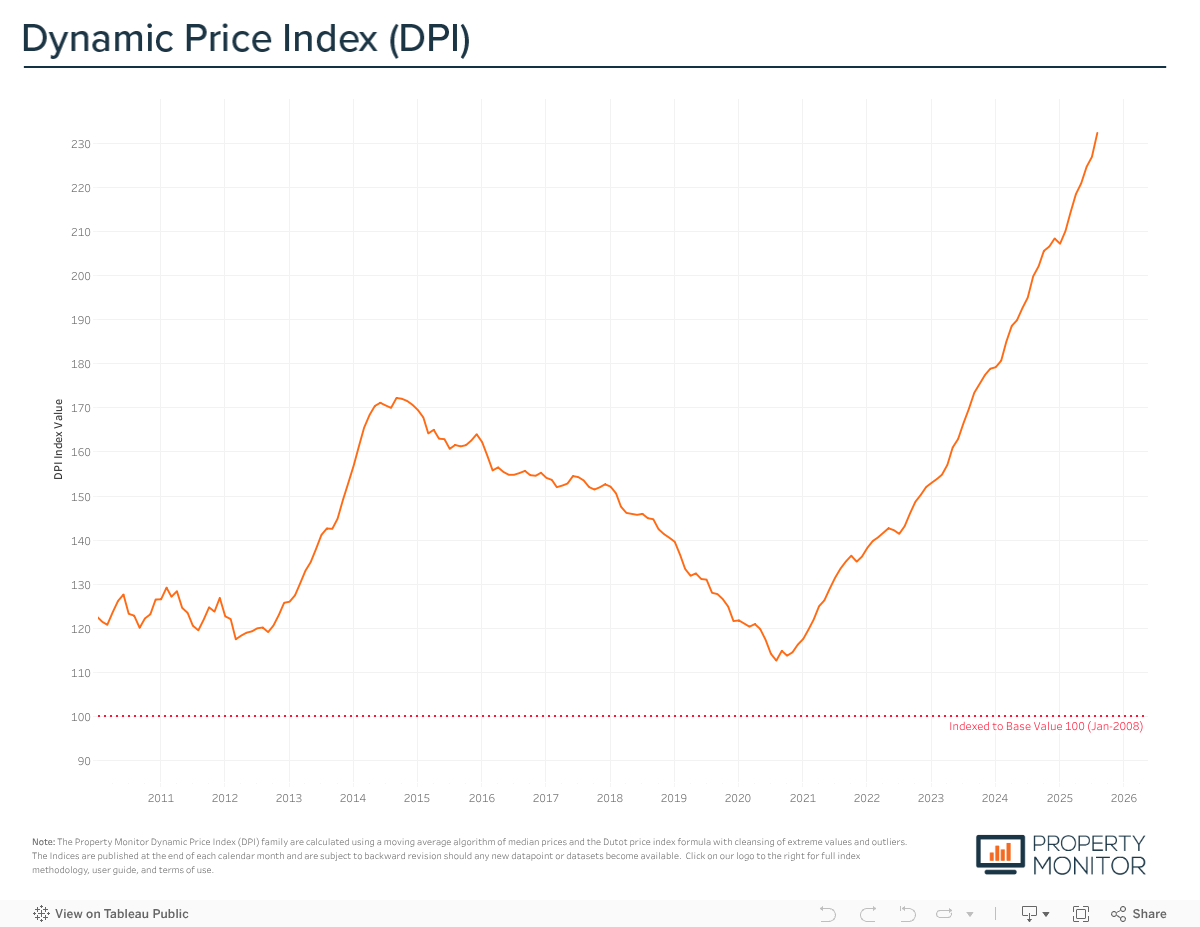

Dubai’s residential real estate market extended its growth in August, with prices rising 2.40% compared to July’s more subdued gain of 0.99%. The Property Monitor Dynamic Price Index (DPI) places average property prices at AED 1,664 per square foot, more than double the levels seen at the bottom of the market cycle in November 2020.

