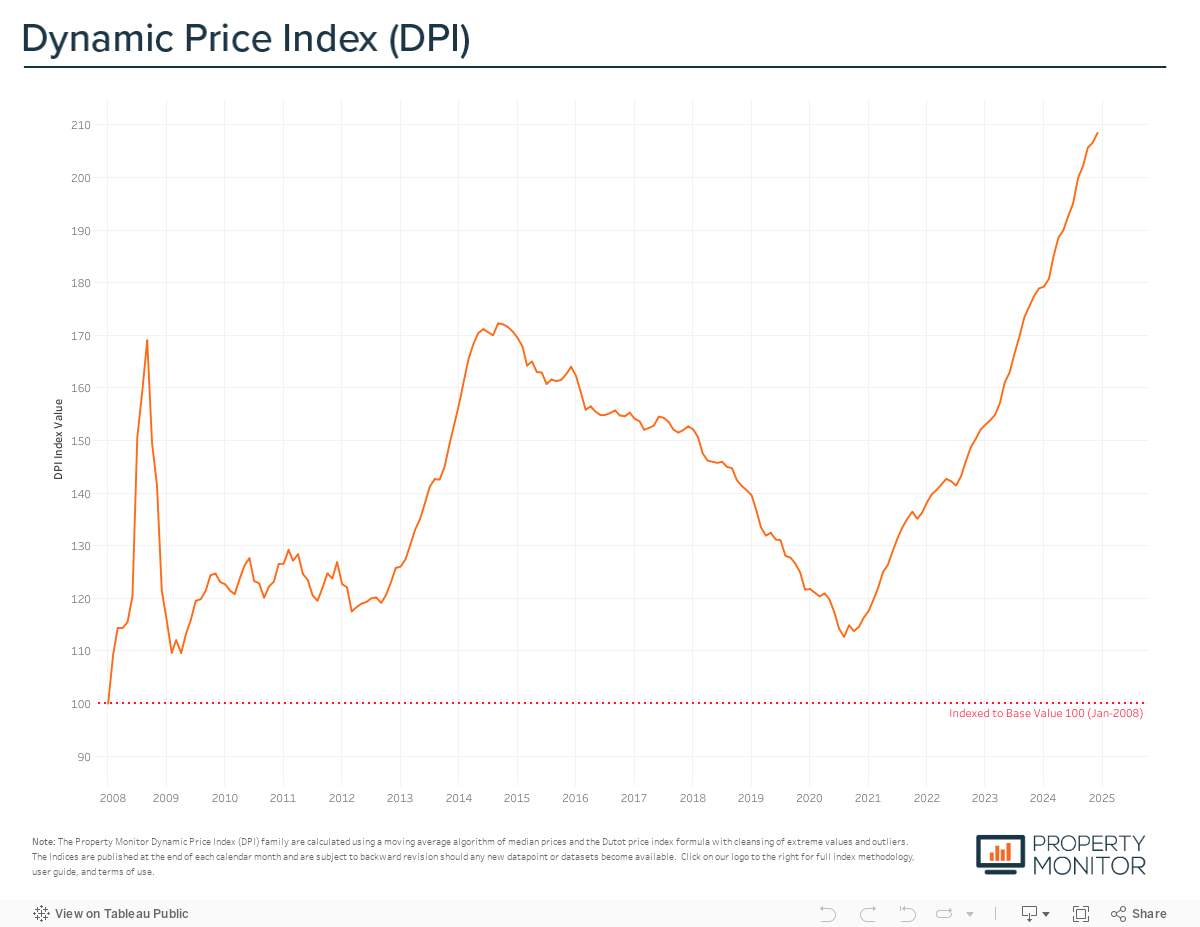

Dubai property prices continued their steady and moderately paced climb in December, rising by 0.88% month-on-month to reach AED 1,493 per square foot, according to the Property Monitor Dynamic Price Index (DPI). This marks a 16.52% year-on-year increase, closing out what has been another record-breaking year for Dubai’s real estate market. The current market cycle has now extended to 50 months, with average price appreciation sustaining a moderate pace of 1.22% per month.

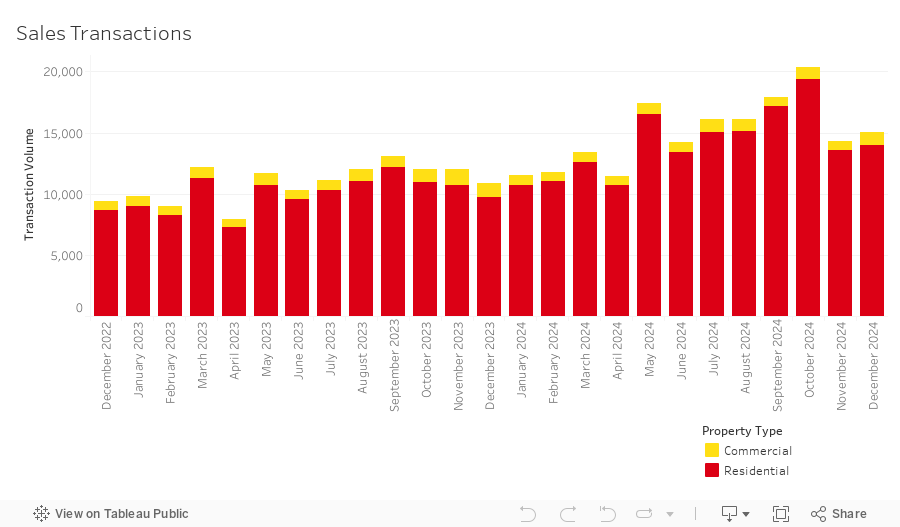

Closing out the year on a strong note, Dubai’s total sales transaction volume rose 4.3% month-on-month in December, reaching 15,108 transactions. While this represents a pullback from the record-breaking highs seen earlier in the year, it still marks the strongest December on record. Residential sales—comprising apartments, townhouses, and villas—continued to dominate, accounting for 92.8% of total transactions. Among commercial property types, vacant land (3.1%), office spaces (1.25%), and hotel apartments (1.2%) saw the highest transaction volumes.

With 181,131 total transactions, 2024 ended 35.5% higher than 2023’s total of 133,673, marking another exceptional year for Dubai’s real estate market. However, while the annual growth remains impressive, the dramatic spike in October transaction volumes—which set an all-time monthly record—appears increasingly to have been an outlier. The surge likely pulled forward demand, contributing to the comparatively lower volumes seen in November and December. Though seasonal factors and batch registrations of off-plan sales often cause fluctuations, this cooling-off period is a reminder that market momentum is not infinite.

In December, 9,179 off-plan Oqood transactions were recorded, an increase of 7.4% from the previous month and an increase in market share to 50.8%. Meanwhile, Title Deed sale volumes witnessed a minor decrease, falling by 0.1% and now account for 39.2% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions secure an even larger market share of 69.9%.

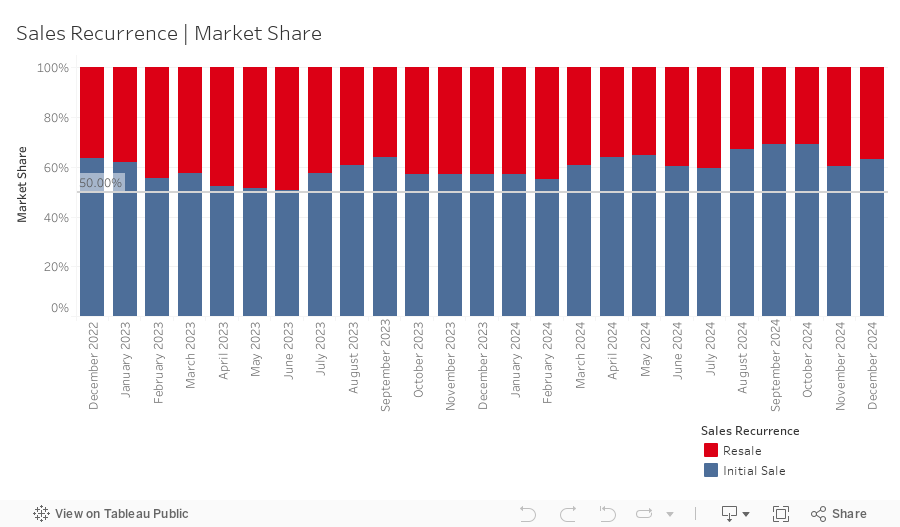

Meanwhile, resale transactions— any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project —stood at 5,572 in December, accounting for 36.9% of the market. This marks a 2.7% decline month-on-month, though provisional figures indicate that the share of off-plan resales climbed to 29.7%, its highest level on record and well above the 12-month rolling average of 25.3%. Off-plan resale activity has been on a steady upward trajectory over the past three years, largely concentrated in properties nearing completion. However, a notable shift is emerging, with a growing share of resales occurring for units further from handover. While this does not yet indicate a surge in speculative flipping, it is an early signal worth monitoring. A sustained rise in such transactions could suggest shifting market dynamics, and as the volume of off-plan supply continues to grow, resale activity will be an important indicator of overall market sentiment and investor behavior.

New off-plan development project launches for December came in strong, with just over 10,600 off-plan units added to the market for sale, carrying an anticipated combined gross sales value of ~AED 26.8 billion. Apartments continue to dominate, accounting for 94.2% of new inventory, while townhouses and villas represent 3.3% and 2.5%, respectively. The year closed with off-plan launches at all-time highs—surpassing 145,000 units and AED 360.1 billion in aggregate sales value—an extraordinary leap from the 96,000 units launched in 2023 and 53,000 in 2022.

The surge in new projects has been driven by a rapidly expanding developer landscape, with the number of active developers rising by 47.2% year-on-year and project launches increasing by 42.9%. This expansion has fostered a broader diversity in product offerings—whereas 2023 was dominated by luxury and ultra-luxury launches, 2024 has seen a shift towards a more varied spectrum of price points, catering to a wider pool of buyers. With over 250 additional projects currently in the planning pipeline, new launches are expected to remain at historically high levels well into 2025.

Mortgage transaction volumes decreased by 3.3% in December with a total of 3,871 loans recorded. During the month, loans taken for new purchase money mortgages accounted for 43.8% (down 17.1% from last month) of borrowing activity, with the average amount borrowed being AED 1.79m at a loan-to-value ratio of 76.3%. Meanwhile, loans for refinancing and equity release saw their market share increase by 10.4% to 24.4%. The remaining 30.8% (up by 6.7% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 1,192 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Al Sayyah Residences (268) in Arjan, Shorooq Land 2 (227) and Luna Residence (190) in Dubai Land Residence Complex, as well as portfolio mortgage modifications at buildings B2 and C1 at The Neighborhood in Al Barari. The December numbers bring the total volume of mortgages for 2024 to an all-time record of 41,518 loans and an 18.2% year-on-year.

As 2024 comes to an end, the market stands nearly 21% above the previous all-time high of September 2014, reinforcing Dubai’s resilience and sustained growth. Despite a year filled with record-breaking sales volumes, price appreciation has remained measured and stable, steering clear of speculative volatility seen in previous cycles. While monthly fluctuations are expected, particularly with the continued dominance of the off-plan segment, the overarching trend signals sustained demand and market confidence.

However, key questions emerge as the market continues to scale. With unit volume up 51.9% year-on-year and aggregate sales value increasing 32.6%, demand remains strong, but the pace of absorption will be critical to monitor. The sheer volume of new supply entering the market in 2025 will put further pressure on sustaining high transaction levels, and any signs of cooling investor sentiment or weaker off-plan take-up could signal a shift in momentum. The continued success of Dubai’s long-term real estate vision will depend on maintaining a healthy equilibrium between supply and demand to avoid potential oversaturation.

Mortgage activity, often a bellwether for buyer confidence, saw a 3.3% decline in December, though total mortgage volumes for the year reached a record 41,518 loans, an 18.2% increase year-on-year. Unlike most global markets, Dubai bucked the trend throughout the recent rate-hike cycle, with borrowing activity surging despite higher interest rates—a stark contrast to the typical slowdown seen elsewhere. With the U.S. Federal Reserve signaling potential rate cuts in 2025, currently expected at 50 basis points across two reductions, borrowing conditions may become more favorable. However, given Dubai’s unique response to rising rates, it remains to be seen whether rate cuts will further stimulate demand or if the market has already adapted to higher borrowing costs. Mortgage activity in early 2025 will be an important indicator of real demand, particularly for end-users versus investors.

Looking ahead, 2025 will be a defining year for Dubai’s real estate sector. With off-plan development continuing at historic levels, investor interest holding firm, and government-backed initiatives such as the Dubai Economic Agenda (D33) and the Real Estate Sector Strategy 2033 providing long-term confidence, Dubai remains well-positioned for continued growth. However, as the market matures, expectations must adjust to a more balanced trajectory—one that favors sustainability over rapid expansion. While the big gains of the past four years may be behind us, stability, liquidity, and strategic development will be the key themes shaping the year ahead.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |