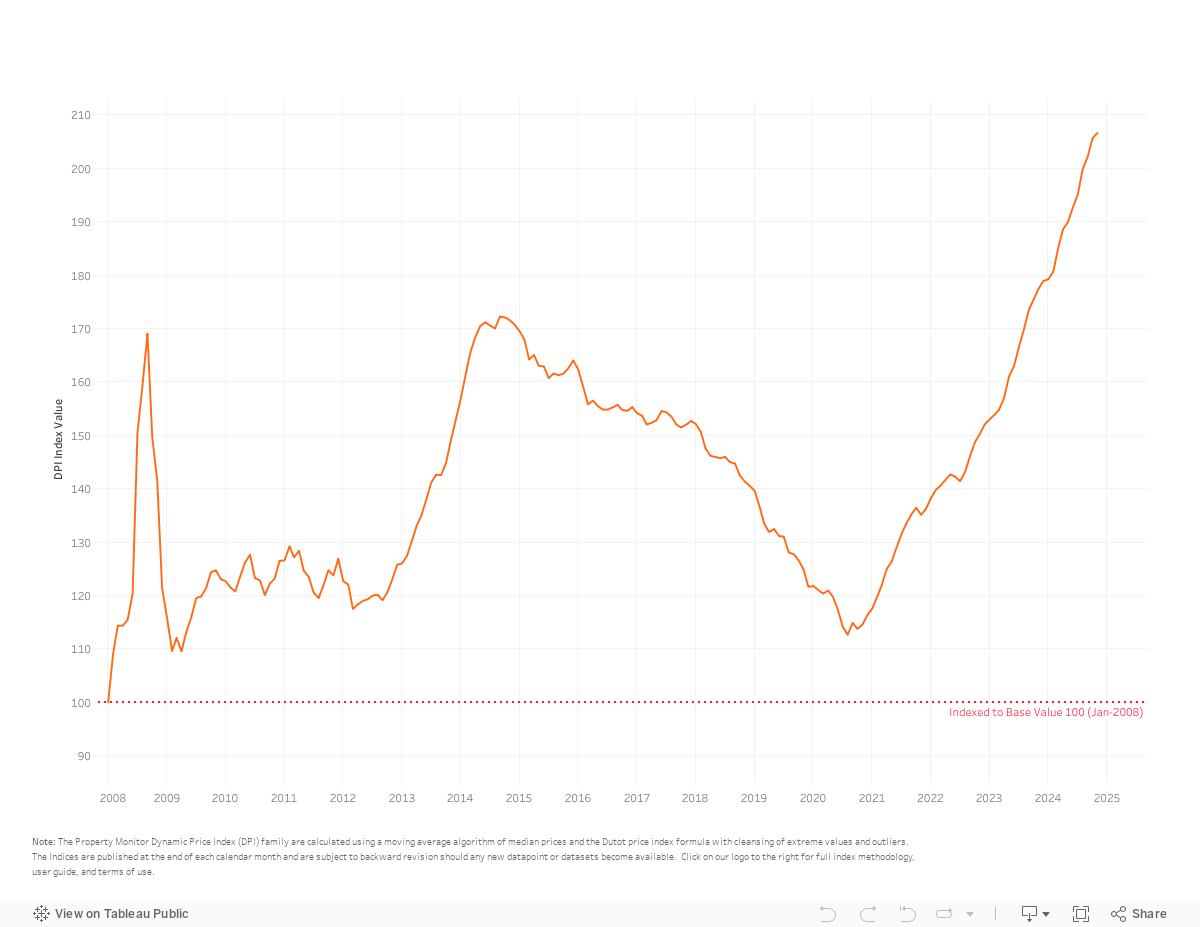

After several months of price appreciation well above 1% month-on-month, Dubai property prices grew by a subdued 0.48% in November and currently stand at AED 1,480 per square foot, just shy of 20% over the previous all-time high and market peak of September 2014. According to the Property Monitor Dynamic Price Index (DPI), the upward phases (recovery and growth) of the current market cycle have spanned 49 months so far, with prices increasing at a moderate rate of 1.23% per month on average. In contrast to the previous market cycle—one that experienced a period of aggressive price increases in excess of 2% per month—which lasted only 24-months and saw average monthly appreciation of 1.6%, what we are experiencing now shows greater signs of stability with less speculative activity. Barring any major disruptions, this trend appears likely to carry on well into the New Year.

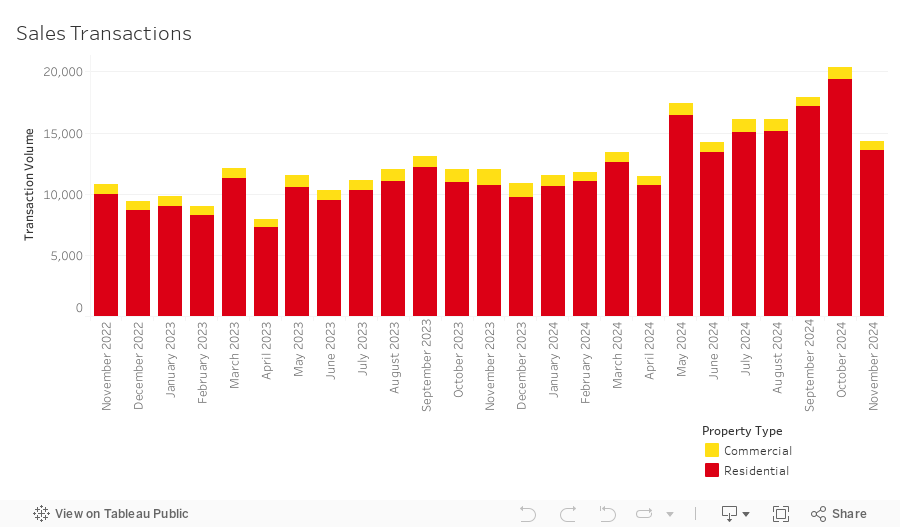

On the heels of a record shattering October—where sales transactions saw a 13.4% increase and breached 20,000 for the first time ever—the volume of sales transactions dropped in November to 14,483, a decrease of 29.2%. Despite the marked decrease, this still registers as the highest volume ever for the month of November, shattering the previous November record by more than 18%. Residential transactions, encompassing apartments, townhouses, and villas, accounted for the majority of sales at 93.5% (13,537 transactions). The highest transacted commercial property types were office spaces (1.9%), vacant land (1.7%), and hotel apartments (1.1%). Annual sales transaction volumes have now surpassed 166,000 and have eclipsed 2023 year-end sales by 24.2%. With just one month remaining, we are on track to see a year-on-year increase of close to 35% (~185,000 sales).

In November, 8,550 off-plan Oqood transactions were recorded, a decrease of 35.8% from the previous month and a decrease in market share falling to 59.0%. Meanwhile, Title Deed sale volumes also witnessed a decrease, falling by 17.0% and now account for 41.0% of all sales transactions. While Oqood transactions are generally used to measure the off-plan market, several villa and townhouse sales are presented in the Dubai Land Department data as being issued with Title Deeds and as completed properties—instead of being under construction and sold off-plan. After adjusting for this technicality, off-plan transactions secure an even larger market share of 64.0%.

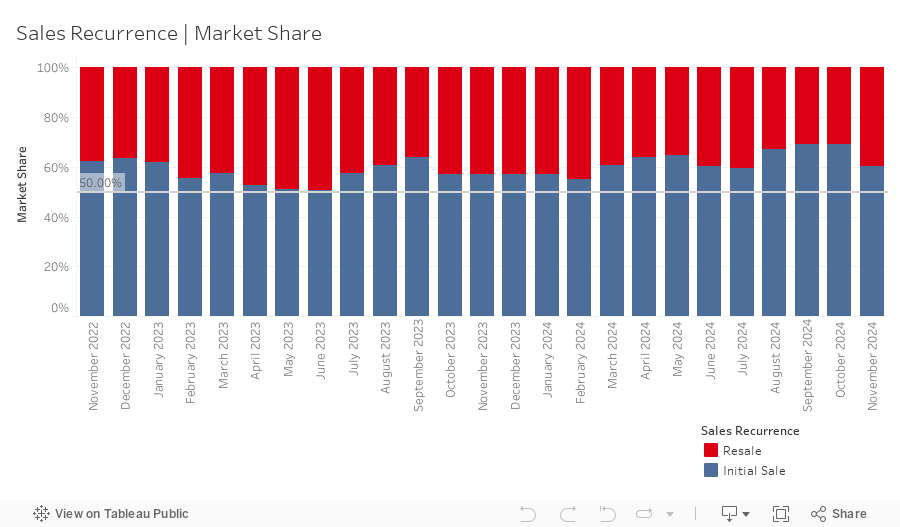

Meanwhile, resales transactions—any subsequent sale of a property that follows the initial first-time sale from the developer, for an off-plan or completed project—stood at 5,737 in November representing a market share of 39.6%, increasing by 8.4% month-on-month. While overall resale activity increased, the portion of off-plan resales decreased to 23.6%, falling below the 12-month rolling average of 24.4%. Off-plan resale activity has seen a steady yet gradual rise over the past three years. However, as in previous months, the bulk of these resales are concentrated in properties nearing completion within the year, suggesting a healthy demand rather than purely speculative trading.

New off-plan development project launches remain at record highs, with just over 17,700 off-plan units added to the market for sale with an anticipated combined gross sales value of ~AED 53.7 billion. Apartments represent 71.8% by volume of this new inventory, while townhouses and villas represent 23.9% and 4.3% respectively. Year-to-date, new project launches have reached slightly less than 135,000 units and AED 333.3 billion in aggregate sales value. This well surpasses both the volume and value of units launched throughout the entirety of 2023. With more than double the amount of developers active in the market, this has led to a much greater diversity in product offerings—while 2023 saw launches skewed towards the luxury and ultra-luxury segments, 2024 has seen projects spread across a wider range of price segments. With over 250 additional projects in the planning phases being tracked by the Property Monitor team, we anticipate that new launches will maintain historically high levels well into 2025.

Mortgage transaction volumes decreased by 7.3% in November, dropping to 4,004. This follows October’s stellar performance which saw the second highest level of mortgages ever recorded. During the month, loans taken for new purchase money mortgages accounted for 60.9% (up 12.7% from last month) of borrowing activity, with the average amount borrowed being AED 2.03m at a loan-to-value ratio of 76.4%. Meanwhile, loans for refinancing and equity release saw their market share decrease by 18.3% to 15.0%. The remaining 24.1% (up by 5.6% from last month) was due to bulk mortgages—those taken by developers and larger investors with multiple units. The 767 bulk loans issued for the month were spread across several projects, most notably portfolio mortgage registrations at Jeewar Tower (220) in Jumeirah Village Circle and Etlala Residence 2 (102) in Dubai Land Residence Complex, as well as portfolio mortgage modifications at Eden Apartments in Motor City.

As 2024 draws to a close, it’s a fitting moment to reflect on the remarkable performance of Dubai’s real estate market over the past year. Since the market bottomed out just over four years ago, prices have risen more than 60%, averaging a steady 1.23% monthly growth, with a slightly higher average of 1.28% over the past 12 months. This pace, while robust, can be viewed as moderate and aligned with a sustainable growth trajectory, which is a blend of growth across both the ready and off-plan segments of the market. Simultaneously, transaction volumes have been extraordinary, averaging 9,527 per month since the recovery began, and an impressive 14,758 per month over the past year. To put this in perspective, during the last recovery cycle ending in April 2014—a 24-month phase—monthly transaction volumes averaged just 5,155, a staggering 84.8% lower than the current cycle. These figures raise an important question: how long can this unprecedented level of activity persist?

Dubai’s strong performance is underpinned by its ambitious goals outlined in frameworks such as the 2040 Urban Master Plan, the D33 Dubai Economic Agenda, the Dubai Social Agenda 33, and the Real Estate Sector Strategy 2033. These initiatives, supported by forward-thinking regulatory reforms, continue to attract population and economic growth, cementing Dubai’s position as a global outlier in real estate. The fundamentals driving this growth are solid and unlikely to dissipate in the near term.

The off-plan market has been another significant driver of activity, with new project launches appealing to a wide range of buyers, from investors to end-users. While uptake has been strong, the increasing frequency of new launches warrants careful observation. A slowdown in absorption rates could serve as an early indicator of potential oversupply, which may lead to a cooling market. As we move into 2025, maintaining a balanced perspective will be crucial. While the market’s health remains strong, the lessons of past cycles must guide decisions across all stakeholders—developers, investors, and consumers alike.

The current boom will not continue indefinitely. The substantial gains of recent years are likely behind us for the time being. Heading into 2025, we anticipate a period of price stability, with modest gains and losses evening out over time, reflecting a market that is maturing and adapting to sustained growth dynamics.

This website uses cookies to improve your experience

Accept AllCookie Preferencesx| Cookie | Duration | Description |

|---|---|---|

| cookielawinfo-checkbox-analytics | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics". |

| cookielawinfo-checkbox-functional | 11 months | The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional". |

| cookielawinfo-checkbox-necessary | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary". |

| cookielawinfo-checkbox-others | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other. |

| cookielawinfo-checkbox-performance | 11 months | This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance". |

| viewed_cookie_policy | 11 months | The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data. |