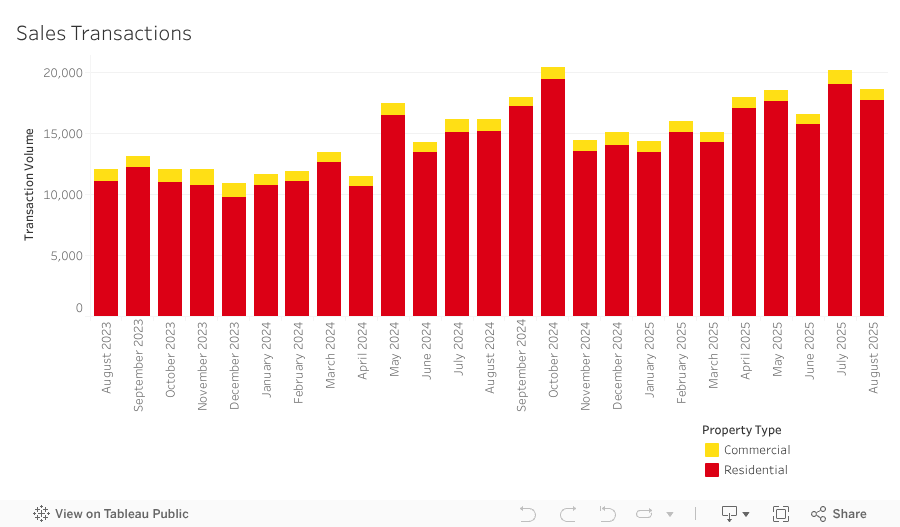

A total of 18,655 sales transactions were recorded in August, down 7.3% from July but still the highest ever for the month of August, continuing the pattern of record-breaking activity seen in every calendar month this year. While the dip from July likely reflects natural market seasonality, transaction volumes remain well above historical norms and are evidence of sustained liquidity in the market. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 94.4% (17,609 transactions). The highest transacted commercial property types were office spaces (1.8%), vacant land (1.3%), then hotel apartments (0.9%).

Year-to-date sales transaction volumes have surpassed just shy of 138,000 and are over 31.4% higher compared to the same period 2024. At the current pace of transaction velocity, we are on track to see year-end sales volumes surpass 205,000 and set a new all-time high.

In August, 13,116 off-plan Oqood transactions were recorded, an increase of 4.1% from the previous month, in tandem with the increase in volume, the overall market share also rose to 70.3%, up 7.7% month-on-month. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions represent an even larger market share of 75.7%. This underscores the central role of the off-plan market in driving headline transaction growth, though it also highlights the increasing reliance on future supply pipelines rather than immediate occupancy. Title Deed sale volumes, meanwhile, witnessed a sharp monthly decrease—dropping by 26.4% to account for just 29.7% of all transactions—a decline that was exacerbated by fewer off-plan villa and townhouse sales, which would otherwise have bolstered Title Deed volumes due to the way these properties are reported in DLD data.

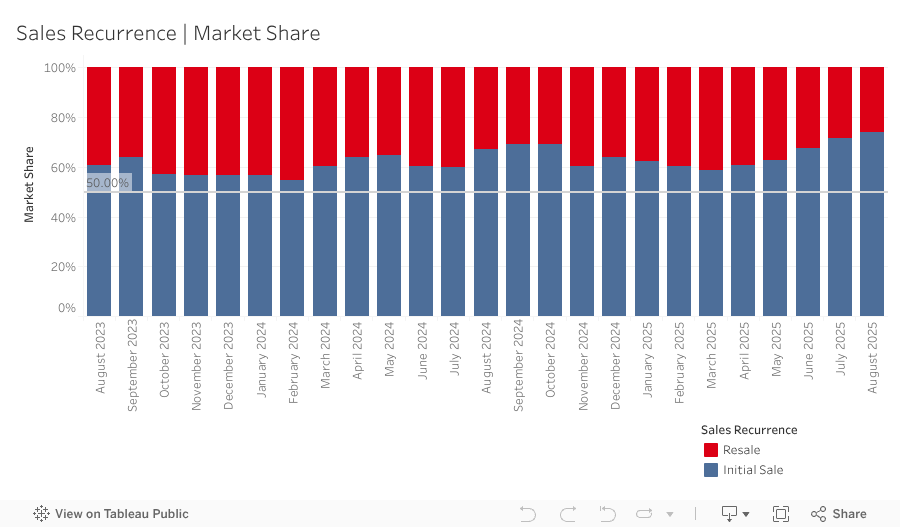

Meanwhile, resale transactions—any subsequent sale of a property following its initial sale by the developer—regardless of whether the first sale was off-plan or completed—stood at 4,762 in August, accounting for 25.5% of the market. This marks yet another monthly decrease, falling by 2.1%. Off-plan resales ticked up slightly in August, accounting for 21.1% of all resale activity, though the 12-month rolling average continued to decline, now at 25.5%. After peaking at over 33% in April, off-plan resales remain well below earlier highs—even as initial developer sales activity stays strong. This suggests the trend is being driven less by sellers looking to exit before handover and more by a tempering of buyer demand in the resale segment. With developers continuing to hold unsold inventory across many projects, resale listings—often priced above original purchase values—may be facing stiffer competition from direct-from-developer options, which generally offer a more straightforward transaction process along with incentives and flexible payment terms.

Dubai’s new project pipeline remained highly active in August, with 45 launches bringing over 9,000 residential units to market with an estimated gross sales value of AED 19.3 billion. Year-to-date, over 400 launches have taken place and close to 102,000 units have been brought to market—volumes that far exceed what historically would have been considered a full-year cycle. A total of 184 developers have launched projects so far in 2025, compared to 129 over the same period in 2024, underscoring the breadth of supply-side participation. Apartments continued to dominate new supply in August, accounting for 92.9% of launches, broadly in line with the 2025 year-to-date share of 90.5% (up from 85.2% in 2024). Villas and townhouses made up the balance, contributing 4.1% and 3.0% of August’s new supply, respectively. While the steady pace of launches reflects strong developer confidence, absorption is slowing—most notably for apartments. Projects from newer entrants are finding it harder to compete with established developers whose track records provide buyers with greater confidence, leaving many newcomers reliant on incentives and special offers to generate interest and facing a noticeably slower uptake of their launches.

Mortgage activity remained robust in August, registering 4,689 loans—the highest volume ever recorded for the month and the second strongest on record overall, despite a 4.1% decline from July’s all-time peak. New purchase mortgages represented 42.4% of transactions, down 3.2% from the prior month, with an average loan size of AED 1.9 million and an average loan-to-value (LTV) ratio of 73.9%. The remaining 24.8% (up by 8.7% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 1,163 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Nibras Oasis (216) in Dubai Silicon Oasis, Samaya (190) in Majan, and Murano Residences 2 (117) in Al Furjan, as well as portfolio mortgage modifications at Sol Avenue (323) in Business Bay.

As the market moves deeper into the third quarter, Dubai real estate continues to operate at historically high levels, though signs of strain are increasingly visible. Price growth remains positive and transaction volumes are on track to set new records, yet the surge in supply—particularly in the off-plan segment—raises questions about how much more demand the market can sustainably absorb.

Tailwinds such as continued population and wealth inflows, Dubai’s positioning as a global safe haven, and the likelihood of lower interest rates provide strong underlying support. The upcoming U.S. Federal Reserve FOMC meeting is expected to deliver at least a 25-basis point cut, with the possibility of further reductions by year-end—a shift that would reinforce already strong mortgage activity, sustain purchase demand, and likely spur refinancing.

At the same time, headwinds are building: affordability pressures are mounting, buyer selectivity is sharpening, and construction cost inflation—combined with the large pipeline of scheduled handovers in the coming years—could test both developer margins and delivery timelines. Looking ahead, the balance between supportive macro factors and emerging structural challenges will determine whether momentum can be sustained throughout 2025 and beyond.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |